Paul Bousquet

@pbousquet.bsky.social

Econ PhD @ UVA | mostly sharing macro research from twitter until people are more active here | pbousquet.com

Pinned

Paul Bousquet

@pbousquet.bsky.social

· Jul 10

A typical centerpiece of papers probing "monetary policy's effect on x" or "how does x affect MP's effects on y" is results from a LP or VAR with an off the shelf monetary surprise series. Some papers asking important questions about how to do and think about these exercises ⬇️ #EconSky

Reposted by Paul Bousquet

Global solutions with adaptive sparse grids are now implemented in Dynare.jl, thanks to @compsimon.bsky.social and team! This should substantially improve the ease of implementing fully nonlinear medium-scale macro models.

New Dynare working paper (with source code!): “Scalable Global Solution Techniques for High-Dimensional Models in Dynare” by Aryan Eftekhari, Michel Juillard, Normann Rion and Simon Scheidegger

www.dynare.org/wp-repo/dyna...

github.com/NormannR/HDM...

www.dynare.org/wp-repo/dyna...

github.com/NormannR/HDM...

www.dynare.org

November 17, 2025 at 11:27 AM

Global solutions with adaptive sparse grids are now implemented in Dynare.jl, thanks to @compsimon.bsky.social and team! This should substantially improve the ease of implementing fully nonlinear medium-scale macro models.

Reposted by Paul Bousquet

Excellent VSME talk by Jordi Gali, who provided a new perspective on monetary policy rules based on his Keynes Lectures and discussion at Jackson Hole of Emi Nakamura's paper. He makes a compelling case for rules for long-term real rates. Video here:

www.youtube.com/watch?v=UrbH...

www.youtube.com/watch?v=UrbH...

November 11, 2025 at 4:12 PM

Excellent VSME talk by Jordi Gali, who provided a new perspective on monetary policy rules based on his Keynes Lectures and discussion at Jackson Hole of Emi Nakamura's paper. He makes a compelling case for rules for long-term real rates. Video here:

www.youtube.com/watch?v=UrbH...

www.youtube.com/watch?v=UrbH...

Reposted by Paul Bousquet

Can a central bank tighten monetary policy and actually see real interest rates FALL under monetary dominance?

My new research paper finds that under certain conditions, the answer is a surprising YES.

A thread on a monetary policy puzzle (1/10) #Economics #MonetaryPolicy #CentralBank

My new research paper finds that under certain conditions, the answer is a surprising YES.

A thread on a monetary policy puzzle (1/10) #Economics #MonetaryPolicy #CentralBank

September 24, 2025 at 2:01 AM

Can a central bank tighten monetary policy and actually see real interest rates FALL under monetary dominance?

My new research paper finds that under certain conditions, the answer is a surprising YES.

A thread on a monetary policy puzzle (1/10) #Economics #MonetaryPolicy #CentralBank

My new research paper finds that under certain conditions, the answer is a surprising YES.

A thread on a monetary policy puzzle (1/10) #Economics #MonetaryPolicy #CentralBank

To my surprise, I have written another Substack on the Fed info effect.

I've read Karthik Sastry's excellent forthcoming AEJ many times but recently it dawned on me that one of his results seemed to contradict a well-established idea in this literature

whymacro.substack.com/p/fed-info-r...

I've read Karthik Sastry's excellent forthcoming AEJ many times but recently it dawned on me that one of his results seemed to contradict a well-established idea in this literature

whymacro.substack.com/p/fed-info-r...

October 27, 2025 at 1:18 PM

To my surprise, I have written another Substack on the Fed info effect.

I've read Karthik Sastry's excellent forthcoming AEJ many times but recently it dawned on me that one of his results seemed to contradict a well-established idea in this literature

whymacro.substack.com/p/fed-info-r...

I've read Karthik Sastry's excellent forthcoming AEJ many times but recently it dawned on me that one of his results seemed to contradict a well-established idea in this literature

whymacro.substack.com/p/fed-info-r...

