@emopportunities.bsky.social

EM credit & rates PM. Opportunistic management style with large expertise on restructuring stories. (no investment advice or recommendations, my own view)

🇸🇳 Senegal : *IMF, WORLD BANK WORKING ON FINALIZING SENEGAL'S DEBT ANALYSIS

I reload a bit on Wednesday tbh. Still have decent room to add.

I reload a bit on Wednesday tbh. Still have decent room to add.

🇸🇳 Sénégal : after being out of the name for long time. Just started to build a position this morning benefiting from volatility. Not a high conviction trade but some good willingness supporting by an IMF open minded. Sizing matters.

November 14, 2025 at 9:22 AM

🇸🇳 Senegal : *IMF, WORLD BANK WORKING ON FINALIZING SENEGAL'S DEBT ANALYSIS

I reload a bit on Wednesday tbh. Still have decent room to add.

I reload a bit on Wednesday tbh. Still have decent room to add.

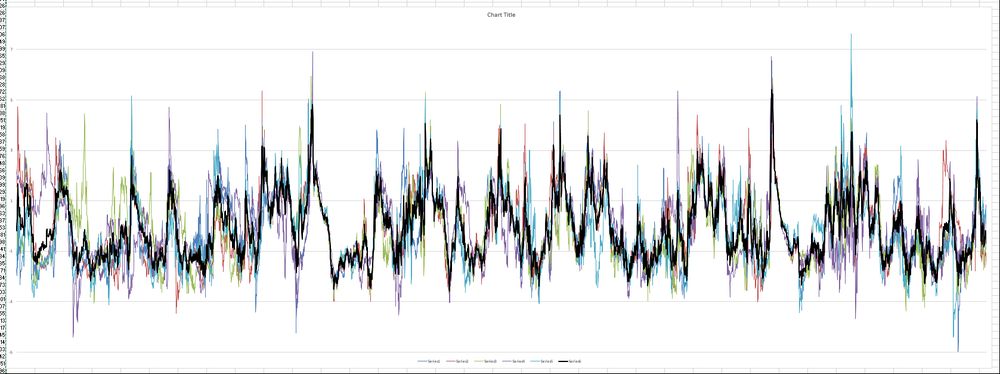

Global EM :

Two proprietary EM indicators (>>0 track):

• 1st = global macro risk support

• 2nd = EM-specific risk sentiment

Interesting divergence: EM risk appetite still well above danger zone, while global macro support for EM just dropped sharply.

Python if people asked

Two proprietary EM indicators (>>0 track):

• 1st = global macro risk support

• 2nd = EM-specific risk sentiment

Interesting divergence: EM risk appetite still well above danger zone, while global macro support for EM just dropped sharply.

Python if people asked

November 11, 2025 at 11:25 AM

Global EM :

Two proprietary EM indicators (>>0 track):

• 1st = global macro risk support

• 2nd = EM-specific risk sentiment

Interesting divergence: EM risk appetite still well above danger zone, while global macro support for EM just dropped sharply.

Python if people asked

Two proprietary EM indicators (>>0 track):

• 1st = global macro risk support

• 2nd = EM-specific risk sentiment

Interesting divergence: EM risk appetite still well above danger zone, while global macro support for EM just dropped sharply.

Python if people asked

🇸🇳 Sénégal : after being out of the name for long time. Just started to build a position this morning benefiting from volatility. Not a high conviction trade but some good willingness supporting by an IMF open minded. Sizing matters.

November 7, 2025 at 9:57 AM

🇸🇳 Sénégal : after being out of the name for long time. Just started to build a position this morning benefiting from volatility. Not a high conviction trade but some good willingness supporting by an IMF open minded. Sizing matters.

🇦🇷 Argentina : Here we go. Should be a great day for Argentina holder 😀

October 27, 2025 at 6:20 AM

🇦🇷 Argentina : Here we go. Should be a great day for Argentina holder 😀

IMF takeaways : cautious but a mood of hope with no euphoria. Everyone know about poor valuation but need to sell asset class to survive.

Still don’t like Senegal, though an SLA looks possible. Venezuela still comfortable with.

Still don’t like Senegal, though an SLA looks possible. Venezuela still comfortable with.

October 20, 2025 at 10:41 AM

IMF takeaways : cautious but a mood of hope with no euphoria. Everyone know about poor valuation but need to sell asset class to survive.

