Bakou Mertens

@bakoumertens.bsky.social

Econ PhD student @Ghent University.

Working with firm-level data on corporate finance without the self-serving blinds.

=> Corporate financialization, inequality and climate, but Interested in macro in general. Blogging at https://bakoumertens.quarto.pub

Working with firm-level data on corporate finance without the self-serving blinds.

=> Corporate financialization, inequality and climate, but Interested in macro in general. Blogging at https://bakoumertens.quarto.pub

Pinned

When shareholder power kicks in: corporate financialization as ratchet behaviour and sticky payouts

Abstract. The rise of payout ratios has been ascribed by financialization scholars to shareholder value orientation (SVO), a governance practice associated

doi.org

My first paper is out in Socio-Economic Review!

doi.org/10.1093/ser/...

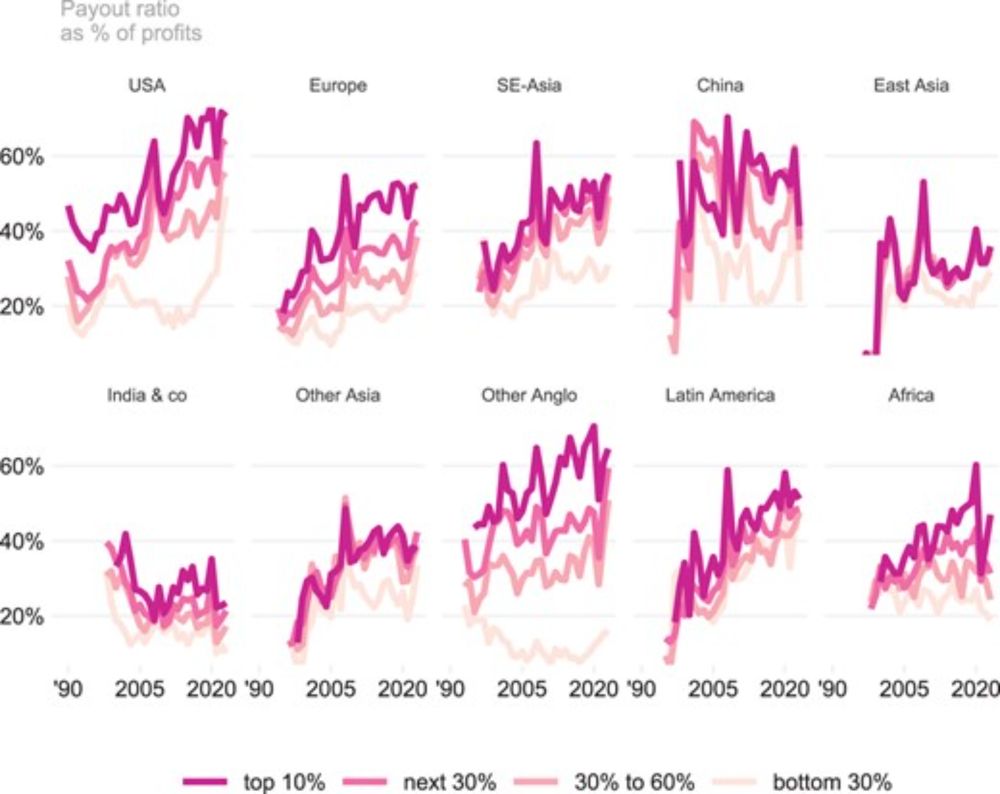

Using firm-level data on all stock listed firms in the world I show that it is not the growth of shareholder remunerations that causes rising payout ratios, but precisely their inability to fall, their downward rigidity.

doi.org/10.1093/ser/...

Using firm-level data on all stock listed firms in the world I show that it is not the growth of shareholder remunerations that causes rising payout ratios, but precisely their inability to fall, their downward rigidity.

My first paper has a volume number!!

crux: "heads, shareholders win, tails, society loses"

shareholders do not share in the costs of negative profit shocks. This ratchets up payout ratio persistently over the ensuing years.

1/n

crux: "heads, shareholders win, tails, society loses"

shareholders do not share in the costs of negative profit shocks. This ratchets up payout ratio persistently over the ensuing years.

1/n

When shareholder power kicks in: corporate financialization as ratchet behaviour and sticky payouts, by @bakoumertens.bsky.social academic.oup.com/ser/article-...

When shareholder power kicks in: corporate financialization as ratchet behaviour and sticky payouts

Abstract. The rise of payout ratios has been ascribed by financialization scholars to shareholder value orientation (SVO), a governance practice associated

academic.oup.com

January 27, 2025 at 8:24 AM

My first paper has a volume number!!

crux: "heads, shareholders win, tails, society loses"

shareholders do not share in the costs of negative profit shocks. This ratchets up payout ratio persistently over the ensuing years.

1/n

crux: "heads, shareholders win, tails, society loses"

shareholders do not share in the costs of negative profit shocks. This ratchets up payout ratio persistently over the ensuing years.

1/n

In this little piece, I ask a little provocatively whether t shareholder is more akin to a knightly investor, lazy rentier or bloodsucking parasite. 3 key questions:

1) Aren't we all shareholders?

