@ttunguz.bsky.social

Two revelations this week have shaken the narrative in AI : Nvidia’s earnings & this tweet about Gemini.

The AI industry spent 2025 convinced that pre-training scaling laws had hit a wall. Models weren’t improving just from adding more compute during training.

The AI industry spent 2025 convinced that pre-training scaling laws had hit a wall. Models weren’t improving just from adding more compute during training.

November 20, 2025 at 8:17 PM

Two revelations this week have shaken the narrative in AI : Nvidia’s earnings & this tweet about Gemini.

The AI industry spent 2025 convinced that pre-training scaling laws had hit a wall. Models weren’t improving just from adding more compute during training.

The AI industry spent 2025 convinced that pre-training scaling laws had hit a wall. Models weren’t improving just from adding more compute during training.

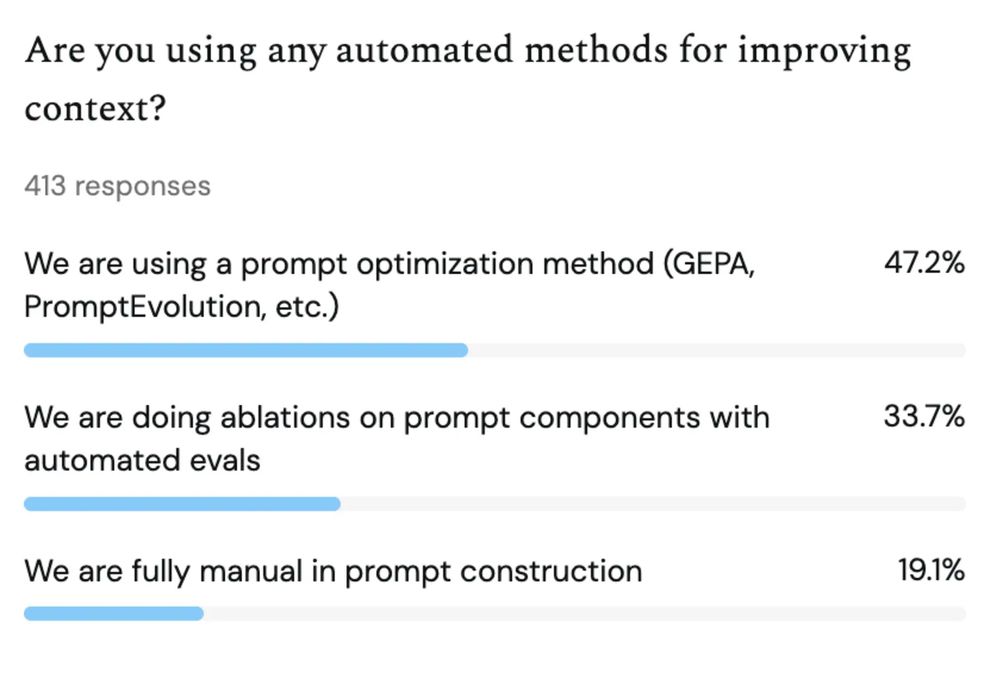

88% use automated methods for improving context. Yet it remains the #1 pain point in deploying AI products. This gap between tooling adoption & problem resolution points to a fundamental challenge.

November 17, 2025 at 11:30 PM

88% use automated methods for improving context. Yet it remains the #1 pain point in deploying AI products. This gap between tooling adoption & problem resolution points to a fundamental challenge.

Synthetic data powers evaluation more than training. 65% use synthetic data for eval generation versus 24% for fine-tuning. This points to a near-term surge in eval-data marketplaces, scenario libraries, & failure-mode corpora before synthetic training data scales up.

November 17, 2025 at 11:30 PM

Synthetic data powers evaluation more than training. 65% use synthetic data for eval generation versus 24% for fine-tuning. This points to a near-term surge in eval-data marketplaces, scenario libraries, & failure-mode corpora before synthetic training data scales up.

Agents in the field are systems operators, not chat interfaces. We thought agents would mostly call APIs. Instead, 72.5% connect to databases. 61% to web search. 56% to memory systems & file systems. 47% to code interpreters.

November 17, 2025 at 11:30 PM

Agents in the field are systems operators, not chat interfaces. We thought agents would mostly call APIs. Instead, 72.5% connect to databases. 61% to web search. 56% to memory systems & file systems. 47% to code interpreters.

70% of teams use open source models in some capacity. 48% describe their strategy as mostly open. 22% commit to only open. Just 11% stay purely proprietary.

November 17, 2025 at 11:30 PM

70% of teams use open source models in some capacity. 48% describe their strategy as mostly open. 22% commit to only open. Just 11% stay purely proprietary.