Still don’t like Senegal, though an SLA looks possible. Venezuela still comfortable with.

Still don’t like Senegal, though an SLA looks possible. Venezuela still comfortable with.

IMF meetings start today. Let’s see if anything truly insightful comes out of them.

October 14, 2025 at 1:14 PM

IMF meetings start today. Let’s see if anything truly insightful comes out of them.

Tbh, corporate investors crack me up:

• “Corps are more resilient” → nah, just illiquid

• “They lag because of the sovereign cap”

• “They blow up because gov interference”

Sounds like my 6-year-old searching for excuses 😂

• “Corps are more resilient” → nah, just illiquid

• “They lag because of the sovereign cap”

• “They blow up because gov interference”

Sounds like my 6-year-old searching for excuses 😂

September 29, 2025 at 8:30 AM

Tbh, corporate investors crack me up:

• “Corps are more resilient” → nah, just illiquid

• “They lag because of the sovereign cap”

• “They blow up because gov interference”

Sounds like my 6-year-old searching for excuses 😂

• “Corps are more resilient” → nah, just illiquid

• “They lag because of the sovereign cap”

• “They blow up because gov interference”

Sounds like my 6-year-old searching for excuses 😂

🇦🇷 Argentina : Buenos holders looking Argentina bonds

a man in a suit and tie is asking " what 's going on here "

ALT: a man in a suit and tie is asking " what 's going on here "

media.tenor.com

September 24, 2025 at 12:33 PM

🇦🇷 Argentina : Buenos holders looking Argentina bonds

🇦🇷 Argentina : Some good news coming from US. Bonds are up 7pts.

September 22, 2025 at 1:31 PM

🇦🇷 Argentina : Some good news coming from US. Bonds are up 7pts.

🇦🇷 Argentina: Added a second tranche at 48.4 on this latest leg lower, still capacity to increase.

Interesting how the market eagerly chased every 0.5pt dip around 70, yet is now just as eager to unload at any price.

Interesting how the market eagerly chased every 0.5pt dip around 70, yet is now just as eager to unload at any price.

🇦🇷 Argentina: sharp wake-up for bondholders. I cut most of my exposure Friday on positioning & risk/reward (still have a bit of Buenos). Bonds opened -6pts, so I picked up Arg 35s at 56.2 (still have lot of room to add). Good luck to everyone

September 18, 2025 at 3:22 PM

🇦🇷 Argentina: Added a second tranche at 48.4 on this latest leg lower, still capacity to increase.

Interesting how the market eagerly chased every 0.5pt dip around 70, yet is now just as eager to unload at any price.

Interesting how the market eagerly chased every 0.5pt dip around 70, yet is now just as eager to unload at any price.

All my PM colleagues (€IG as €HY) panic over France slipping from AA- to A+, while I’m chilling on a comfy B- cushion. Different leagues of stress.

a man in a suit and tie is sitting in a chair with his hands in the air

ALT: a man in a suit and tie is sitting in a chair with his hands in the air

media.tenor.com

September 16, 2025 at 10:41 AM

All my PM colleagues (€IG as €HY) panic over France slipping from AA- to A+, while I’m chilling on a comfy B- cushion. Different leagues of stress.

Global EM: Total return ~10% over the past 6 months. Historically, further upside over the last 25 yrs only came after a global shock.

Risk/reward now feels asymmetric, time to reduce risk or to be selective.

TTR by region (25 yrs):

Risk/reward now feels asymmetric, time to reduce risk or to be selective.

TTR by region (25 yrs):

September 15, 2025 at 10:06 AM

Global EM: Total return ~10% over the past 6 months. Historically, further upside over the last 25 yrs only came after a global shock.

Risk/reward now feels asymmetric, time to reduce risk or to be selective.

TTR by region (25 yrs):

Risk/reward now feels asymmetric, time to reduce risk or to be selective.

TTR by region (25 yrs):

🇹🇳 Tunisia – Big day for this credit. Been long since the early lows, riding the whole curve: 23s, 24s, 26s and finally the 31s starting around 55 cts.

🥳

🥳

September 12, 2025 at 2:24 PM

🇹🇳 Tunisia – Big day for this credit. Been long since the early lows, riding the whole curve: 23s, 24s, 26s and finally the 31s starting around 55 cts.

🥳

🥳

🇨🇴 Colombia: +17% since then.

