Shane Oliver

@shaneoliver.bsky.social

Chief Economist & Head of Inv Strategy, AMP. Into boats, pop music, nature, economics, investing, my family…& being nice. I don’t solicit funds or spruik trading schemes.

Australian business investment surged 6.4%qoq in Sept qtr with bldings +2.1%q & equipment +11.5%q on the back of surging IT investment in data centres & transport inv (aircraft). We now expect Sept qtr GDP growth of 0.7%q/2.2%y.

Capex plans for 2025-26 are now solid at +7.1%y

Capex plans for 2025-26 are now solid at +7.1%y

November 27, 2025 at 3:07 AM

Australian business investment surged 6.4%qoq in Sept qtr with bldings +2.1%q & equipment +11.5%q on the back of surging IT investment in data centres & transport inv (aircraft). We now expect Sept qtr GDP growth of 0.7%q/2.2%y.

Capex plans for 2025-26 are now solid at +7.1%y

Capex plans for 2025-26 are now solid at +7.1%y

..regarding the APRA move to limit hi DTI loans to 20% of each bank’s lending from 1 Feb…the aggregate ratio at present is well below that suggesting it may be a while before it has much impact. It’s really a shot across the bows of the lenders not to let things heat up too much

November 27, 2025 at 12:19 AM

..regarding the APRA move to limit hi DTI loans to 20% of each bank’s lending from 1 Feb…the aggregate ratio at present is well below that suggesting it may be a while before it has much impact. It’s really a shot across the bows of the lenders not to let things heat up too much

As foreshadowed APRA will cap high debt to income lending from 1 Feb at 20% of home loans. While APRA says the aggregate is below that the move is pre-emptive & designed to cool investor activity before it gets too hot. This & less rate cuts will constrain home price grth next yr (APRA statement)

November 26, 2025 at 10:07 PM

As foreshadowed APRA will cap high debt to income lending from 1 Feb at 20% of home loans. While APRA says the aggregate is below that the move is pre-emptive & designed to cool investor activity before it gets too hot. This & less rate cuts will constrain home price grth next yr (APRA statement)

US initial jobless claims -6k and remaining low, but continuing claims +7k with rising trend…“low firing but low hiring”

Sep durable goods orders +0.5%mom (as exp) but capital goods orders & shipments ex aircraft and defence both up 0.9%mom and trending higher

(Bloomberg chart)

Sep durable goods orders +0.5%mom (as exp) but capital goods orders & shipments ex aircraft and defence both up 0.9%mom and trending higher

(Bloomberg chart)

November 26, 2025 at 8:44 PM

US initial jobless claims -6k and remaining low, but continuing claims +7k with rising trend…“low firing but low hiring”

Sep durable goods orders +0.5%mom (as exp) but capital goods orders & shipments ex aircraft and defence both up 0.9%mom and trending higher

(Bloomberg chart)

Sep durable goods orders +0.5%mom (as exp) but capital goods orders & shipments ex aircraft and defence both up 0.9%mom and trending higher

(Bloomberg chart)

..and guess where a lot of the inflation is coming from!

Market related price inflation has picked up to 2.8%yoy…

…but prices which are largely govt administered or indexed under govt regulation are up 7.8%yoy

Market related price inflation has picked up to 2.8%yoy…

…but prices which are largely govt administered or indexed under govt regulation are up 7.8%yoy

November 26, 2025 at 2:16 AM

..and guess where a lot of the inflation is coming from!