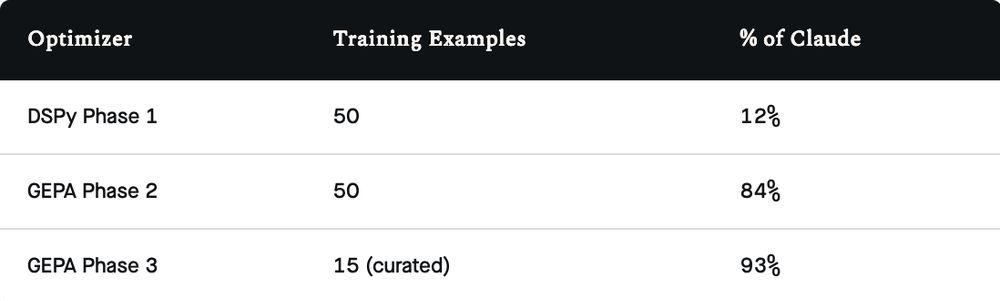

Combined, we improved from a 12% Claude match rate to 93% in three iterations by increasing the data volume to cover different scenarios :

November 13, 2025 at 10:22 PM

Combined, we improved from a 12% Claude match rate to 93% in three iterations by increasing the data volume to cover different scenarios :

Could a large model teach a smaller one to call the right tools?

The answer is yes, or at least yes in our case. Here’s our current effort :

The answer is yes, or at least yes in our case. Here’s our current effort :

November 13, 2025 at 10:22 PM

Could a large model teach a smaller one to call the right tools?

The answer is yes, or at least yes in our case. Here’s our current effort :

The answer is yes, or at least yes in our case. Here’s our current effort :

I typed ultrathink to solve a particularly challenging coding problem, knowing the rainbow colors of the word was playing with digital fire.

November 12, 2025 at 9:51 PM

I typed ultrathink to solve a particularly challenging coding problem, knowing the rainbow colors of the word was playing with digital fire.

By Monday lunch, I had burned through my Claude code credits. I’d been warned ; damn the budget, full prompting ahead.

November 12, 2025 at 9:51 PM

By Monday lunch, I had burned through my Claude code credits. I’d been warned ; damn the budget, full prompting ahead.

Net dollar retention underpins this growth, combined with accelerating new customer account acquisition. One of the biggest changes in the last five quarters is terrific cross-selling across an increasingly large product suite.

November 10, 2025 at 6:43 PM

Net dollar retention underpins this growth, combined with accelerating new customer account acquisition. One of the biggest changes in the last five quarters is terrific cross-selling across an increasingly large product suite.

Datadog is becoming a platform company, & its Q3 2025 results underscore how successful this transition is. If nothing else, the consistency around 25% growth for the last 12 quarters exemplifies this point.

November 10, 2025 at 6:43 PM

Datadog is becoming a platform company, & its Q3 2025 results underscore how successful this transition is. If nothing else, the consistency around 25% growth for the last 12 quarters exemplifies this point.

To match the railroad era’s 6% of GDP, AI spending would need to reach $2.1T per year by 2030 (6% of projected $35.4T GDP), a 320% increase from today’s $500B. That would require Google, Meta, OpenAI, & Microsoft each investing $500-700B per year, a 5-7x increase from today’s levels.

November 6, 2025 at 11:41 PM

To match the railroad era’s 6% of GDP, AI spending would need to reach $2.1T per year by 2030 (6% of projected $35.4T GDP), a 320% increase from today’s $500B. That would require Google, Meta, OpenAI, & Microsoft each investing $500-700B per year, a 5-7x increase from today’s levels.

Companies like Microsoft, Google, & Meta are investing $140B, $92B, & $71B respectively in data centers & GPUs. OpenAI plans to spend $295B in 2030 alone.

If we assume OpenAI represents 30% of the market, total AI infrastructure spending would reach $983B annually by 2030, or 2.8% of GDP.

If we assume OpenAI represents 30% of the market, total AI infrastructure spending would reach $983B annually by 2030, or 2.8% of GDP.

November 6, 2025 at 11:41 PM

Companies like Microsoft, Google, & Meta are investing $140B, $92B, & $71B respectively in data centers & GPUs. OpenAI plans to spend $295B in 2030 alone.

If we assume OpenAI represents 30% of the market, total AI infrastructure spending would reach $983B annually by 2030, or 2.8% of GDP.

If we assume OpenAI represents 30% of the market, total AI infrastructure spending would reach $983B annually by 2030, or 2.8% of GDP.