Reposted by Paul Bousquet

October 22, 2025 at 2:35 AM

Reposted by Paul Bousquet

📣 We are excited to share the program for the IM-TCD virtual seminar series 2025-26!

Would you like to join? Sign up here 👇:

forms.office.com/e/hYhCPCZ2Lp

@tcdeconomics.bsky.social #EconBlueSky #EconSky

Would you like to join? Sign up here 👇:

forms.office.com/e/hYhCPCZ2Lp

@tcdeconomics.bsky.social #EconBlueSky #EconSky

September 17, 2025 at 1:11 PM

📣 We are excited to share the program for the IM-TCD virtual seminar series 2025-26!

Would you like to join? Sign up here 👇:

forms.office.com/e/hYhCPCZ2Lp

@tcdeconomics.bsky.social #EconBlueSky #EconSky

Would you like to join? Sign up here 👇:

forms.office.com/e/hYhCPCZ2Lp

@tcdeconomics.bsky.social #EconBlueSky #EconSky

Nice short paper with a new way to demonstrate how critical assumptions about policy are for model dynamics

Expectation Response Functions capture how today's economy responds to beliefs about the future—regardless of how those beliefs are formed, from Ryan Chahrour and Kyle Jurado https://www.nber.org/papers/w34210

September 13, 2025 at 12:11 PM

Nice short paper with a new way to demonstrate how critical assumptions about policy are for model dynamics

Justifications for the "central bank information effect" are largely abstract. But a new WP floats a tangible mechanism: the FOMC sometimes gets early access to important manufacturing data.

My first substack uses these claims to assess the broader debate

whymacro.substack.com/p/the-fed-in...

My first substack uses these claims to assess the broader debate

whymacro.substack.com/p/the-fed-in...

The Fed Information Effect: A New Perspective

I’ve always been skeptical of the idea that people learn about the economy directly through central bank press events.

whymacro.substack.com

September 1, 2025 at 1:53 PM

Justifications for the "central bank information effect" are largely abstract. But a new WP floats a tangible mechanism: the FOMC sometimes gets early access to important manufacturing data.

My first substack uses these claims to assess the broader debate

whymacro.substack.com/p/the-fed-in...

My first substack uses these claims to assess the broader debate

whymacro.substack.com/p/the-fed-in...

Reposted by Paul Bousquet

🧵It was a great pleasure to work with excellent colleagues across the @federalreserve.gov on a paper for the FOMC framework review. Thanks to my coauthors Travis Berge, Giuseppe Fiori, Francesca Loria, Molin Zhong. You can find the paper here:

www.federalreserve.gov/econres/feds... 1/3

www.federalreserve.gov/econres/feds... 1/3

Accounting for Uncertainty and Risks in Monetary Policy

The Federal Reserve Board of Governors in Washington DC.

www.federalreserve.gov

August 26, 2025 at 8:05 PM

🧵It was a great pleasure to work with excellent colleagues across the @federalreserve.gov on a paper for the FOMC framework review. Thanks to my coauthors Travis Berge, Giuseppe Fiori, Francesca Loria, Molin Zhong. You can find the paper here:

www.federalreserve.gov/econres/feds... 1/3

www.federalreserve.gov/econres/feds... 1/3

A much needed meta-analysis with an extensive replication repo to boot

We have a new paper on the overstated effects of conventional monetary policy on output and prices. Results reported in the literature are plagued by p-hacking and publication bias, leading to inflated effect sizes of how interest rate hikes affect output and prices.

August 21, 2025 at 2:41 PM

A much needed meta-analysis with an extensive replication repo to boot

Reposted by Paul Bousquet

Interested in top-notch research in monetary economics? Join us for this new online seminar series, co-hosted CEPR's Monetary Economics and Fluctuations program and our Center for Monetary Research! @ivanwerning.bsky.social will kick things off on Sep-4.

Sign up: cepr-org.zoom.us/webinar/regi...