Market related price inflation has picked up to 2.8%yoy…

…but prices which are largely govt administered or indexed under govt regulation are up 7.8%yoy

Market related price inflation has picked up to 2.8%yoy…

…but prices which are largely govt administered or indexed under govt regulation are up 7.8%yoy

Electricity prices are +37%yoy due to the roll off of state rebates a year ago, but -10%mom as NSW and ACT got catch up Fed rebates. Electricity prices are roughly 21% below where they would be without the rebates. Which means pressure on Fed Gov to extend them beyond this yr

November 26, 2025 at 2:03 AM

Electricity prices are +37%yoy due to the roll off of state rebates a year ago, but -10%mom as NSW and ACT got catch up Fed rebates. Electricity prices are roughly 21% below where they would be without the rebates. Which means pressure on Fed Gov to extend them beyond this yr

Key drivers of the further pick up in annual inflation were electricity (as yr ago rebates dropped out), food, holiday travel (school holiday related) and housing costs starting to hook up again (altho that for rent was due to less Commonwealth rent assistance).

November 26, 2025 at 1:58 AM

Key drivers of the further pick up in annual inflation were electricity (as yr ago rebates dropped out), food, holiday travel (school holiday related) and housing costs starting to hook up again (altho that for rent was due to less Commonwealth rent assistance).

Aust’s new mthly CPI showed another lift to 0%m/3.8%y with new trimmed mean 0.3%m/3.3%y. Goods inflation is well up & there are now more items above 3%y than below 2%y. The chance of another rate cut next yr has taken another hit - but this new data needs to be treated cautiously

November 26, 2025 at 1:51 AM

Aust’s new mthly CPI showed another lift to 0%m/3.8%y with new trimmed mean 0.3%m/3.3%y. Goods inflation is well up & there are now more items above 3%y than below 2%y. The chance of another rate cut next yr has taken another hit - but this new data needs to be treated cautiously

Soft US data

Sep retail sales just +0.2%m, control -0.1%m

Nov consumer confidence -7pts and nearly back to Liberation Day lows. Jobs plentiful/hard to get slightly better but weak

Cotality Sept home prices +0.1%m/1.4%y

Sept core PPI 0.1%m/2.6%y

Adds to case for Dec rate cut

(Bloomberg chart)

Sep retail sales just +0.2%m, control -0.1%m

Nov consumer confidence -7pts and nearly back to Liberation Day lows. Jobs plentiful/hard to get slightly better but weak

Cotality Sept home prices +0.1%m/1.4%y

Sept core PPI 0.1%m/2.6%y

Adds to case for Dec rate cut

(Bloomberg chart)

November 25, 2025 at 10:25 PM

Soft US data

Sep retail sales just +0.2%m, control -0.1%m

Nov consumer confidence -7pts and nearly back to Liberation Day lows. Jobs plentiful/hard to get slightly better but weak

Cotality Sept home prices +0.1%m/1.4%y

Sept core PPI 0.1%m/2.6%y

Adds to case for Dec rate cut

(Bloomberg chart)

Sep retail sales just +0.2%m, control -0.1%m

Nov consumer confidence -7pts and nearly back to Liberation Day lows. Jobs plentiful/hard to get slightly better but weak

Cotality Sept home prices +0.1%m/1.4%y

Sept core PPI 0.1%m/2.6%y

Adds to case for Dec rate cut

(Bloomberg chart)

