Bakou Mertens

@bakoumertens.bsky.social

Econ PhD student @Ghent University.

Working with firm-level data on corporate finance without the self-serving blinds.

=> Corporate financialization, inequality and climate, but Interested in macro in general. Blogging at https://bakoumertens.quarto.pub

Working with firm-level data on corporate finance without the self-serving blinds.

=> Corporate financialization, inequality and climate, but Interested in macro in general. Blogging at https://bakoumertens.quarto.pub

January 29, 2025 at 7:22 AM

In follow-up work that I will submit for review in coming week, I ask what the consequences are for other stakeholders?

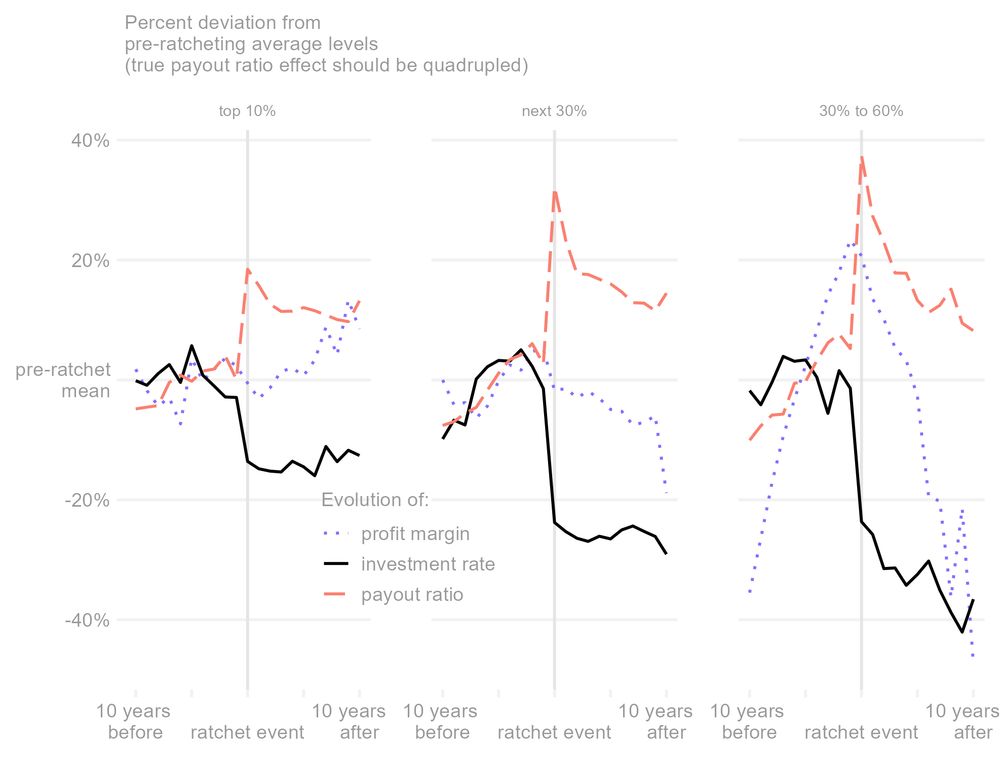

sneak peak: ratchet events cause persistently: 1) higher payout ratios, 2) higher indebtedness and 3) lower investments.

Hopefully coming soonish!

sneak peak: ratchet events cause persistently: 1) higher payout ratios, 2) higher indebtedness and 3) lower investments.

Hopefully coming soonish!

January 27, 2025 at 8:24 AM

In follow-up work that I will submit for review in coming week, I ask what the consequences are for other stakeholders?

sneak peak: ratchet events cause persistently: 1) higher payout ratios, 2) higher indebtedness and 3) lower investments.

Hopefully coming soonish!

sneak peak: ratchet events cause persistently: 1) higher payout ratios, 2) higher indebtedness and 3) lower investments.

Hopefully coming soonish!