Sign up: cepr-org.zoom.us/webinar/regi...

New Virtual Seminar series on #MonetaryEconomics begins September 2025, joint with the Center for Monetary Research of the Federal Reserve Bank of San Francisco.

Monthly sessions explore central bank frameworks, policy design, and international dimensions.

More: cepr.org/events/event...

#EconSky

Monthly sessions explore central bank frameworks, policy design, and international dimensions.

More: cepr.org/events/event...

#EconSky

July 31, 2025 at 3:11 PM

Interested in top-notch research in monetary economics? Join us for this new online seminar series, co-hosted CEPR's Monetary Economics and Fluctuations program and our Center for Monetary Research! @ivanwerning.bsky.social will kick things off on Sep-4.

Sign up: cepr-org.zoom.us/webinar/regi...

Sign up: cepr-org.zoom.us/webinar/regi...

A typical centerpiece of papers probing "monetary policy's effect on x" or "how does x affect MP's effects on y" is results from a LP or VAR with an off the shelf monetary surprise series. Some papers asking important questions about how to do and think about these exercises ⬇️ #EconSky

July 10, 2025 at 3:38 PM

A typical centerpiece of papers probing "monetary policy's effect on x" or "how does x affect MP's effects on y" is results from a LP or VAR with an off the shelf monetary surprise series. Some papers asking important questions about how to do and think about these exercises ⬇️ #EconSky

Reposted by Paul Bousquet

🧵:

What does monetary policy do?

Our best evidence comes from quality empirical monetary policy shocks (EMPS) using high-frequency and narrative methods.

… but what *are* these shocks?

What does monetary policy do?

Our best evidence comes from quality empirical monetary policy shocks (EMPS) using high-frequency and narrative methods.

… but what *are* these shocks?

a cartoon dog in a pink suit and bow tie says let 's find out

ALT: a cartoon dog in a pink suit and bow tie says let 's find out

media.tenor.com

July 9, 2025 at 12:34 PM

🧵:

What does monetary policy do?

Our best evidence comes from quality empirical monetary policy shocks (EMPS) using high-frequency and narrative methods.

… but what *are* these shocks?

What does monetary policy do?

Our best evidence comes from quality empirical monetary policy shocks (EMPS) using high-frequency and narrative methods.

… but what *are* these shocks?

Reposted by Paul Bousquet

Connor Brennan, Maggie Jacobson, Todd Walker, and I have now made the shock series we created for our “Monetary Policy Shocks: Data or Methods?” paper public. Any comments are greatly appreciated!

Data: doi.org/10.7910/DVN/MQ…

Paper: cm1518.github.io/files/BMW.pdf

Data: doi.org/10.7910/DVN/MQ…

Paper: cm1518.github.io/files/BMW.pdf

https://doi.org/10.7910/DVN/MQ…

June 28, 2025 at 2:33 AM

Connor Brennan, Maggie Jacobson, Todd Walker, and I have now made the shock series we created for our “Monetary Policy Shocks: Data or Methods?” paper public. Any comments are greatly appreciated!

Data: doi.org/10.7910/DVN/MQ…

Paper: cm1518.github.io/files/BMW.pdf

Data: doi.org/10.7910/DVN/MQ…

Paper: cm1518.github.io/files/BMW.pdf

Reposted by Paul Bousquet

🚨New paper with Veronica Guerrieri and Guido Lorenzoni

Was the recent inflation surge due to a lack of coordination? Can lack of coordination lead to too much inflation?

Yes, we show. Especially in response to global supply shocks.

link to paper: economics.mit.edu/sites/defaul...

1/n🧵

Was the recent inflation surge due to a lack of coordination? Can lack of coordination lead to too much inflation?

Yes, we show. Especially in response to global supply shocks.

link to paper: economics.mit.edu/sites/defaul...

1/n🧵

June 9, 2025 at 12:48 PM

🚨New paper with Veronica Guerrieri and Guido Lorenzoni

Was the recent inflation surge due to a lack of coordination? Can lack of coordination lead to too much inflation?