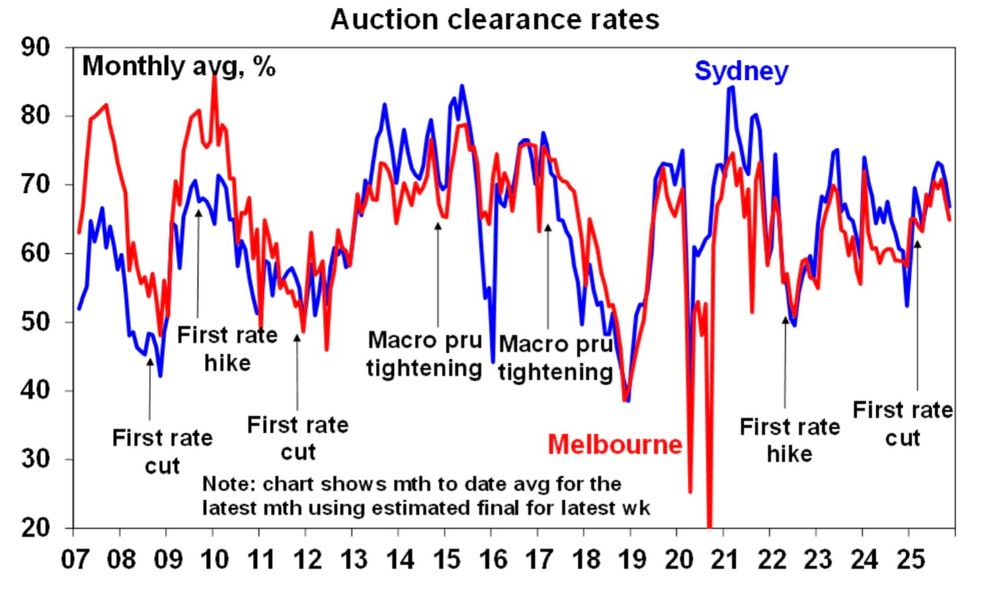

Prelim Domain auction clearances

Syd 64%=final ~62%,Nov avg 60

Mel 65%=final ~63%,Nov avg 61

Clearances slowing with less rate cut optimism & rising listings but looks partly seasonal. Avg clearances fall ~6-7% Aug to Nov. Support remains from the 3 rate cuts & low deposit FHB scheme.

#ausecon

Syd 64%=final ~62%,Nov avg 60

Mel 65%=final ~63%,Nov avg 61

Clearances slowing with less rate cut optimism & rising listings but looks partly seasonal. Avg clearances fall ~6-7% Aug to Nov. Support remains from the 3 rate cuts & low deposit FHB scheme.

#ausecon

November 22, 2025 at 7:51 AM

Prelim Domain auction clearances

Syd 64%=final ~62%,Nov avg 60

Mel 65%=final ~63%,Nov avg 61

Clearances slowing with less rate cut optimism & rising listings but looks partly seasonal. Avg clearances fall ~6-7% Aug to Nov. Support remains from the 3 rate cuts & low deposit FHB scheme.

#ausecon

Syd 64%=final ~62%,Nov avg 60

Mel 65%=final ~63%,Nov avg 61

Clearances slowing with less rate cut optimism & rising listings but looks partly seasonal. Avg clearances fall ~6-7% Aug to Nov. Support remains from the 3 rate cuts & low deposit FHB scheme.

#ausecon

US University of Mich consumer sentiment remaining very weak

1 yr ahead inflation expectations fell to 4.5% from 4.7%

5-10 yr ahead inflation expectations fell to 3.4% from 3.6% (which is getting closer to levels more consistent with the 2% inflation target)

(Bloomberg charts)

1 yr ahead inflation expectations fell to 4.5% from 4.7%

5-10 yr ahead inflation expectations fell to 3.4% from 3.6% (which is getting closer to levels more consistent with the 2% inflation target)

(Bloomberg charts)

November 21, 2025 at 11:12 PM

US University of Mich consumer sentiment remaining very weak

1 yr ahead inflation expectations fell to 4.5% from 4.7%

5-10 yr ahead inflation expectations fell to 3.4% from 3.6% (which is getting closer to levels more consistent with the 2% inflation target)

(Bloomberg charts)

1 yr ahead inflation expectations fell to 4.5% from 4.7%

5-10 yr ahead inflation expectations fell to 3.4% from 3.6% (which is getting closer to levels more consistent with the 2% inflation target)

(Bloomberg charts)

Eurozone shares -1% (-3.1% wk)

US shares +1% (-1.9% wk) as Feds Williams see room for a near term rate cut (mkt back to 60% prob for Dec)

US 10 yr yld -2bp to 4.06%

Oil -1.6% to $58

Gold -0.3% to $4065

Iron ore -0.05% to $104.3

Bitcoin $84.2k

ASX futures +1.1%

$A 0.645 w $US flat

US shares +1% (-1.9% wk) as Feds Williams see room for a near term rate cut (mkt back to 60% prob for Dec)