2) At the firm level each ratchet event (falling profits, steady payouts) persistently raises the payout ratio for a decade (staggered DiD)

January 27, 2025 at 8:24 AM

2) At the firm level each ratchet event (falling profits, steady payouts) persistently raises the payout ratio for a decade (staggered DiD)

Payouts fractionally adjust upwards in good times but are downward rigid in bad times - just like a ratchet.

What does the data say?

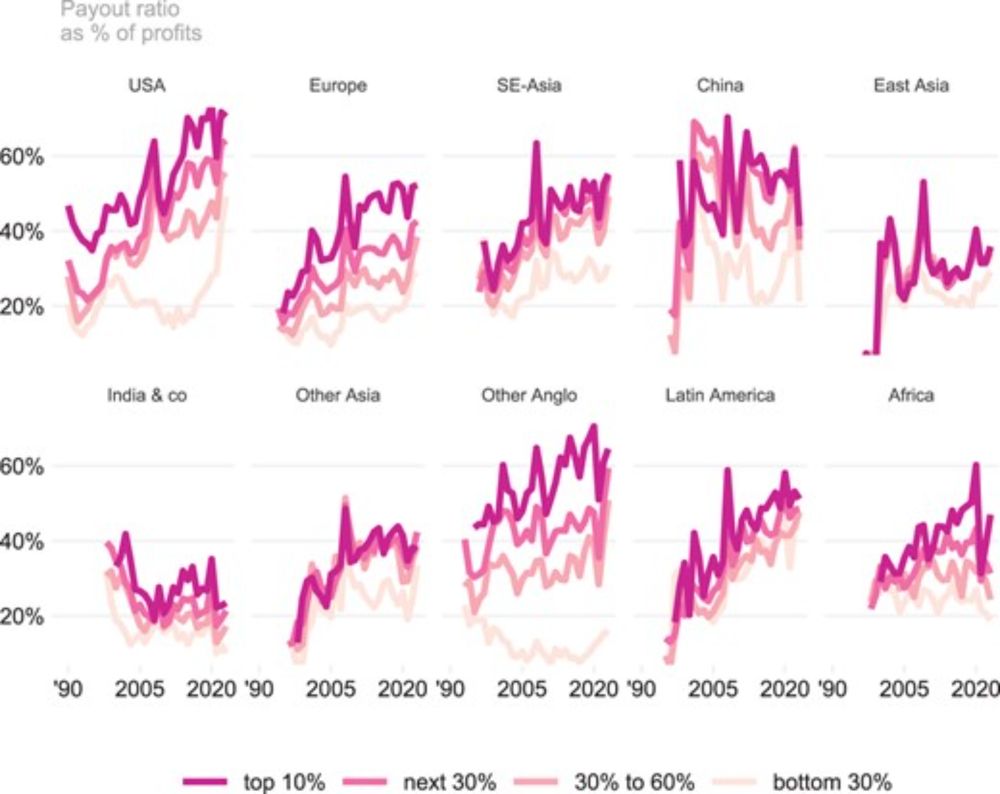

1) Aggregate payout ratios are structured along the frequency of ratchet behaviour, across size, sector & region (although differences do exist)

What does the data say?

1) Aggregate payout ratios are structured along the frequency of ratchet behaviour, across size, sector & region (although differences do exist)

January 27, 2025 at 8:24 AM

Payouts fractionally adjust upwards in good times but are downward rigid in bad times - just like a ratchet.

What does the data say?

1) Aggregate payout ratios are structured along the frequency of ratchet behaviour, across size, sector & region (although differences do exist)

What does the data say?

1) Aggregate payout ratios are structured along the frequency of ratchet behaviour, across size, sector & region (although differences do exist)

Payout ratios ⬆️not because of some shareholder bonanza, but rather because fluctuations in profits are not met by fluctuations in shareholder income.

=> Upward trend in both payout ratios and profits can emerge despite falling payout ratios whenever profits rise!

=> Upward trend in both payout ratios and profits can emerge despite falling payout ratios whenever profits rise!

January 27, 2025 at 8:24 AM

Payout ratios ⬆️not because of some shareholder bonanza, but rather because fluctuations in profits are not met by fluctuations in shareholder income.

