Kamil Kovar

@crisisstudent.bsky.social

Economist paid for doing what I love by Moody's Analytics as senior euro zone economist. Student and teacher of macroeconomic and financial crises. Views my own.

Overall, I consider the Q4 final GDP report as good as it could be – both relative to the preliminary data and relative to the expectations at the end of 2024.

Alas, we all know that this is quickly becoming old news with the incoming tariffs and boatload of uncertainty…

9/9

Alas, we all know that this is quickly becoming old news with the incoming tariffs and boatload of uncertainty…

9/9

March 10, 2025 at 7:50 AM

Overall, I consider the Q4 final GDP report as good as it could be – both relative to the preliminary data and relative to the expectations at the end of 2024.

Alas, we all know that this is quickly becoming old news with the incoming tariffs and boatload of uncertainty…

9/9

Alas, we all know that this is quickly becoming old news with the incoming tariffs and boatload of uncertainty…

9/9

The problem is that the decline in net exports in last two quarters was much more about decline in exports than increase in imports.

In other words, there is a good reason to expect further declines in net exports.

8/

In other words, there is a good reason to expect further declines in net exports.

8/

March 10, 2025 at 7:50 AM

The problem is that the decline in net exports in last two quarters was much more about decline in exports than increase in imports.

In other words, there is a good reason to expect further declines in net exports.

8/

In other words, there is a good reason to expect further declines in net exports.

8/

That leaves net exports as the only true negative part of the release.

We know net exports will drag on growth given their bounce in mid-2022 to 2023, which to a large degree was about drop in imports – after all imports were likely to bounce back at least a bit.

7/

We know net exports will drag on growth given their bounce in mid-2022 to 2023, which to a large degree was about drop in imports – after all imports were likely to bounce back at least a bit.

7/

March 10, 2025 at 7:50 AM

That leaves net exports as the only true negative part of the release.

We know net exports will drag on growth given their bounce in mid-2022 to 2023, which to a large degree was about drop in imports – after all imports were likely to bounce back at least a bit.

7/

We know net exports will drag on growth given their bounce in mid-2022 to 2023, which to a large degree was about drop in imports – after all imports were likely to bounce back at least a bit.

7/

So what about those inventories, then?

First, we knew they the Q3 boost will not come again, so weakness was expected.

Second, inventories went further away from normal, so they will likely add in future quarters.

x.com/CrisisStuden...

6/

First, we knew they the Q3 boost will not come again, so weakness was expected.

Second, inventories went further away from normal, so they will likely add in future quarters.

x.com/CrisisStuden...

6/

March 10, 2025 at 7:50 AM

So what about those inventories, then?

First, we knew they the Q3 boost will not come again, so weakness was expected.

Second, inventories went further away from normal, so they will likely add in future quarters.

x.com/CrisisStuden...

6/

First, we knew they the Q3 boost will not come again, so weakness was expected.

Second, inventories went further away from normal, so they will likely add in future quarters.

x.com/CrisisStuden...

6/

Again, looking across countries the same story holds.

We got at least some consumption growth everywhere – and that was on top of strong Q3.

And we got strong growth in fixed investment everywhere but France (alas for investment it is bounce back from previous quarter).

5/

We got at least some consumption growth everywhere – and that was on top of strong Q3.

And we got strong growth in fixed investment everywhere but France (alas for investment it is bounce back from previous quarter).

5/

March 10, 2025 at 7:50 AM

Again, looking across countries the same story holds.

We got at least some consumption growth everywhere – and that was on top of strong Q3.

And we got strong growth in fixed investment everywhere but France (alas for investment it is bounce back from previous quarter).

5/

We got at least some consumption growth everywhere – and that was on top of strong Q3.

And we got strong growth in fixed investment everywhere but France (alas for investment it is bounce back from previous quarter).

5/

And even better, all the components of final domestic demand have expanded, including fixed investment - where we saw expansion for the first time in a long while.

4/

4/

March 10, 2025 at 7:50 AM

And even better, all the components of final domestic demand have expanded, including fixed investment - where we saw expansion for the first time in a long while.

4/

4/

Importantly, this story is geographically broad-based:

All the major economies saw solid increases in final domestic demand, including Germany and France (0.23% and 0.22%).

3/

All the major economies saw solid increases in final domestic demand, including Germany and France (0.23% and 0.22%).

3/

March 10, 2025 at 7:50 AM

Importantly, this story is geographically broad-based:

All the major economies saw solid increases in final domestic demand, including Germany and France (0.23% and 0.22%).

3/

All the major economies saw solid increases in final domestic demand, including Germany and France (0.23% and 0.22%).

