Jim Paulsen

@jimwpaulsen.bsky.social

PhD economist by training. 40 years as a Chief Investment Strategist still following the economy & financial markets at http://paulsenperspectives.Substack.com

Job numbers are punk, and the unemployment rate is up to 4.4%. Trends in public company employment are even worse. Policy officials need to make job creation "the" priority! Check out my work at paulsenperspectives.substack.com

November 20, 2025 at 6:43 PM

Job numbers are punk, and the unemployment rate is up to 4.4%. Trends in public company employment are even worse. Policy officials need to make job creation "the" priority! Check out my work at paulsenperspectives.substack.com

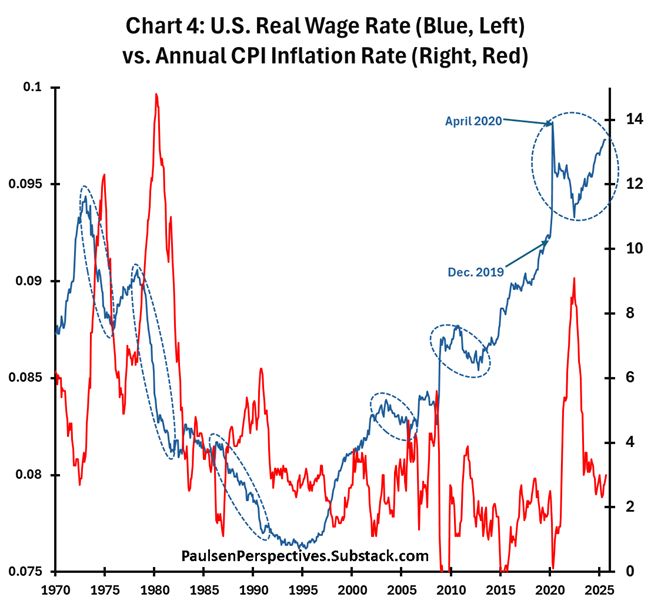

US Inflation has been calm for the past 3 years. Real GDP growth & jobs have been subpar for 20 years and both are currently punk. Why do policy officials continue to emphasize fighting inflation rather than promoting/supporting real growth? See my latest report @ paulsenperspectives.substack.com

November 20, 2025 at 1:11 PM

US Inflation has been calm for the past 3 years. Real GDP growth & jobs have been subpar for 20 years and both are currently punk. Why do policy officials continue to emphasize fighting inflation rather than promoting/supporting real growth? See my latest report @ paulsenperspectives.substack.com

The Main Street Meter has a strong inverse relationship with future stock market returns. It has declined substantially suggesting the stock market is "younger" and more attractive than 22% of time since 1955! See my latest report for all the details at: paulsenperspectives.substack.com

November 17, 2025 at 12:36 PM

The Main Street Meter has a strong inverse relationship with future stock market returns. It has declined substantially suggesting the stock market is "younger" and more attractive than 22% of time since 1955! See my latest report for all the details at: paulsenperspectives.substack.com

I had the pleasure of joining Morgan Brennan & Jon Fortt on CNBC Overtime Friday. We had a lively discussion about the stock market, broader market plays, and the tech bubble. Thanks to both Morgan & Jon for having me. Have a listen!

PaulsenPerspectives.Substack.com

www.youtube.com/watch?v=av4_...

PaulsenPerspectives.Substack.com

www.youtube.com/watch?v=av4_...

LinkedIn

This link will take you to a page that’s not on LinkedIn

lnkd.in

November 10, 2025 at 12:44 PM

I had the pleasure of joining Morgan Brennan & Jon Fortt on CNBC Overtime Friday. We had a lively discussion about the stock market, broader market plays, and the tech bubble. Thanks to both Morgan & Jon for having me. Have a listen!

PaulsenPerspectives.Substack.com

www.youtube.com/watch?v=av4_...

PaulsenPerspectives.Substack.com

www.youtube.com/watch?v=av4_...