Today’s €4.1bn 3-part deal reportedly drew ~€22bn demand. Liability mgmt well timed, but with spreads now ~325bp, valuation no longer looks cheap.

Today’s €4.1bn 3-part deal reportedly drew ~€22bn demand. Liability mgmt well timed, but with spreads now ~325bp, valuation no longer looks cheap.

🇨🇴 Colombia : Yes deficit, yes politics but :

- It’s already priced in as we are trading as a B+/BB- so who cares?

- 8.7% yield on the LE (decent buffer) + one of the last wide spread

- Market positioning is ok (even if a bit OW)

- No big wall of maturity coming (€/$)

- It’s already priced in as we are trading as a B+/BB- so who cares?

- 8.7% yield on the LE (decent buffer) + one of the last wide spread

- Market positioning is ok (even if a bit OW)

- No big wall of maturity coming (€/$)

September 10, 2025 at 2:59 PM

🇨🇴 Colombia: +17% since then.

Today’s €4.1bn 3-part deal reportedly drew ~€22bn demand. Liability mgmt well timed, but with spreads now ~325bp, valuation no longer looks cheap.

Today’s €4.1bn 3-part deal reportedly drew ~€22bn demand. Liability mgmt well timed, but with spreads now ~325bp, valuation no longer looks cheap.

🇦🇷 Argentina: sharp wake-up for bondholders. I cut most of my exposure Friday on positioning & risk/reward (still have a bit of Buenos). Bonds opened -6pts, so I picked up Arg 35s at 56.2 (still have lot of room to add). Good luck to everyone

September 8, 2025 at 10:53 AM

🇦🇷 Argentina: sharp wake-up for bondholders. I cut most of my exposure Friday on positioning & risk/reward (still have a bit of Buenos). Bonds opened -6pts, so I picked up Arg 35s at 56.2 (still have lot of room to add). Good luck to everyone

🇻🇪 Venezuela: A bit of newsflow as pressure is rising on Venezuela and Maduro.

August 20, 2025 at 7:55 PM

🇻🇪 Venezuela: A bit of newsflow as pressure is rising on Venezuela and Maduro.

EM Global : EM sov spreads outperforms corpo ones <> DM

2004–07: Sovereigns outperformed on the commodity boom

2010–22: Deficits hurt sovereigns

Since 2022: Fiscal repair + CB credibility = sov tightening cycle

EM sovereigns spreads should continue to outperform corporates.

2004–07: Sovereigns outperformed on the commodity boom

2010–22: Deficits hurt sovereigns

Since 2022: Fiscal repair + CB credibility = sov tightening cycle

EM sovereigns spreads should continue to outperform corporates.

August 20, 2025 at 9:51 AM

EM Global : EM sov spreads outperforms corpo ones <> DM

2004–07: Sovereigns outperformed on the commodity boom

2010–22: Deficits hurt sovereigns

Since 2022: Fiscal repair + CB credibility = sov tightening cycle

EM sovereigns spreads should continue to outperform corporates.

2004–07: Sovereigns outperformed on the commodity boom

2010–22: Deficits hurt sovereigns

Since 2022: Fiscal repair + CB credibility = sov tightening cycle

EM sovereigns spreads should continue to outperform corporates.

🇪🇨 Ecuador : As you know Ecuador has been part of my biggest convictions over the last 2-3years. But today it’s time to say goodbye. My trigger is more about oil price and overall market valuation than the gvt itself.

August 19, 2025 at 2:03 PM

🇪🇨 Ecuador : As you know Ecuador has been part of my biggest convictions over the last 2-3years. But today it’s time to say goodbye. My trigger is more about oil price and overall market valuation than the gvt itself.

🇿🇲 Zambia : (Bloomberg) -- Zambia’s debt-carrying capacity under the Composite Indicator rating remains weak, the International Monetary Fund says in staff report.

53s down 4pts 😬

53s down 4pts 😬

August 6, 2025 at 10:25 AM

🇿🇲 Zambia : (Bloomberg) -- Zambia’s debt-carrying capacity under the Composite Indicator rating remains weak, the International Monetary Fund says in staff report.

53s down 4pts 😬

53s down 4pts 😬

Global EM : Any opportunity ? No ? Ok back to bed.