US 10 yr yld -2bp to 4.06%

Oil -1.6% to $58

Gold -0.3% to $4065

Iron ore -0.05% to $104.3

Bitcoin $84.2k

ASX futures +1.1%

$A 0.645 w $US flat

November 21, 2025 at 11:08 PM

Eurozone shares -1% (-3.1% wk)

US shares +1% (-1.9% wk) as Feds Williams see room for a near term rate cut (mkt back to 60% prob for Dec)

US 10 yr yld -2bp to 4.06%

Oil -1.6% to $58

Gold -0.3% to $4065

Iron ore -0.05% to $104.3

Bitcoin $84.2k

ASX futures +1.1%

$A 0.645 w $US flat

US shares +1% (-1.9% wk) as Feds Williams see room for a near term rate cut (mkt back to 60% prob for Dec)

US 10 yr yld -2bp to 4.06%

Oil -1.6% to $58

Gold -0.3% to $4065

Iron ore -0.05% to $104.3

Bitcoin $84.2k

ASX futures +1.1%

$A 0.645 w $US flat

Australia’s November composite PMI rose to a solid reading of 52.6, with stronger manufacturing & orders in a rising trend. But employment plans fell.

Output prices rose but the trend is down suggesting softer December quarter inflation.

(Macquarie Macro Strategy charts)

Output prices rose but the trend is down suggesting softer December quarter inflation.

(Macquarie Macro Strategy charts)

November 21, 2025 at 3:15 AM

Australia’s November composite PMI rose to a solid reading of 52.6, with stronger manufacturing & orders in a rising trend. But employment plans fell.

Output prices rose but the trend is down suggesting softer December quarter inflation.

(Macquarie Macro Strategy charts)

Output prices rose but the trend is down suggesting softer December quarter inflation.

(Macquarie Macro Strategy charts)

US Nov Phily Fed manufacturing index +11 points to a still soft -1.7pts, with new orders down but employment up. Prices paid rose and are still elevated.

(No clear signal here for Fed)

(No clear signal here for Fed)

November 20, 2025 at 3:33 PM

US Nov Phily Fed manufacturing index +11 points to a still soft -1.7pts, with new orders down but employment up. Prices paid rose and are still elevated.

(No clear signal here for Fed)

(No clear signal here for Fed)

US delayed jobless claims now released and show initial claims little changed, but continuing claims continuing to rise. So no dramatic weakening and it’s still a low firing but low hiring environment.

(EvercoreISI charts)

(EvercoreISI charts)

November 20, 2025 at 3:28 PM

US delayed jobless claims now released and show initial claims little changed, but continuing claims continuing to rise. So no dramatic weakening and it’s still a low firing but low hiring environment.

(EvercoreISI charts)

(EvercoreISI charts)

US Sept payrolls +119k, >exp but payrolls revised down by 33k for months, hrs wkd were flat, unemployment rose unexpectedly to 4.4% & wages growth was unchanged at 3.8%yoy. And the trend in payroll grth is down.

Overall this is neutral for Fed interest rates.

(EvercoreISI charts)

Overall this is neutral for Fed interest rates.

(EvercoreISI charts)

November 20, 2025 at 3:22 PM

US Sept payrolls +119k, >exp but payrolls revised down by 33k for months, hrs wkd were flat, unemployment rose unexpectedly to 4.4% & wages growth was unchanged at 3.8%yoy. And the trend in payroll grth is down.

Overall this is neutral for Fed interest rates.

(EvercoreISI charts)

Overall this is neutral for Fed interest rates.

(EvercoreISI charts)

Nvidia shares up around 5% in after hours trading and US S&P 500 share futures +0.8% as Nvidia beats on earnings, sales and guidance.

(Bloomberg chart)

(Bloomberg chart)

November 19, 2025 at 11:33 PM

Nvidia shares up around 5% in after hours trading and US S&P 500 share futures +0.8% as Nvidia beats on earnings, sales and guidance.