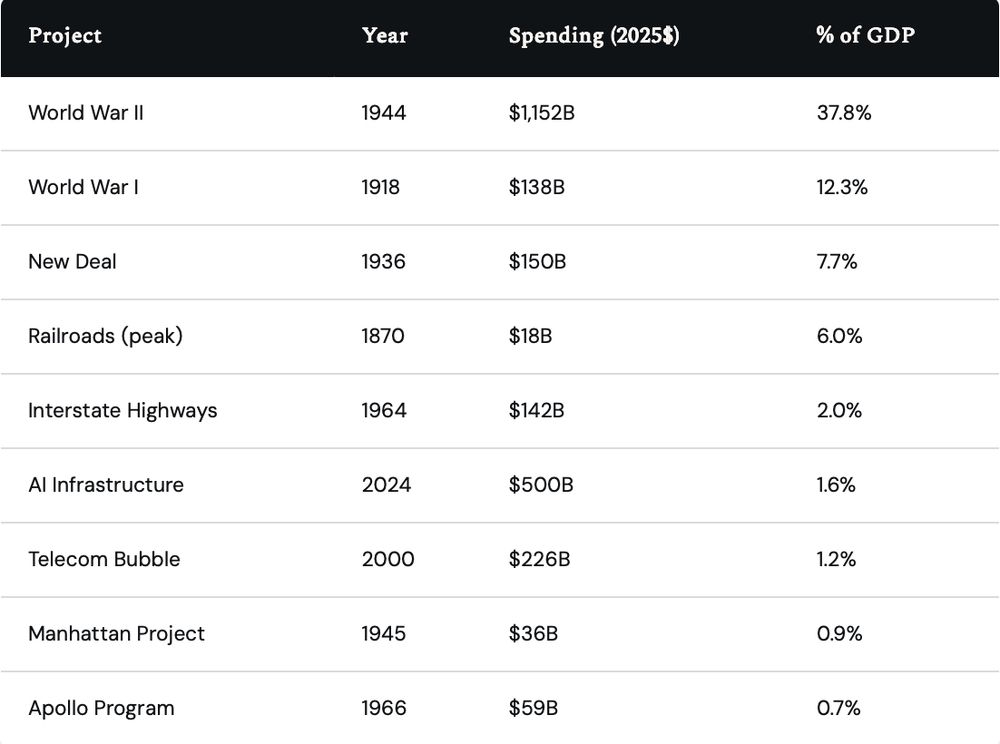

World War II dwarfs everything else at 37.8% of GDP. World War I consumed 12.3%. The New Deal peaked at 7.7%. Railroads during the Gilded Age reached 6.0%.

AI infrastructure today sits at 1.6%, just above the telecom bubble’s 1.2% & well below the major historical mobilizations.

AI infrastructure today sits at 1.6%, just above the telecom bubble’s 1.2% & well below the major historical mobilizations.

November 6, 2025 at 11:41 PM

World War II dwarfs everything else at 37.8% of GDP. World War I consumed 12.3%. The New Deal peaked at 7.7%. Railroads during the Gilded Age reached 6.0%.

AI infrastructure today sits at 1.6%, just above the telecom bubble’s 1.2% & well below the major historical mobilizations.

AI infrastructure today sits at 1.6%, just above the telecom bubble’s 1.2% & well below the major historical mobilizations.

Source : ClickBench

As the amount of data expands & I process more technology podcasts every day, I’m sure I’ll need a data lake. At that point, I can migrate to DuckLake.

Small data becomes big data faster than you know it.

As the amount of data expands & I process more technology podcasts every day, I’m sure I’ll need a data lake. At that point, I can migrate to DuckLake.

Small data becomes big data faster than you know it.

October 31, 2025 at 11:39 PM

Source : ClickBench

As the amount of data expands & I process more technology podcasts every day, I’m sure I’ll need a data lake. At that point, I can migrate to DuckLake.

Small data becomes big data faster than you know it.

As the amount of data expands & I process more technology podcasts every day, I’m sure I’ll need a data lake. At that point, I can migrate to DuckLake.

Small data becomes big data faster than you know it.

Source : ClickBench

Aside from ease of use, there are real price-performance advantages. MotherDuck systems are two to four times faster than a Snowflake 3XL & from a tenth to a hundredth of the price.

Aside from ease of use, there are real price-performance advantages. MotherDuck systems are two to four times faster than a Snowflake 3XL & from a tenth to a hundredth of the price.

October 31, 2025 at 11:39 PM

Source : ClickBench

Aside from ease of use, there are real price-performance advantages. MotherDuck systems are two to four times faster than a Snowflake 3XL & from a tenth to a hundredth of the price.

Aside from ease of use, there are real price-performance advantages. MotherDuck systems are two to four times faster than a Snowflake 3XL & from a tenth to a hundredth of the price.

Now, in the small hours, 10 robots listen & summarize podcasts for me while I sleep.