3/

Why does this matter?

Well, starting in late September there was a chorus of worries about economic growth in eurozone.

We now know that this was mostly misplaced: in absence of Trump eurozone was on its way to recovery.

2/

Well, starting in late September there was a chorus of worries about economic growth in eurozone.

We now know that this was mostly misplaced: in absence of Trump eurozone was on its way to recovery.

2/

March 10, 2025 at 7:50 AM

Why does this matter?

Well, starting in late September there was a chorus of worries about economic growth in eurozone.

We now know that this was mostly misplaced: in absence of Trump eurozone was on its way to recovery.

2/

Well, starting in late September there was a chorus of worries about economic growth in eurozone.

We now know that this was mostly misplaced: in absence of Trump eurozone was on its way to recovery.

2/

So overall, very bad end to disappointing year. Rather than the expected bottoming out of production we got another leg down – and with Trump in White House, this might be a (noisy) beginning of yet another contraction.

6/

6/

February 13, 2025 at 11:04 AM

So overall, very bad end to disappointing year. Rather than the expected bottoming out of production we got another leg down – and with Trump in White House, this might be a (noisy) beginning of yet another contraction.

6/

6/

So why do I say that the overall number is more ugly than reality?

One reason, really: drop in transport production drove a lot of the decline, and this is unlikely more than monthly noise to be reversed next year.

(That said, similar thing in reverse applies to jump in pharma production).

5/

One reason, really: drop in transport production drove a lot of the decline, and this is unlikely more than monthly noise to be reversed next year.

(That said, similar thing in reverse applies to jump in pharma production).

5/

February 13, 2025 at 11:04 AM

So why do I say that the overall number is more ugly than reality?

One reason, really: drop in transport production drove a lot of the decline, and this is unlikely more than monthly noise to be reversed next year.

(That said, similar thing in reverse applies to jump in pharma production).

5/

One reason, really: drop in transport production drove a lot of the decline, and this is unlikely more than monthly noise to be reversed next year.

(That said, similar thing in reverse applies to jump in pharma production).

5/

Looking at individual industries brought further disappointment. For example, chemicals production seems to be on downward trend again now that gas prices are at 50euro per MWH.

4/

4/

February 13, 2025 at 11:04 AM

Looking at individual industries brought further disappointment. For example, chemicals production seems to be on downward trend again now that gas prices are at 50euro per MWH.

4/

4/

It was also not concentrated in one or two industries, with median industry seeing large decline in December and at 2digit detail most industries saw decline.

3/

3/

February 13, 2025 at 11:04 AM

It was also not concentrated in one or two industries, with median industry seeing large decline in December and at 2digit detail most industries saw decline.

3/

3/

Unlike some previous months, this time around the drop was not about Ireland and Germany.

Indeed, the jump in Ireland mostly offset drop in Germany, so excluding both meant decline of -1.5%

2/

Indeed, the jump in Ireland mostly offset drop in Germany, so excluding both meant decline of -1.5%

2/

February 13, 2025 at 11:04 AM

Unlike some previous months, this time around the drop was not about Ireland and Germany.

Indeed, the jump in Ireland mostly offset drop in Germany, so excluding both meant decline of -1.5%

2/

Indeed, the jump in Ireland mostly offset drop in Germany, so excluding both meant decline of -1.5%

2/

As a result, based on the available data we believe that the final domestic demand had an ok quarter – not as good as Q3, but better than Q1 and Q2.

So in our mind, the recovery is intact – albeit disappointing one.

5/

So in our mind, the recovery is intact – albeit disappointing one.

5/

January 30, 2025 at 4:12 PM

As a result, based on the available data we believe that the final domestic demand had an ok quarter – not as good as Q3, but better than Q1 and Q2.

So in our mind, the recovery is intact – albeit disappointing one.

5/

So in our mind, the recovery is intact – albeit disappointing one.

5/

That said, under the hood the numbers were more positive. While consumption probably saw subdued growth, investment likely added to growth for the first time in more than a year.

Instead, it was net exports which likely dragged on growth – with France and Spain showing as much.

4/

Instead, it was net exports which likely dragged on growth – with France and Spain showing as much.

4/

January 30, 2025 at 4:12 PM

That said, under the hood the numbers were more positive. While consumption probably saw subdued growth, investment likely added to growth for the first time in more than a year.

Instead, it was net exports which likely dragged on growth – with France and Spain showing as much.

4/

Instead, it was net exports which likely dragged on growth – with France and Spain showing as much.

4/

In other words, if it wasn’t for the strong growth in Spain and stellar in Portugal, we would get a contraction in euro zone GDP. This is not a good picture.

