David Milliken

@davidmilliken.bsky.social

Reuters economics reporter covering the Bank of England, HM Treasury, bond markets and UK data.

And British businesses see their costs rising faster - and are increasing their prices faster than before the pandemic, according to monthly PMI data.

August 4, 2025 at 10:00 AM

And British businesses see their costs rising faster - and are increasing their prices faster than before the pandemic, according to monthly PMI data.

Meanwhile, surveys of what the public and businesses think inflation will be in around 5 years are on the up.

Sometimes these surveys can be a knee-jerk reaction to a recent rise in inflation, but they might also reflect less certainty that inflation will average near the BoE's 2% target.

Sometimes these surveys can be a knee-jerk reaction to a recent rise in inflation, but they might also reflect less certainty that inflation will average near the BoE's 2% target.

August 4, 2025 at 9:59 AM

Meanwhile, surveys of what the public and businesses think inflation will be in around 5 years are on the up.

Sometimes these surveys can be a knee-jerk reaction to a recent rise in inflation, but they might also reflect less certainty that inflation will average near the BoE's 2% target.

Sometimes these surveys can be a knee-jerk reaction to a recent rise in inflation, but they might also reflect less certainty that inflation will average near the BoE's 2% target.

Wage growth is a big driver of services prices and longer-term UK inflation trends.

Lots hangs on whether it continues to slow as the BoE expects - returning to pre-pandemic rates of around 3% - or bottoms out at a higher level.

Lots hangs on whether it continues to slow as the BoE expects - returning to pre-pandemic rates of around 3% - or bottoms out at a higher level.

August 4, 2025 at 9:53 AM

Wage growth is a big driver of services prices and longer-term UK inflation trends.

Lots hangs on whether it continues to slow as the BoE expects - returning to pre-pandemic rates of around 3% - or bottoms out at a higher level.

Lots hangs on whether it continues to slow as the BoE expects - returning to pre-pandemic rates of around 3% - or bottoms out at a higher level.

However, some policymakers worry that longer-term domestic drivers of inflation haven't receded as much as they'd like.

Services inflation at 4.7% is 2 percentage points higher than in 2019.

And food prices, which drive shorter-term inflation moves, are rebounding after a fall in 2025.

Services inflation at 4.7% is 2 percentage points higher than in 2019.

And food prices, which drive shorter-term inflation moves, are rebounding after a fall in 2025.

August 4, 2025 at 9:48 AM

However, some policymakers worry that longer-term domestic drivers of inflation haven't receded as much as they'd like.

Services inflation at 4.7% is 2 percentage points higher than in 2019.

And food prices, which drive shorter-term inflation moves, are rebounding after a fall in 2025.

Services inflation at 4.7% is 2 percentage points higher than in 2019.

And food prices, which drive shorter-term inflation moves, are rebounding after a fall in 2025.