As I collect more & more podcast information, my data has grown. I’m using a larger instance of MotherDuck.

As I collect more & more podcast information, my data has grown. I’m using a larger instance of MotherDuck.

October 31, 2025 at 11:39 PM

Now, in the small hours, 10 robots listen & summarize podcasts for me while I sleep.

As I collect more & more podcast information, my data has grown. I’m using a larger instance of MotherDuck.

As I collect more & more podcast information, my data has grown. I’m using a larger instance of MotherDuck.

But then the data started to grow, & I wanted the podcast processor to run by itself. I changed two little letters, & the database moved to the cloud :

October 31, 2025 at 11:39 PM

But then the data started to grow, & I wanted the podcast processor to run by itself. I changed two little letters, & the database moved to the cloud :

Cash Position vs Annualized Capex

Both companies are spending at or above their cash positions on AI infrastructure. Microsoft is committing 137% of its cash reserves to annualized capex, while Google’s capex represents 93% of its cash position.

Both companies are spending at or above their cash positions on AI infrastructure. Microsoft is committing 137% of its cash reserves to annualized capex, while Google’s capex represents 93% of its cash position.

October 30, 2025 at 4:21 PM

Cash Position vs Annualized Capex

Both companies are spending at or above their cash positions on AI infrastructure. Microsoft is committing 137% of its cash reserves to annualized capex, while Google’s capex represents 93% of its cash position.

Both companies are spending at or above their cash positions on AI infrastructure. Microsoft is committing 137% of its cash reserves to annualized capex, while Google’s capex represents 93% of its cash position.

Microsoft & Google both announced earnings yesterday, & the scale of AI adoption remains staggering. The infrastructure businesses are growing at accelerating growth rates that are the envy of businesses one-hundredth the size.

October 30, 2025 at 4:21 PM

Microsoft & Google both announced earnings yesterday, & the scale of AI adoption remains staggering. The infrastructure businesses are growing at accelerating growth rates that are the envy of businesses one-hundredth the size.

The scarcity of hyper-growth companies in 2025 tells its own story. Public SaaS companies have matured. The median company in our dataset grows at 13.7% annually, with a median multiple of 5.5x.

October 27, 2025 at 7:19 PM

The scarcity of hyper-growth companies in 2025 tells its own story. Public SaaS companies have matured. The median company in our dataset grows at 13.7% annually, with a median multiple of 5.5x.

Even here, AI is the story, with AI SaaS companies seeing different valuation correlates : revenue growth. Meanwhile, non-AI SaaS companies are valued more broadly with efficiency metrics included.

October 27, 2025 at 7:19 PM

Even here, AI is the story, with AI SaaS companies seeing different valuation correlates : revenue growth. Meanwhile, non-AI SaaS companies are valued more broadly with efficiency metrics included.

As the world follows every whisper & rumor from AI, what has happened to public SaaS?

The answer is not much! All the fun is in the private markets.

Multiples haven’t moved outside of a narrow band since the post-Covid crash in 2022.

The answer is not much! All the fun is in the private markets.

Multiples haven’t moved outside of a narrow band since the post-Covid crash in 2022.

October 27, 2025 at 7:19 PM

As the world follows every whisper & rumor from AI, what has happened to public SaaS?

The answer is not much! All the fun is in the private markets.

Multiples haven’t moved outside of a narrow band since the post-Covid crash in 2022.

The answer is not much! All the fun is in the private markets.

Multiples haven’t moved outside of a narrow band since the post-Covid crash in 2022.

Polymarket predicts Google will have the best AI model at the end of the year. At the beginning of 2024, Google was far behind. The most advanced companies in AI are still jockeying for position & so are startups.

October 23, 2025 at 7:23 PM

Polymarket predicts Google will have the best AI model at the end of the year. At the beginning of 2024, Google was far behind. The most advanced companies in AI are still jockeying for position & so are startups.

Today, AI can create the plan, but isn’t yet able to develop the reward functions. People do this, much as we developed features 15 years ago.

Will we see an AutoRL? Not for a while. The techniques for RL are still up for debate. Andrej Karpathy highlighted the debate in a recent podcast.

Will we see an AutoRL? Not for a while. The techniques for RL are still up for debate. Andrej Karpathy highlighted the debate in a recent podcast.

October 20, 2025 at 7:19 PM

Today, AI can create the plan, but isn’t yet able to develop the reward functions. People do this, much as we developed features 15 years ago.

Will we see an AutoRL? Not for a while. The techniques for RL are still up for debate. Andrej Karpathy highlighted the debate in a recent podcast.

Will we see an AutoRL? Not for a while. The techniques for RL are still up for debate. Andrej Karpathy highlighted the debate in a recent podcast.