3/

3/

January 30, 2025 at 4:12 PM

In other words, if it wasn’t for the strong growth in Spain and stellar in Portugal, we would get a contraction in euro zone GDP. This is not a good picture.

3/

3/

Instead of the headline number, it was the geographical composition of growth which was most negative news in the report:

There was little if any growth to be found outside of Iberian Peninsula. Germany and France saw small contractions, Italy, Austria and Belgium stagnation.

2/

There was little if any growth to be found outside of Iberian Peninsula. Germany and France saw small contractions, Italy, Austria and Belgium stagnation.

2/

January 30, 2025 at 4:12 PM

Instead of the headline number, it was the geographical composition of growth which was most negative news in the report:

There was little if any growth to be found outside of Iberian Peninsula. Germany and France saw small contractions, Italy, Austria and Belgium stagnation.

2/

There was little if any growth to be found outside of Iberian Peninsula. Germany and France saw small contractions, Italy, Austria and Belgium stagnation.

2/

Overall, I think that Q1 will bring some upside inflation surprises relative to the consensus.

Luckily for doves, this won’t change the outcome of January and March meetings.

But I am increasingly more convinced that April will be a skip.

11/

Luckily for doves, this won’t change the outcome of January and March meetings.

But I am increasingly more convinced that April will be a skip.

11/

January 17, 2025 at 12:19 PM

Overall, I think that Q1 will bring some upside inflation surprises relative to the consensus.

Luckily for doves, this won’t change the outcome of January and March meetings.

But I am increasingly more convinced that April will be a skip.

11/

Luckily for doves, this won’t change the outcome of January and March meetings.

But I am increasingly more convinced that April will be a skip.

11/

Here we are in for further unpleasant numbers in Q1.

For example, the decline in German gas prices is for now over, which is not a good sign at all.

10/

For example, the decline in German gas prices is for now over, which is not a good sign at all.

10/

January 17, 2025 at 12:19 PM

Here we are in for further unpleasant numbers in Q1.

For example, the decline in German gas prices is for now over, which is not a good sign at all.

10/

For example, the decline in German gas prices is for now over, which is not a good sign at all.

10/

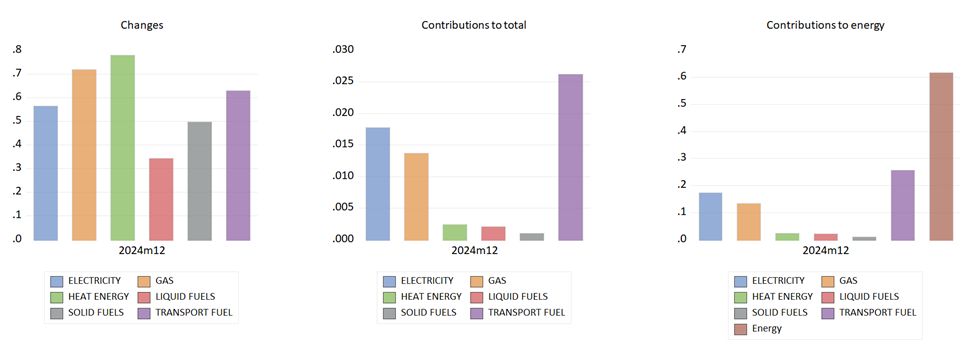

Finally, energy prices confirmed our expectations that the large increase was not only about fuel prices, but reflected higher gas and electricity prices.

9/

9/

January 17, 2025 at 12:19 PM

Finally, energy prices confirmed our expectations that the large increase was not only about fuel prices, but reflected higher gas and electricity prices.

9/

9/

The worst news in food prices is that the pass-through from higher feed prices into higher animal product prices is still not over.

8/

8/

January 17, 2025 at 12:19 PM

The worst news in food prices is that the pass-through from higher feed prices into higher animal product prices is still not over.

8/

8/

Otherwise, the same cross currents are still present.

There hasn’t been any slowdown in coffee and tea prices yet, and while olive oil prices are dropping quickly, butter is doing its best to compensate.

7/

There hasn’t been any slowdown in coffee and tea prices yet, and while olive oil prices are dropping quickly, butter is doing its best to compensate.

7/

January 17, 2025 at 12:19 PM

Otherwise, the same cross currents are still present.

There hasn’t been any slowdown in coffee and tea prices yet, and while olive oil prices are dropping quickly, butter is doing its best to compensate.

7/

There hasn’t been any slowdown in coffee and tea prices yet, and while olive oil prices are dropping quickly, butter is doing its best to compensate.

7/