(Bloomberg chart)

(Bloomberg chart)

Australian real wages growth slowed to a crawl last quarter and real wages are still down 6% on 5 years ago (with prices up 23% since December 2020 but wages up just 17%).

Our wages leading indicator still points to a further slowing in wages growth ahead.

Our wages leading indicator still points to a further slowing in wages growth ahead.

November 19, 2025 at 2:33 AM

Australian real wages growth slowed to a crawl last quarter and real wages are still down 6% on 5 years ago (with prices up 23% since December 2020 but wages up just 17%).

Our wages leading indicator still points to a further slowing in wages growth ahead.

Our wages leading indicator still points to a further slowing in wages growth ahead.

Australian wages growth is strongest in utilities, public admin and health and weakest in finance and insurance.

(ABS charts)

(ABS charts)

November 19, 2025 at 1:49 AM

Australian wages growth is strongest in utilities, public admin and health and weakest in finance and insurance.

(ABS charts)

(ABS charts)

..the % of workers seeing a wage rise of 4% or more continues to fall.

Stable wages grth at 3.4%y is consistent with the jobs mkt being balanced, not tight.

Slowing priv wages grth (more important for infl) leaves the door open for another rate cut but the RBA wont be hurrying

Stable wages grth at 3.4%y is consistent with the jobs mkt being balanced, not tight.

Slowing priv wages grth (more important for infl) leaves the door open for another rate cut but the RBA wont be hurrying

November 19, 2025 at 1:47 AM

..the % of workers seeing a wage rise of 4% or more continues to fall.

Stable wages grth at 3.4%y is consistent with the jobs mkt being balanced, not tight.

Slowing priv wages grth (more important for infl) leaves the door open for another rate cut but the RBA wont be hurrying

Stable wages grth at 3.4%y is consistent with the jobs mkt being balanced, not tight.

Slowing priv wages grth (more important for infl) leaves the door open for another rate cut but the RBA wont be hurrying

Aust Sept qtr wages grth flat at 0.8%q/3.4%y (in line with RBA & mkt). The details were on the soft side tho with public sector wages grth elevated at 3.8%yoy but private wages grth slowing to 3.2%yoy & private workers seeing a lower avg rise than a yr ago (3.6% v 3.9% yr ago)..

November 19, 2025 at 1:39 AM

Aust Sept qtr wages grth flat at 0.8%q/3.4%y (in line with RBA & mkt). The details were on the soft side tho with public sector wages grth elevated at 3.8%yoy but private wages grth slowing to 3.2%yoy & private workers seeing a lower avg rise than a yr ago (3.6% v 3.9% yr ago)..

Cotality home price data Nov month to date

Syd +0.5% (=0.8% at mthly rate)

Mel +0.2%

Bri +0.9%

Ade +0.8%

Per +1.2%

5 city av +0.6% (=1.1% at mthly rate)

Property price growth remains strong so far this mth despite talk rates may have bottomed with 5% deposit scheme likely helping

Syd +0.5% (=0.8% at mthly rate)

Mel +0.2%

Bri +0.9%

Ade +0.8%

Per +1.2%

5 city av +0.6% (=1.1% at mthly rate)

Property price growth remains strong so far this mth despite talk rates may have bottomed with 5% deposit scheme likely helping

November 17, 2025 at 1:31 AM

Cotality home price data Nov month to date

Syd +0.5% (=0.8% at mthly rate)

Mel +0.2%

Bri +0.9%

Ade +0.8%

Per +1.2%

5 city av +0.6% (=1.1% at mthly rate)

Property price growth remains strong so far this mth despite talk rates may have bottomed with 5% deposit scheme likely helping

Syd +0.5% (=0.8% at mthly rate)

Mel +0.2%

Bri +0.9%

Ade +0.8%

Per +1.2%

5 city av +0.6% (=1.1% at mthly rate)

Property price growth remains strong so far this mth despite talk rates may have bottomed with 5% deposit scheme likely helping

Prelim Domain auction clearances

Syd 67%=final ~66%,Nov avg 60

Mel 66%=final ~63%,Nov avg 61

Clearances r continuing to slow reflecting talk of less rate cuts & rising listings but looks partly seasonal. Support remains from 3 rate cuts this yr & the low deposit scheme.