2) Do shareholders invest in our economy?

3) Is the stock market a source or a drain of funds?

1) Aren't we all shareholders?

2) Do shareholders invest in our economy?

3) Is the stock market a source or a drain of funds?

mooi stuk van @bakoumertens.bsky.social !

De aandeelhouder: investeerder, rentenier of parasiet?

www.sampol.be/2024/04/de-a...

De aandeelhouder: investeerder, rentenier of parasiet?

www.sampol.be/2024/04/de-a...

De aandeelhouder: investeerder, rentenier of parasiet?

Moderne aandeelhouders investeren niet in een bedrijf, ze kopen en verkopen financiële eigendomsrechten zonder dat het bedrijf er baat bij heeft.

www.sampol.be

January 10, 2025 at 9:47 AM

In this little piece, I ask a little provocatively whether t shareholder is more akin to a knightly investor, lazy rentier or bloodsucking parasite. 3 key questions:

1) Aren't we all shareholders?

2) Do shareholders invest in our economy?

3) Is the stock market a source or a drain of funds?

1) Aren't we all shareholders?

2) Do shareholders invest in our economy?

3) Is the stock market a source or a drain of funds?

Reposted by Bakou Mertens

Funny how 5 years ago we had all these debates about wealth taxation, and a big argument was that billionaires don't have that much power really—and right after that Musk bought Twitter for $44B, used it to get Trump win, and now to prop up the global neo-nazi movement ¯\_(ツ)_/¯

December 20, 2024 at 8:09 PM

Funny how 5 years ago we had all these debates about wealth taxation, and a big argument was that billionaires don't have that much power really—and right after that Musk bought Twitter for $44B, used it to get Trump win, and now to prop up the global neo-nazi movement ¯\_(ツ)_/¯

Reposted by Bakou Mertens

new working paper ⬇️💰

the assumption that shareholders are the key investors in business innovation is simply taken as a given

it's past time to abandon this myth: shareholders of corporations are not always, or even often, “investors.”

the assumption that shareholders are the key investors in business innovation is simply taken as a given

it's past time to abandon this myth: shareholders of corporations are not always, or even often, “investors.”

NEW: Shareholders should not get exclusive power in corporate governance.

@lenorepalladino.bsky.social & Harrison Karlewicz argue we need to abandon the myth that shareholding and investing go hand in hand 🤝 and rethink the regulation of financial markets: rooseveltinstitute.org/publications...

@lenorepalladino.bsky.social & Harrison Karlewicz argue we need to abandon the myth that shareholding and investing go hand in hand 🤝 and rethink the regulation of financial markets: rooseveltinstitute.org/publications...

November 21, 2024 at 6:10 PM

new working paper ⬇️💰

the assumption that shareholders are the key investors in business innovation is simply taken as a given

it's past time to abandon this myth: shareholders of corporations are not always, or even often, “investors.”

the assumption that shareholders are the key investors in business innovation is simply taken as a given

it's past time to abandon this myth: shareholders of corporations are not always, or even often, “investors.”

Reposted by Bakou Mertens

In de afgelopen neoliberale decennia ontwikkelden bedrijven een obsessie voor aandeelhoudersbelangen, ten koste van werknemers en gemeenschap. De Belgische arbeidssocioloog Isabelle Ferreras wil terug naar democratisch ondernemen.

Isabelle Ferreras pleit voor het einde van de neoliberale onderneming. ‘Werk is politiek’

In de afgelopen neoliberale decennia ontwikkelden bedrijven een obsessie voor aandeelhoudersbelangen, ten koste van werknemers en gemeenschap. De Belgische arbeidssocioloog Isabelle Ferreras wil…

buff.ly

October 21, 2024 at 6:10 AM

In de afgelopen neoliberale decennia ontwikkelden bedrijven een obsessie voor aandeelhoudersbelangen, ten koste van werknemers en gemeenschap. De Belgische arbeidssocioloog Isabelle Ferreras wil terug naar democratisch ondernemen.

My first paper is out in Socio-Economic Review!

doi.org/10.1093/ser/...

Using firm-level data on all stock listed firms in the world I show that it is not the growth of shareholder remunerations that causes rising payout ratios, but precisely their inability to fall, their downward rigidity.

doi.org/10.1093/ser/...

Using firm-level data on all stock listed firms in the world I show that it is not the growth of shareholder remunerations that causes rising payout ratios, but precisely their inability to fall, their downward rigidity.

When shareholder power kicks in: corporate financialization as ratchet behaviour and sticky payouts

Abstract. The rise of payout ratios has been ascribed by financialization scholars to shareholder value orientation (SVO), a governance practice associated

doi.org

October 2, 2024 at 8:16 AM

My first paper is out in Socio-Economic Review!

doi.org/10.1093/ser/...

Using firm-level data on all stock listed firms in the world I show that it is not the growth of shareholder remunerations that causes rising payout ratios, but precisely their inability to fall, their downward rigidity.

doi.org/10.1093/ser/...

Using firm-level data on all stock listed firms in the world I show that it is not the growth of shareholder remunerations that causes rising payout ratios, but precisely their inability to fall, their downward rigidity.