The Stock Market is entering its historically strongest part of the year (November through April) after performance during its weakest part (May thru Oct) was STRONG. Both seasonal results point to additional solid stock market returns. See my full report for free @ paulsenperspectives.substack.com

October 30, 2025 at 11:59 AM

The Stock Market is entering its historically strongest part of the year (November through April) after performance during its weakest part (May thru Oct) was STRONG. Both seasonal results point to additional solid stock market returns. See my full report for free @ paulsenperspectives.substack.com

Participation in this bull market has been extremely narrow. However, for the 1st time in about 2 years, RTY's EPS is outpacing S&P EPS. Maybe more accommodative economic policies are starting to awaken broader parts of the stock market? paulsenperspectives.subtack.com

October 28, 2025 at 7:28 PM

Participation in this bull market has been extremely narrow. However, for the 1st time in about 2 years, RTY's EPS is outpacing S&P EPS. Maybe more accommodative economic policies are starting to awaken broader parts of the stock market? paulsenperspectives.subtack.com

Despite the 2020-2022 inflationary surge being one of the largest in post-war history, among the economy’s major performance benchmarks - real GDP, employment, real profits, & real wages -- there was little damaging impact. Why? See my latest report at paulsenperspectives.substack.com

October 27, 2025 at 11:35 AM

Despite the 2020-2022 inflationary surge being one of the largest in post-war history, among the economy’s major performance benchmarks - real GDP, employment, real profits, & real wages -- there was little damaging impact. Why? See my latest report at paulsenperspectives.substack.com

What has happened to US economic momentum since the government quit releasing econ reports on Oct. 1st? A good proxy for US economic surprises may be the relative performance of S&P cyclical sectors. Cyclicals have continued underperforming badly since Oct 1!

See paulsenperspectives.substack.com

See paulsenperspectives.substack.com

October 24, 2025 at 5:34 PM

What has happened to US economic momentum since the government quit releasing econ reports on Oct. 1st? A good proxy for US economic surprises may be the relative performance of S&P cyclical sectors. Cyclicals have continued underperforming badly since Oct 1!

See paulsenperspectives.substack.com

See paulsenperspectives.substack.com

New-era has carried investors during the first three years of this bull market. Could old-era segments assisted by economic policy easing finally take leadership and elongate this bull for a few more years? See my latest report @ paulsenperspectives.substack.com

October 6, 2025 at 11:56 AM

New-era has carried investors during the first three years of this bull market. Could old-era segments assisted by economic policy easing finally take leadership and elongate this bull for a few more years? See my latest report @ paulsenperspectives.substack.com

Because the jobs market has been so weak, it's become the most important economic metric. Less than 1% job growth in the last year and a rise in the UR make job market conditions simply unacceptable. See my latest free report "Jobs Rule" @ paulsenperspectives.substack.com

October 2, 2025 at 12:04 PM

Because the jobs market has been so weak, it's become the most important economic metric. Less than 1% job growth in the last year and a rise in the UR make job market conditions simply unacceptable. See my latest free report "Jobs Rule" @ paulsenperspectives.substack.com

I recently had the great opportunity to work with Jack Forehand and Justin Carbonneau from the Excess Return Podcast for our monthly discuss. I hope you have some time to Please watch the discussion. Thanks! www.google.com/url?sa=t&rct...

See my reserach @ paulsenperspectives.substack.com

See my reserach @ paulsenperspectives.substack.com

You're Misreading This Bull Market | Jim Paulsen on the Major Supports That Are About to Flip

Follow Jim at https://paulsenperspectives.substack.com/ In this episode, we sit down with Jim Paulsen to analyze the latest economic and market data through his lens of decades of market experience. Jim shares insights from his Paulsen Perspectives research, covering the job market, the Fed, inflation, valuations, investor confidence, and what they all mean for the future of the economy and markets. We explore why confidence is so low despite a bull market, how Fed policy is shaping market dynamics, and where investors might want to focus as the cycle evolves. Topics covered in the episode: * The job market’s pivotal role in driving the economy and Fed decisions * Why recent Fed rate cuts may mark a turning point in market support systems * The narrowness of the bull market and how innovation-driven firms diverge from traditional cycles * Investor confidence, the “misery index,” and recession probability models * How easing may broaden market participation beyond large-cap growth * What “animal spirits” mean for small caps, high beta, and IPOs * The disconnect between inflation, bond yields, and growth measures * Gold, cash, crypto, and tech as “fear assets” in today’s environment * The impact of tariffs on profits, wages, and inflation expectations * Valuations in context: historical perspective and the upward bias of multiples Timestamps: 00:00 Introduction and market overview 02:00 Fed easing, inflation, and recession risks 09:00 Bull market without normal supports 17:00 Narrow leadership and innovative companies 23:55 Confidence and the misery index 29:35 Yield curve, recession probabilities, and Fed policy 34:00 Broadening of market participation 37:00 Animal spirit stocks and small caps 38:00 Inflation, bond yields, and resource unemployment 43:20 Copper-gold ratio and yields 45:10 The role of gold in portfolios 50:00 Cash, crypto, and tech as defensive assets 54:00 Tariffs, inflation, and profit margins 59:00 Inflation persistence vs. wage growth 01:01:10 Valuations and the upward bias in multiples 01:07:00 Closing thoughts and takeaways