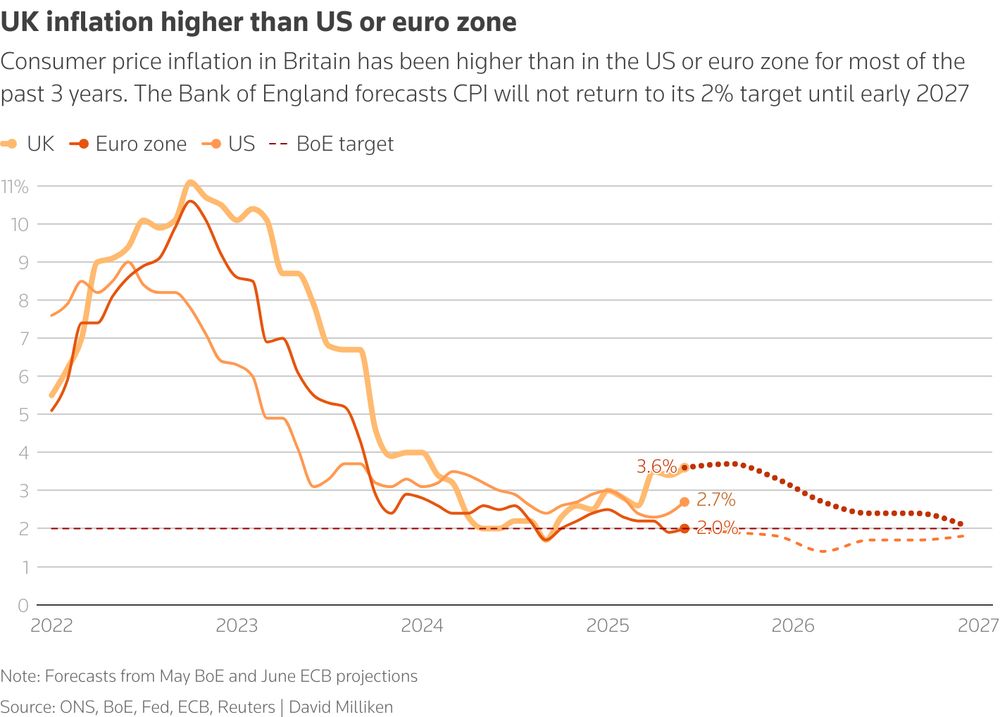

First, a bit of context. British inflation peaked higher than in the United States or the euro zone in 2022 at 11.1%. It fell sharply in 2023 and briefly returned to its 2% target in 2024.

But since hitting a low of 1.7% in September 2024, it has more than doubled, reaching 3.6% in June.

But since hitting a low of 1.7% in September 2024, it has more than doubled, reaching 3.6% in June.

August 4, 2025 at 9:35 AM

First, a bit of context. British inflation peaked higher than in the United States or the euro zone in 2022 at 11.1%. It fell sharply in 2023 and briefly returned to its 2% target in 2024.

But since hitting a low of 1.7% in September 2024, it has more than doubled, reaching 3.6% in June.

But since hitting a low of 1.7% in September 2024, it has more than doubled, reaching 3.6% in June.

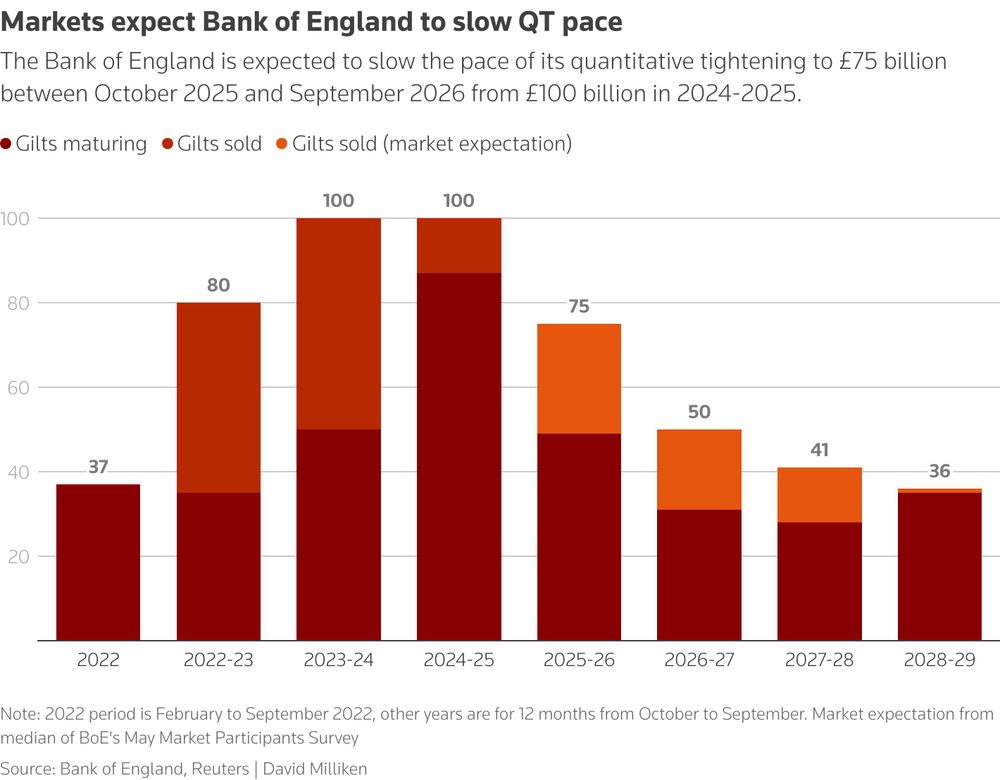

There's more consensus that the BoE will slow QT over the next 12 months to £75 billion from £100 billion.