=> Upward trend in both payout ratios and profits can emerge despite falling payout ratios whenever profits rise!

=> Upward trend in both payout ratios and profits can emerge despite falling payout ratios whenever profits rise!

And here is a sneak peak in my next paper on the consequences for investments:

January 10, 2025 at 9:47 AM

And here is a sneak peak in my next paper on the consequences for investments:

In my actual research I look into how exactly that happens and what the consequences are. I find that shareholder remunerations are downward sticky in hard times and that that it is when resources become scarce that shareholder power manifests.

See a thread here: bsky.app/profile/bako...

See a thread here: bsky.app/profile/bako...

My first paper is out in Socio-Economic Review!

doi.org/10.1093/ser/...

Using firm-level data on all stock listed firms in the world I show that it is not the growth of shareholder remunerations that causes rising payout ratios, but precisely their inability to fall, their downward rigidity.

doi.org/10.1093/ser/...

Using firm-level data on all stock listed firms in the world I show that it is not the growth of shareholder remunerations that causes rising payout ratios, but precisely their inability to fall, their downward rigidity.

When shareholder power kicks in: corporate financialization as ratchet behaviour and sticky payouts

Abstract. The rise of payout ratios has been ascribed by financialization scholars to shareholder value orientation (SVO), a governance practice associated

doi.org

January 10, 2025 at 9:47 AM

In my actual research I look into how exactly that happens and what the consequences are. I find that shareholder remunerations are downward sticky in hard times and that that it is when resources become scarce that shareholder power manifests.

See a thread here: bsky.app/profile/bako...

See a thread here: bsky.app/profile/bako...

3) Over the recent decades, shareholders have been increasing their claim over firm resources, while the stock market serves less a a source of funds for new or existing companies.

January 10, 2025 at 9:47 AM

3) Over the recent decades, shareholders have been increasing their claim over firm resources, while the stock market serves less a a source of funds for new or existing companies.

2) this question is answered by the excellent @lenorepalladino.bsky.social for @rooseveltinstitute.org, read it there (spoiler: mostly not!) : rooseveltinstitute.org/publications...

The Myth That Shareholders Are Always Investors: Challenging the Paradigm of Shareholder Primacy - Roosevelt Institute

In a new analysis, Lenore Palladino and Harrison Karlewicz argue that shareholders of corporations are not always, or even often, “investors” in any meaningful sense.

rooseveltinstitute.org

January 10, 2025 at 9:47 AM

2) this question is answered by the excellent @lenorepalladino.bsky.social for @rooseveltinstitute.org, read it there (spoiler: mostly not!) : rooseveltinstitute.org/publications...

1) Stock wealth in Belgium is not negligible, but what crucially matters is its distribution. Wealth is very unequally distributed, financial wealth already much more so but stock wealth is the item that is most unequal, certainly in Belgium where we have a pay as you go pension system

January 10, 2025 at 9:47 AM

1) Stock wealth in Belgium is not negligible, but what crucially matters is its distribution. Wealth is very unequally distributed, financial wealth already much more so but stock wealth is the item that is most unequal, certainly in Belgium where we have a pay as you go pension system

Daarbij is cruciaal: niet de toename van dividenden of buybacks verdringt investeringen, maar juist hun neerwaartse rigiditeit! Als bedrijf het tijdelijk moeilijk heeft weigeren aandeelhouders te delen in de klappen, waardoor bedrijf genoodzaakt is te snijden in investeringen en/of schuld aan t gaan

January 10, 2025 at 9:20 AM

Daarbij is cruciaal: niet de toename van dividenden of buybacks verdringt investeringen, maar juist hun neerwaartse rigiditeit! Als bedrijf het tijdelijk moeilijk heeft weigeren aandeelhouders te delen in de klappen, waardoor bedrijf genoodzaakt is te snijden in investeringen en/of schuld aan t gaan