Yes, we show. Especially in response to global supply shocks.

link to paper: economics.mit.edu/sites/defaul...

1/n🧵

Was the recent inflation surge due to a lack of coordination? Can lack of coordination lead to too much inflation?

Yes, we show. Especially in response to global supply shocks.

link to paper: economics.mit.edu/sites/defaul...

1/n🧵

Reposted by Paul Bousquet

Editing our writing is a common academic task. I *hate* how spell/grammar checks annoy me by thinking proper nouns or LaTeX code are misspellings (yes, I want `` ''). I also want *style* tips like a good editor would give me. Problem solved. 1/5

June 12, 2025 at 9:55 PM

Editing our writing is a common academic task. I *hate* how spell/grammar checks annoy me by thinking proper nouns or LaTeX code are misspellings (yes, I want `` ''). I also want *style* tips like a good editor would give me. Problem solved. 1/5

Reposted by Paul Bousquet

New! Efficient Estimation of Nonlinear DSGE Models, w/ Sean McCrary

📄 papers.ssrn.com/sol3/papers....

We propose a broadly applicable computationally efficient method for full-information estimation of nonlinear DSGE models. It avoids two key bottlenecks: global solutions and nonlinear filters.

📄 papers.ssrn.com/sol3/papers....

We propose a broadly applicable computationally efficient method for full-information estimation of nonlinear DSGE models. It avoids two key bottlenecks: global solutions and nonlinear filters.

Efficient Estimation of Nonlinear DSGE Models

This paper introduces a computationally efficient method for full-information estimation of nonlinear Dynamic Stochastic General Equilibrium (DSGE) models. In c

papers.ssrn.com

June 6, 2025 at 6:41 PM

New! Efficient Estimation of Nonlinear DSGE Models, w/ Sean McCrary

📄 papers.ssrn.com/sol3/papers....

We propose a broadly applicable computationally efficient method for full-information estimation of nonlinear DSGE models. It avoids two key bottlenecks: global solutions and nonlinear filters.

📄 papers.ssrn.com/sol3/papers....

We propose a broadly applicable computationally efficient method for full-information estimation of nonlinear DSGE models. It avoids two key bottlenecks: global solutions and nonlinear filters.

Reposted by Paul Bousquet

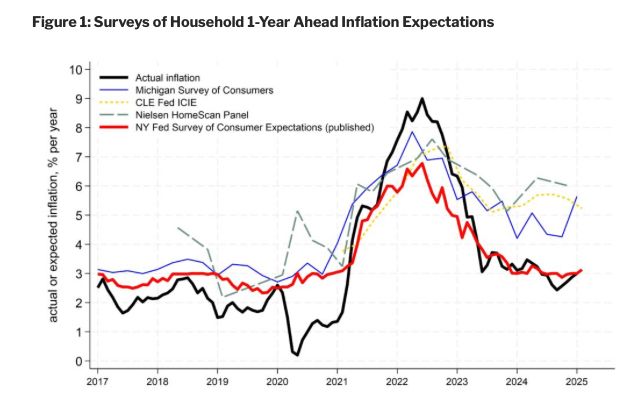

What's happening with inflation expectations?

Two often used household surveys disagree:

- the Michigan MSC says inflation expectations are up

- the NY Fed SCE says they're not...

Which one is it?

New blog by Oli Coibion and @ygorodnichenko.bsky.social says: MSC is right!

Find out why ⬇️

Two often used household surveys disagree:

- the Michigan MSC says inflation expectations are up

- the NY Fed SCE says they're not...

Which one is it?

New blog by Oli Coibion and @ygorodnichenko.bsky.social says: MSC is right!

Find out why ⬇️

April 29, 2025 at 9:25 PM

What's happening with inflation expectations?

Two often used household surveys disagree:

- the Michigan MSC says inflation expectations are up

- the NY Fed SCE says they're not...

Which one is it?