Still holding:

- high cash level bucket or 1yr paper ~20%+

- decent CDS expo ~ 70%

- decent steepner in $

- credit barbell between IG and B/lower credits

- fx frontier vs € or $

Let’s hope August could offer some volatility.

Still holding:

- high cash level bucket or 1yr paper ~20%+

- decent CDS expo ~ 70%

- decent steepner in $

- credit barbell between IG and B/lower credits

- fx frontier vs € or $

Let’s hope August could offer some volatility.

a cartoon of donald duck is laying in bed with his eyes closed

ALT: a cartoon of donald duck is laying in bed with his eyes closed

media.tenor.com

August 1, 2025 at 1:59 PM

Global EM : Any opportunity ? No ? Ok back to bed.

Still holding:

- high cash level bucket or 1yr paper ~20%+

- decent CDS expo ~ 70%

- decent steepner in $

- credit barbell between IG and B/lower credits

- fx frontier vs € or $

Let’s hope August could offer some volatility.

Still holding:

- high cash level bucket or 1yr paper ~20%+

- decent CDS expo ~ 70%

- decent steepner in $

- credit barbell between IG and B/lower credits

- fx frontier vs € or $

Let’s hope August could offer some volatility.

Global EM:

- chief we can’t issue anymore

- ok don’t worry do green bonds, it will fly under the radar for most investors

- chief no one care about green bonds anymore

- I have a crazy idea, let’s rebase our GDP

- chief we can’t issue anymore

- ok don’t worry do green bonds, it will fly under the radar for most investors

- chief no one care about green bonds anymore

- I have a crazy idea, let’s rebase our GDP

July 22, 2025 at 10:42 AM

Global EM:

- chief we can’t issue anymore

- ok don’t worry do green bonds, it will fly under the radar for most investors

- chief no one care about green bonds anymore

- I have a crazy idea, let’s rebase our GDP

- chief we can’t issue anymore

- ok don’t worry do green bonds, it will fly under the radar for most investors

- chief no one care about green bonds anymore

- I have a crazy idea, let’s rebase our GDP

Let me clarify: last chart is just 6m rolling em regional normalization on price. Below same chart on spreads.

So what I’m saying is just I’m more cautious about spread duration risk locally.

So what I’m saying is just I’m more cautious about spread duration risk locally.

July 2, 2025 at 9:57 AM

Let me clarify: last chart is just 6m rolling em regional normalization on price. Below same chart on spreads.

So what I’m saying is just I’m more cautious about spread duration risk locally.

So what I’m saying is just I’m more cautious about spread duration risk locally.

Global EM: I reduced Angola and Egypt exposure yst and today. Closed Zambia 53s.

Imo we saw a rebound as mkt was running after papers due to light positioning. Except if we have strong inflows, dynamic should drop.

We are trading at 2-3 z score so prefer to reduce risk.

Imo we saw a rebound as mkt was running after papers due to light positioning. Except if we have strong inflows, dynamic should drop.

We are trading at 2-3 z score so prefer to reduce risk.

July 2, 2025 at 9:14 AM

Global EM: I reduced Angola and Egypt exposure yst and today. Closed Zambia 53s.

Imo we saw a rebound as mkt was running after papers due to light positioning. Except if we have strong inflows, dynamic should drop.

We are trading at 2-3 z score so prefer to reduce risk.

Imo we saw a rebound as mkt was running after papers due to light positioning. Except if we have strong inflows, dynamic should drop.

We are trading at 2-3 z score so prefer to reduce risk.

🇸🇳 Sénégal : Bonds are finally starting to reprice. It could rebound but I still need to see more value on Senegal before to step in especially with a 28s at 79cts…

A comparison with Angola. Both are trading at c.12% (LE) and, we are still waiting for Senegal audits.

A comparison with Angola. Both are trading at c.12% (LE) and, we are still waiting for Senegal audits.

June 30, 2025 at 12:50 PM

🇸🇳 Sénégal : Bonds are finally starting to reprice. It could rebound but I still need to see more value on Senegal before to step in especially with a 28s at 79cts…

A comparison with Angola. Both are trading at c.12% (LE) and, we are still waiting for Senegal audits.

A comparison with Angola. Both are trading at c.12% (LE) and, we are still waiting for Senegal audits.

🇲🇿 Mozambique : Not a bad news to finish the week.

June 27, 2025 at 6:55 AM

🇲🇿 Mozambique : Not a bad news to finish the week.