#ausecon

Syd 67%=final ~66%,Nov avg 60

Mel 66%=final ~63%,Nov avg 61

Clearances r continuing to slow reflecting talk of less rate cuts & rising listings but looks partly seasonal. Support remains from 3 rate cuts this yr & the low deposit scheme.

#ausecon

November 15, 2025 at 7:31 AM

Prelim Domain auction clearances

Syd 67%=final ~66%,Nov avg 60

Mel 66%=final ~63%,Nov avg 61

Clearances r continuing to slow reflecting talk of less rate cuts & rising listings but looks partly seasonal. Support remains from 3 rate cuts this yr & the low deposit scheme.

#ausecon

Syd 67%=final ~66%,Nov avg 60

Mel 66%=final ~63%,Nov avg 61

Clearances r continuing to slow reflecting talk of less rate cuts & rising listings but looks partly seasonal. Support remains from 3 rate cuts this yr & the low deposit scheme.

#ausecon

Eurozone shares -0.9% (+2.2%)

US shares -0.05%(+0.1% wk) up from -1.3% with 50 day av holding so far.Nas +0.1%

US 10 yr yld +3bp to 4.15%

Oil +2.1% to $59.9

Gold -2.1% to $4084

Iron ore -0.2% to $103.5

Bitcoin $94.7k as risk off tone weighs

ASX futures -0.2%

$A 0.6537 w $US +0.1%

US shares -0.05%(+0.1% wk) up from -1.3% with 50 day av holding so far.Nas +0.1%

US 10 yr yld +3bp to 4.15%

Oil +2.1% to $59.9

Gold -2.1% to $4084

Iron ore -0.2% to $103.5

Bitcoin $94.7k as risk off tone weighs

ASX futures -0.2%

$A 0.6537 w $US +0.1%

November 14, 2025 at 9:52 PM

Eurozone shares -0.9% (+2.2%)

US shares -0.05%(+0.1% wk) up from -1.3% with 50 day av holding so far.Nas +0.1%

US 10 yr yld +3bp to 4.15%

Oil +2.1% to $59.9

Gold -2.1% to $4084

Iron ore -0.2% to $103.5

Bitcoin $94.7k as risk off tone weighs

ASX futures -0.2%

$A 0.6537 w $US +0.1%

US shares -0.05%(+0.1% wk) up from -1.3% with 50 day av holding so far.Nas +0.1%

US 10 yr yld +3bp to 4.15%

Oil +2.1% to $59.9

Gold -2.1% to $4084

Iron ore -0.2% to $103.5

Bitcoin $94.7k as risk off tone weighs

ASX futures -0.2%

$A 0.6537 w $US +0.1%

China Oct activity data slowed further to 4.9%yoy for IP, 2.9% for retail sales with investment -1.7% as property inv fell 14.7%. Home prices & prop sales continue to fall.

GDP grth this yr is probably still on track for just below 5% but incremental policy stimulus is still likely

(Bloomberg table)

GDP grth this yr is probably still on track for just below 5% but incremental policy stimulus is still likely

(Bloomberg table)

November 14, 2025 at 2:49 AM

China Oct activity data slowed further to 4.9%yoy for IP, 2.9% for retail sales with investment -1.7% as property inv fell 14.7%. Home prices & prop sales continue to fall.

GDP grth this yr is probably still on track for just below 5% but incremental policy stimulus is still likely

(Bloomberg table)

GDP grth this yr is probably still on track for just below 5% but incremental policy stimulus is still likely

(Bloomberg table)