New blog by Oli Coibion and @ygorodnichenko.bsky.social says: MSC is right!

Find out why ⬇️

Two often used household surveys disagree:

- the Michigan MSC says inflation expectations are up

- the NY Fed SCE says they're not...

Which one is it?

New blog by Oli Coibion and @ygorodnichenko.bsky.social says: MSC is right!

Find out why ⬇️

Reposted by Paul Bousquet

Paper alert: "Scalable Global Solution Techniques for High-Dimensional Models in Dynare" (papers.ssrn.com/sol3/papers....), code: nvls. co/Dynare/GlobalMethods/SparseGrids (joint work with N. Rion, M. Juillard, A. Eftekhari)

April 2, 2025 at 7:37 PM

Paper alert: "Scalable Global Solution Techniques for High-Dimensional Models in Dynare" (papers.ssrn.com/sol3/papers....), code: nvls. co/Dynare/GlobalMethods/SparseGrids (joint work with N. Rion, M. Juillard, A. Eftekhari)

Reposted by Paul Bousquet

March 31, 2025 at 9:34 PM

Reposted by Paul Bousquet

#EconSky: Favorite empirical papers on firms' objective function and whether firms optimize?

I'm specifically interested in the concept that firms may only re-optimize (e.g. pricing) infrequently, once they get hit by a shock. Whether because of inertia or adjustment costs.

I'm specifically interested in the concept that firms may only re-optimize (e.g. pricing) infrequently, once they get hit by a shock. Whether because of inertia or adjustment costs.

March 6, 2025 at 8:35 PM

#EconSky: Favorite empirical papers on firms' objective function and whether firms optimize?

I'm specifically interested in the concept that firms may only re-optimize (e.g. pricing) infrequently, once they get hit by a shock. Whether because of inertia or adjustment costs.

I'm specifically interested in the concept that firms may only re-optimize (e.g. pricing) infrequently, once they get hit by a shock. Whether because of inertia or adjustment costs.

Reposted by Paul Bousquet

Bayesian logic in entrepreneurial experimentation continues to apply under Knightian uncertainty, from @joshgans.bsky.social https://www.nber.org/papers/w33507

March 1, 2025 at 2:00 PM

Bayesian logic in entrepreneurial experimentation continues to apply under Knightian uncertainty, from @joshgans.bsky.social https://www.nber.org/papers/w33507

Reposted by Paul Bousquet

Deriving asymptotically unbiased estimates of the multi-step forecasting risk and the impulse response estimation risk to determine hyperparameters in settings where the Bayesian vector autoregressions is (potentially) misspecified, from González-Casasús and Sch... https://www.nber.org/papers/w33474

February 19, 2025 at 10:00 PM

Deriving asymptotically unbiased estimates of the multi-step forecasting risk and the impulse response estimation risk to determine hyperparameters in settings where the Bayesian vector autoregressions is (potentially) misspecified, from González-Casasús and Sch... https://www.nber.org/papers/w33474

Reposted by Paul Bousquet

I couldn't agree more!

The excessive focus on linearized solutions to HA models is a bit like the old joke about the drunk who is looking for a key under a lamppost because that's where the light is.

More discussion of why we need non-linear models and ways forward here benjaminmoll.com/challenge/

The excessive focus on linearized solutions to HA models is a bit like the old joke about the drunk who is looking for a key under a lamppost because that's where the light is.

More discussion of why we need non-linear models and ways forward here benjaminmoll.com/challenge/

February 17, 2025 at 9:46 AM

I couldn't agree more!

The excessive focus on linearized solutions to HA models is a bit like the old joke about the drunk who is looking for a key under a lamppost because that's where the light is.

More discussion of why we need non-linear models and ways forward here benjaminmoll.com/challenge/

The excessive focus on linearized solutions to HA models is a bit like the old joke about the drunk who is looking for a key under a lamppost because that's where the light is.

More discussion of why we need non-linear models and ways forward here benjaminmoll.com/challenge/