Note that actually means an *increase* in gilts sold by the BoE, as there's a sharp drop in QT gilts that are due to mature between Oct 2025 and Sept 2026.

Note that actually means an *increase* in gilts sold by the BoE, as there's a sharp drop in QT gilts that are due to mature between Oct 2025 and Sept 2026.

July 28, 2025 at 1:08 PM

There's more consensus that the BoE will slow QT over the next 12 months to £75 billion from £100 billion.

Note that actually means an *increase* in gilts sold by the BoE, as there's a sharp drop in QT gilts that are due to mature between Oct 2025 and Sept 2026.

Note that actually means an *increase* in gilts sold by the BoE, as there's a sharp drop in QT gilts that are due to mature between Oct 2025 and Sept 2026.

Investors have a big range of views on how far the BoE will reduce the QE stockpile it built up between 2009 and 2021.

A BoE survey in May showed a median forecast it would fall to £357 bln by September 2029 from £558 bln. But around half thought it would stay above £400 bln or fall below £290 bln.

A BoE survey in May showed a median forecast it would fall to £357 bln by September 2029 from £558 bln. But around half thought it would stay above £400 bln or fall below £290 bln.

July 28, 2025 at 1:02 PM

Investors have a big range of views on how far the BoE will reduce the QE stockpile it built up between 2009 and 2021.

A BoE survey in May showed a median forecast it would fall to £357 bln by September 2029 from £558 bln. But around half thought it would stay above £400 bln or fall below £290 bln.

A BoE survey in May showed a median forecast it would fall to £357 bln by September 2029 from £558 bln. But around half thought it would stay above £400 bln or fall below £290 bln.

What goes up goes down again. After rising 25 basis points yesterday - their biggest one-day rise since October 2022 - 30-year UK gilt yields have fallen 20 basis points this morning after Trump paused some tariffs last night.

April 10, 2025 at 8:15 AM

What goes up goes down again. After rising 25 basis points yesterday - their biggest one-day rise since October 2022 - 30-year UK gilt yields have fallen 20 basis points this morning after Trump paused some tariffs last night.

30-year UK bond yields reached peaked at 5.649% today, their highest since May 1998.

They're on track to rise 0.19 percentage points today - the sharpest jump since Truss's mini-budget.

It's mostly a reaction to Trump, but also investor jitters about illiquid markets and the UK's high borrowing.

They're on track to rise 0.19 percentage points today - the sharpest jump since Truss's mini-budget.

It's mostly a reaction to Trump, but also investor jitters about illiquid markets and the UK's high borrowing.

April 9, 2025 at 3:22 PM

30-year UK bond yields reached peaked at 5.649% today, their highest since May 1998.

They're on track to rise 0.19 percentage points today - the sharpest jump since Truss's mini-budget.

It's mostly a reaction to Trump, but also investor jitters about illiquid markets and the UK's high borrowing.

They're on track to rise 0.19 percentage points today - the sharpest jump since Truss's mini-budget.

It's mostly a reaction to Trump, but also investor jitters about illiquid markets and the UK's high borrowing.

Not something you see evert day: 30-year UK government bond yields hit their highest since 1998 this morning, after an overnight selloff of US Treasuries

April 9, 2025 at 9:02 AM

Not something you see evert day: 30-year UK government bond yields hit their highest since 1998 this morning, after an overnight selloff of US Treasuries

Gilt yields have risen a bit more off the back of the CPI data. 10-year gilt yields are now at a three-week high of 4.62% and are on track for their biggest daily rise since January 8, up 0.06 percentage points.

Markets still see 2 more rate cuts this year. Some banks e.g. UBS trimming their bets.

Markets still see 2 more rate cuts this year. Some banks e.g. UBS trimming their bets.

February 19, 2025 at 1:33 PM

Gilt yields have risen a bit more off the back of the CPI data. 10-year gilt yields are now at a three-week high of 4.62% and are on track for their biggest daily rise since January 8, up 0.06 percentage points.

Markets still see 2 more rate cuts this year. Some banks e.g. UBS trimming their bets.

Markets still see 2 more rate cuts this year. Some banks e.g. UBS trimming their bets.

Initial market reaction was pretty muted but gilt yields have been edging up. 10-year yields are now at a 3-week high of 4.607%, up nearly 5 bps on the day.

Markets still just about see 2 more quarter-point rate cuts from the Bank of England this year.