Bedankt Rodrigo! Misschien een beetje provocerend geformuleerd, maar de aandeelhouder heeft in toenemende mate inderdaad iets parasitairs. In paper (net af) toon ik aan hoe bedrijven herverdelen van investeringen naar aandeelhouders, waarbij ze onze economie vandaag en in toekomst schaden

January 10, 2025 at 9:20 AM

Bedankt Rodrigo! Misschien een beetje provocerend geformuleerd, maar de aandeelhouder heeft in toenemende mate inderdaad iets parasitairs. In paper (net af) toon ik aan hoe bedrijven herverdelen van investeringen naar aandeelhouders, waarbij ze onze economie vandaag en in toekomst schaden

I mean, inflation is not all bad and shouldn't be fought at all costs. Depending on 1) the source 2) strength of Labour unions and Labour markets and 3) the policy reaction, it could be a force for good. Updating our toolbox to fight inflation as Isabella has been arguing for years is still crucial!

November 13, 2024 at 6:48 AM

I mean, inflation is not all bad and shouldn't be fought at all costs. Depending on 1) the source 2) strength of Labour unions and Labour markets and 3) the policy reaction, it could be a force for good. Updating our toolbox to fight inflation as Isabella has been arguing for years is still crucial!

Very interesting work! However I am bit reluctant to amplify inflation aversion in general, given that coordinated Wage driven inflation might be exactly what we need at this point (definitely in Germany) and amping up inflation aversion legitimises lab market slack, high int rates, schw. Null,...

November 13, 2024 at 6:45 AM

Very interesting work! However I am bit reluctant to amplify inflation aversion in general, given that coordinated Wage driven inflation might be exactly what we need at this point (definitely in Germany) and amping up inflation aversion legitimises lab market slack, high int rates, schw. Null,...

This likely has real consequences. When firms maintain stable payouts despite declining profits, they must either resort to cutting investments, R&D expenditures, or labor costs or to taking on higher levels of (unproductive) debt.

October 2, 2024 at 8:26 AM

This likely has real consequences. When firms maintain stable payouts despite declining profits, they must either resort to cutting investments, R&D expenditures, or labor costs or to taking on higher levels of (unproductive) debt.

Payouts fractionally adjust upwards in good times but are downward rigid in bad times - just like a ratchet.

1) Aggregate payout ratios are structured along the frequency of ratchet behaviour

2) At the firm level each ratchet event persistently raises the payout ratio for a decade (staggered DiD)

1) Aggregate payout ratios are structured along the frequency of ratchet behaviour

2) At the firm level each ratchet event persistently raises the payout ratio for a decade (staggered DiD)

October 2, 2024 at 8:25 AM

Payouts fractionally adjust upwards in good times but are downward rigid in bad times - just like a ratchet.

1) Aggregate payout ratios are structured along the frequency of ratchet behaviour

2) At the firm level each ratchet event persistently raises the payout ratio for a decade (staggered DiD)

1) Aggregate payout ratios are structured along the frequency of ratchet behaviour

2) At the firm level each ratchet event persistently raises the payout ratio for a decade (staggered DiD)

Short summary: bakoumertens.quarto.pub/bakoumertens...

People tend to focus on large increases in dividends or share repurchases (payouts), but I show that it is not rising payouts that should attract our attention, but rather their inability to fall.

People tend to focus on large increases in dividends or share repurchases (payouts), but I show that it is not rising payouts that should attract our attention, but rather their inability to fall.

Bakou Mertens - When shareholder power kicks in

Corporate financialization manifests as ratchet behaviour, where shareholders refuse to yield ground when profits decrease. It is the downward rigidity of shareholder remuneration that ratchets up pay...

bakoumertens.quarto.pub

October 2, 2024 at 8:20 AM

Short summary: bakoumertens.quarto.pub/bakoumertens...

People tend to focus on large increases in dividends or share repurchases (payouts), but I show that it is not rising payouts that should attract our attention, but rather their inability to fall.

People tend to focus on large increases in dividends or share repurchases (payouts), but I show that it is not rising payouts that should attract our attention, but rather their inability to fall.