www.google.com

October 1, 2025 at 7:16 PM

I recently had the great opportunity to work with Jack Forehand and Justin Carbonneau from the Excess Return Podcast for our monthly discuss. I hope you have some time to Please watch the discussion. Thanks! www.google.com/url?sa=t&rct...

See my reserach @ paulsenperspectives.substack.com

See my reserach @ paulsenperspectives.substack.com

I suspect the disinflationary force from weakness in real economic activities will more than offset any additional inflationary force from tariffs. The chart below shows the average growth of 7 key metrics relative to CPI inflation. See my full report @ paulsenperspectives.substack.com

September 25, 2025 at 12:24 PM

I suspect the disinflationary force from weakness in real economic activities will more than offset any additional inflationary force from tariffs. The chart below shows the average growth of 7 key metrics relative to CPI inflation. See my full report @ paulsenperspectives.substack.com

US Confidence has been depressed since 2022 primarily because of chronic recession fears tied to an inverted YC. The Fed is finally easing and recession probabilities declining. Thus, confidence & stocks should rise in the coming year. See my latest report @ paulsenperspectives.substack.com

September 22, 2025 at 12:03 PM

US Confidence has been depressed since 2022 primarily because of chronic recession fears tied to an inverted YC. The Fed is finally easing and recession probabilities declining. Thus, confidence & stocks should rise in the coming year. See my latest report @ paulsenperspectives.substack.com

Since the Fed has finally opened the basement door, my latest piece asks, "how low can bond yields go"? The CPI inflation rate, resource unemployment, and Dr. Copper as well as several other strong historical relationships all say bond yields remain too high. paulsenperspectives.substack.com

September 18, 2025 at 12:37 PM

Since the Fed has finally opened the basement door, my latest piece asks, "how low can bond yields go"? The CPI inflation rate, resource unemployment, and Dr. Copper as well as several other strong historical relationships all say bond yields remain too high. paulsenperspectives.substack.com

A Fed ease will be BIG for the stock market. This is the only Bull market in post-war history which has lived its entire existence with negative excess financial liquidity growth and with an inverted yield curve. This is about to change and #stocks will love it! paulsenperspectives.substack.com

September 12, 2025 at 3:58 PM

A Fed ease will be BIG for the stock market. This is the only Bull market in post-war history which has lived its entire existence with negative excess financial liquidity growth and with an inverted yield curve. This is about to change and #stocks will love it! paulsenperspectives.substack.com

Economic Capacity is oddly expanding as the recovery matures. Labor & factory capacity are growing, policy capacity (e.g., YC is still inverted, excess money growth is still low), private balance sheet capacity & liquidity remain immense. See my latest report at: paulsenperspectives.substack.com

September 11, 2025 at 12:53 PM

Economic Capacity is oddly expanding as the recovery matures. Labor & factory capacity are growing, policy capacity (e.g., YC is still inverted, excess money growth is still low), private balance sheet capacity & liquidity remain immense. See my latest report at: paulsenperspectives.substack.com

See my latest report "It's Time to Discard the 2% Inflation Obsession". As the charts below demonstrate, there is nothing magical about 2% inflation for real GDP, jobs, or real profits & income growth. For further insights, click the link below. paulsenperspectives.substack.com

September 8, 2025 at 11:41 AM

See my latest report "It's Time to Discard the 2% Inflation Obsession". As the charts below demonstrate, there is nothing magical about 2% inflation for real GDP, jobs, or real profits & income growth. For further insights, click the link below. paulsenperspectives.substack.com