Markets still just about see 2 more quarter-point rate cuts from the Bank of England this year.

February 19, 2025 at 9:14 AM

Initial market reaction was pretty muted but gilt yields have been edging up. 10-year yields are now at a 3-week high of 4.607%, up nearly 5 bps on the day.

Markets still just about see 2 more quarter-point rate cuts from the Bank of England this year.

Markets still just about see 2 more quarter-point rate cuts from the Bank of England this year.

Today's UK CPI reading of 3% for January topped all forecasts in Reuters' poll (and the BoE's 2.8% forecast).

But in many ways it was a mirror image of December's weaker-than-expected 2.5% reading.

Air fares were a driving factor both times, adding 0.25pp in Dec and subtracting 0.14pp in Jan

But in many ways it was a mirror image of December's weaker-than-expected 2.5% reading.

Air fares were a driving factor both times, adding 0.25pp in Dec and subtracting 0.14pp in Jan

February 19, 2025 at 9:03 AM

Today's UK CPI reading of 3% for January topped all forecasts in Reuters' poll (and the BoE's 2.8% forecast).

But in many ways it was a mirror image of December's weaker-than-expected 2.5% reading.

Air fares were a driving factor both times, adding 0.25pp in Dec and subtracting 0.14pp in Jan

But in many ways it was a mirror image of December's weaker-than-expected 2.5% reading.

Air fares were a driving factor both times, adding 0.25pp in Dec and subtracting 0.14pp in Jan

Out overnight: Reuters' exclusive interview with Bank of England Chief Economist Huw Pill.

Top line: he's cautious about further rate cuts (which isn't a no - but means a slowish pace) due to weaknesses in the supply side of the economy and it's ability to match demand.

Other key lines here:

Top line: he's cautious about further rate cuts (which isn't a no - but means a slowish pace) due to weaknesses in the supply side of the economy and it's ability to match demand.

Other key lines here:

February 13, 2025 at 7:58 AM

Out overnight: Reuters' exclusive interview with Bank of England Chief Economist Huw Pill.

Top line: he's cautious about further rate cuts (which isn't a no - but means a slowish pace) due to weaknesses in the supply side of the economy and it's ability to match demand.

Other key lines here:

Top line: he's cautious about further rate cuts (which isn't a no - but means a slowish pace) due to weaknesses in the supply side of the economy and it's ability to match demand.

Other key lines here:

Some fairly dismal public sector productivity data out this morning from the ONS.

Productivity in the health service was up just 0.2% qq in Q3 2024 - despite the end of strikes - and is still nearly 19% below where it was in Q4 2019.

Productivity in the health service was up just 0.2% qq in Q3 2024 - despite the end of strikes - and is still nearly 19% below where it was in Q4 2019.

February 10, 2025 at 12:40 PM

Some fairly dismal public sector productivity data out this morning from the ONS.

Productivity in the health service was up just 0.2% qq in Q3 2024 - despite the end of strikes - and is still nearly 19% below where it was in Q4 2019.

Productivity in the health service was up just 0.2% qq in Q3 2024 - despite the end of strikes - and is still nearly 19% below where it was in Q4 2019.

But whether the DMO wants to move faster is an open question.

"Debt management is an inherently cautious business," notes Moyeen Islam at Barclays.

And the DMO has a lot of debt to manage...

8/n

"Debt management is an inherently cautious business," notes Moyeen Islam at Barclays.

And the DMO has a lot of debt to manage...

8/n

February 7, 2025 at 11:25 AM

But whether the DMO wants to move faster is an open question.

"Debt management is an inherently cautious business," notes Moyeen Islam at Barclays.

And the DMO has a lot of debt to manage...

8/n

"Debt management is an inherently cautious business," notes Moyeen Islam at Barclays.

And the DMO has a lot of debt to manage...

8/n

The UK Debt Management Office - an agency of the Treasury which issues government bonds - isn't blind to this and has been slowly reducing the share of long-dated (>15 years) bonds that it issues.

But some investors say it now needs to go faster.

5/n

But some investors say it now needs to go faster.

5/n

February 7, 2025 at 11:10 AM

The UK Debt Management Office - an agency of the Treasury which issues government bonds - isn't blind to this and has been slowly reducing the share of long-dated (>15 years) bonds that it issues.

But some investors say it now needs to go faster.

5/n

But some investors say it now needs to go faster.

5/n

Re-upping this piece of mine, which takes a look at how Britain finances (and refinances) £300 billion of government debt each year.

The starting point is that Britain is an outlier. The average maturity of a UK government bond trading today is 14 years, versus 7 years for other rich countries.

1/n

The starting point is that Britain is an outlier. The average maturity of a UK government bond trading today is 14 years, versus 7 years for other rich countries.

1/n

February 7, 2025 at 10:55 AM

Re-upping this piece of mine, which takes a look at how Britain finances (and refinances) £300 billion of government debt each year.

The starting point is that Britain is an outlier. The average maturity of a UK government bond trading today is 14 years, versus 7 years for other rich countries.

1/n

The starting point is that Britain is an outlier. The average maturity of a UK government bond trading today is 14 years, versus 7 years for other rich countries.

1/n

Not everyone is so relaxed though. Rob Wood at Pantheon Macroeconomics reckons ONS data showing 5.6% wage growth is about right. It now tallies with the HMRC data, which has fallen to match the ONS reading.

Instead, it was the weak ONS wage readings earlier in 2024 which were wrong!

Instead, it was the weak ONS wage readings earlier in 2024 which were wrong!

January 21, 2025 at 2:27 PM

Not everyone is so relaxed though. Rob Wood at Pantheon Macroeconomics reckons ONS data showing 5.6% wage growth is about right. It now tallies with the HMRC data, which has fallen to match the ONS reading.

Instead, it was the weak ONS wage readings earlier in 2024 which were wrong!

Instead, it was the weak ONS wage readings earlier in 2024 which were wrong!

Andrew Goodwin at Oxford Economics highlights the changing mix of jobs in the workforce (which isn't inherently inflationary) as another factor pushing up wage growth.

An inhouse model of theirs based on sentiment data estimates UK wage is nearer 4.5%.

An inhouse model of theirs based on sentiment data estimates UK wage is nearer 4.5%.

January 21, 2025 at 2:23 PM

Andrew Goodwin at Oxford Economics highlights the changing mix of jobs in the workforce (which isn't inherently inflationary) as another factor pushing up wage growth.

An inhouse model of theirs based on sentiment data estimates UK wage is nearer 4.5%.

An inhouse model of theirs based on sentiment data estimates UK wage is nearer 4.5%.

Driving some of the latest rise in pay growth (3 months to Nov 2024) is a year on year comparison with Sept and Oct 2023, when wages in the financial services sector fell for two months running for the first time since 2020.

Cathal Kennedy at RBC says a bit more here:

Cathal Kennedy at RBC says a bit more here:

January 21, 2025 at 2:17 PM

Driving some of the latest rise in pay growth (3 months to Nov 2024) is a year on year comparison with Sept and Oct 2023, when wages in the financial services sector fell for two months running for the first time since 2020.

Cathal Kennedy at RBC says a bit more here:

Cathal Kennedy at RBC says a bit more here:

So a 16 basis-point drop in gilt yields almost across the board for the UK today, after softer UK and US inflation data.

That leaves 2-year and 5-year gilts just 5 basis points above where they were at the start of the year, while 10s and 30s are about 15 bps higher

That leaves 2-year and 5-year gilts just 5 basis points above where they were at the start of the year, while 10s and 30s are about 15 bps higher

January 15, 2025 at 4:08 PM

So a 16 basis-point drop in gilt yields almost across the board for the UK today, after softer UK and US inflation data.

That leaves 2-year and 5-year gilts just 5 basis points above where they were at the start of the year, while 10s and 30s are about 15 bps higher

That leaves 2-year and 5-year gilts just 5 basis points above where they were at the start of the year, while 10s and 30s are about 15 bps higher

Thirty-year yields are also down, though not as much and are still within 0.1 percentage points of a post-1998 high reached on Monday

January 15, 2025 at 12:11 PM

Thirty-year yields are also down, though not as much and are still within 0.1 percentage points of a post-1998 high reached on Monday

Big drop in UK gilt yields after today's lower than expected UK inflation. Two-year yields are on track for their biggest one-day fall since June 12 2024 (when some US inflation data came in below expectations).

January 15, 2025 at 12:09 PM

Big drop in UK gilt yields after today's lower than expected UK inflation. Two-year yields are on track for their biggest one-day fall since June 12 2024 (when some US inflation data came in below expectations).