The fearful fuel underlying the gold rally is finally starting to fade and the price of gold is increasingly at risk. See the relative price chart below. Could its relative price return to its range since 1980? Click the link for my latest report "Golden Risk" at paulsenperspectives.substack.com

September 4, 2025 at 12:36 PM

The fearful fuel underlying the gold rally is finally starting to fade and the price of gold is increasingly at risk. See the relative price chart below. Could its relative price return to its range since 1980? Click the link for my latest report "Golden Risk" at paulsenperspectives.substack.com

Is there really any mystery why homebuyer affordability has risen and stayed so high? The chart below offers one compelling reason. Affordability may also why consumer confidence is so low. A Fed easing could improve much on both Main and Wall. See my work at PaulsenPerspectives.Substack.com

September 3, 2025 at 7:11 PM

Is there really any mystery why homebuyer affordability has risen and stayed so high? The chart below offers one compelling reason. Affordability may also why consumer confidence is so low. A Fed easing could improve much on both Main and Wall. See my work at PaulsenPerspectives.Substack.com

Since 1970, intl. stocks have only had 3 secular leadership cycles and each of these coincided with a secular decline in the US dollar. Has a 4th secular decline in the dollar begun making the case for a secular overweight in intl. stocks? See my latest at paulsenperspectives.substack.com

September 2, 2025 at 12:15 PM

Since 1970, intl. stocks have only had 3 secular leadership cycles and each of these coincided with a secular decline in the US dollar. Has a 4th secular decline in the dollar begun making the case for a secular overweight in intl. stocks? See my latest at paulsenperspectives.substack.com

Health care stocks have been a dismal investment during this bull market. But relative to real drug prices, the S&P 500 health care sector finally trades in its cheapest quartile for the first time in 15 years. See my latest report for all the details at paulsenperspectives.substack.com

August 28, 2025 at 12:09 PM

Health care stocks have been a dismal investment during this bull market. But relative to real drug prices, the S&P 500 health care sector finally trades in its cheapest quartile for the first time in 15 years. See my latest report for all the details at paulsenperspectives.substack.com

If the Fed begins easing will recession fears again rise? Perhaps the better question is 'can' the economy recess? Many characteristics are evident today which rarely are seen at the start of past recessions like the two examples below. See my latest report @ paulsenperspectives.substack.com

August 25, 2025 at 11:35 AM

If the Fed begins easing will recession fears again rise? Perhaps the better question is 'can' the economy recess? Many characteristics are evident today which rarely are seen at the start of past recessions like the two examples below. See my latest report @ paulsenperspectives.substack.com

Excess economic liquidity divided by the cash hoarding/dumping indicator has demonstrated a close relationship with inflation and yields since 1960. If inflation risk is overblown, stocks & bonds may have another leg left. For the details, See my latest report @

paulsenperspectives.substack.com

paulsenperspectives.substack.com

August 21, 2025 at 12:05 PM

Excess economic liquidity divided by the cash hoarding/dumping indicator has demonstrated a close relationship with inflation and yields since 1960. If inflation risk is overblown, stocks & bonds may have another leg left. For the details, See my latest report @

paulsenperspectives.substack.com

paulsenperspectives.substack.com

The S&P 500 trades at a premium to its post-war trendline of 43%, higher than 93% of the time. However, much of the broader US stock market continues to sell below respective trendlines. See my latest report for the implications of the narrowest bull since WWII.

paulsen.perspectives.substack.com

paulsen.perspectives.substack.com

August 18, 2025 at 11:50 AM

The S&P 500 trades at a premium to its post-war trendline of 43%, higher than 93% of the time. However, much of the broader US stock market continues to sell below respective trendlines. See my latest report for the implications of the narrowest bull since WWII.

paulsen.perspectives.substack.com

paulsen.perspectives.substack.com

US economic surprise indices measure real growth & inflation momentum. As the chart below shows, today's environment looks much more like "weak growth" than it does "stagflation". See my latest report "A Pictorial Look at Inflation" at paulsenperspectives.substack.com

August 14, 2025 at 1:22 PM

US economic surprise indices measure real growth & inflation momentum. As the chart below shows, today's environment looks much more like "weak growth" than it does "stagflation". See my latest report "A Pictorial Look at Inflation" at paulsenperspectives.substack.com