VK

@vkmacro.bsky.social

I like the weakness in precious metals - since the last few days have been a bit crazy. There’s still more froth left to come out of the market imo.

Was wrong on Fed timing, it’s now rather than Jan, but that’s fine!

Was wrong on Fed timing, it’s now rather than Jan, but that’s fine!

November 14, 2025 at 3:38 PM

I like the weakness in precious metals - since the last few days have been a bit crazy. There’s still more froth left to come out of the market imo.

Was wrong on Fed timing, it’s now rather than Jan, but that’s fine!

Was wrong on Fed timing, it’s now rather than Jan, but that’s fine!

It’s a great lesson - particularly when you see both sides of the book losing simultaneously. Not gonna forget that in a hurry

November 14, 2025 at 12:15 PM

It’s a great lesson - particularly when you see both sides of the book losing simultaneously. Not gonna forget that in a hurry

The one that’s funny is software which is being sold regardless of AI up or AI down

November 14, 2025 at 11:37 AM

The one that’s funny is software which is being sold regardless of AI up or AI down

Insurers too - not sure why but they are also catching a bid

November 14, 2025 at 11:35 AM

Insurers too - not sure why but they are also catching a bid

China’s road fuel consumption***

November 12, 2025 at 7:49 PM

China’s road fuel consumption***

I actually wondered this - thanks

November 12, 2025 at 7:44 PM

I actually wondered this - thanks

Been the same for me having ramen in Japan

November 12, 2025 at 2:39 PM

Been the same for me having ramen in Japan

OpenAI doesn’t yet sell cloud capacity so we can discount them. Meta only has a first party cloud (internal demand) business so far, so again a different example.

Microsoft, Amazon, and Google are all examples of what they will look like from an IaaS perspective since they sell other services.

Microsoft, Amazon, and Google are all examples of what they will look like from an IaaS perspective since they sell other services.

November 12, 2025 at 12:46 PM

OpenAI doesn’t yet sell cloud capacity so we can discount them. Meta only has a first party cloud (internal demand) business so far, so again a different example.

Microsoft, Amazon, and Google are all examples of what they will look like from an IaaS perspective since they sell other services.

Microsoft, Amazon, and Google are all examples of what they will look like from an IaaS perspective since they sell other services.

Azure ROIC followed a similar path despite higher margins and less competition Same story, large upfront costs which payoff over a medium term duration.

Back then, HBS suggested the IaaS cloud biz were commodities with no moats. The moat however is in services and scale!

Back then, HBS suggested the IaaS cloud biz were commodities with no moats. The moat however is in services and scale!

November 12, 2025 at 10:08 AM

Azure ROIC followed a similar path despite higher margins and less competition Same story, large upfront costs which payoff over a medium term duration.

Back then, HBS suggested the IaaS cloud biz were commodities with no moats. The moat however is in services and scale!

Back then, HBS suggested the IaaS cloud biz were commodities with no moats. The moat however is in services and scale!

In 2021, Sundar Pichai said Google cloud are focused on revenue growth and investing aggressively ahead of demand.

In 2022, and start of 2023 cloud revenues decelerated forcing a period of adjustment. It’s very likely something similar happens here. Point imo will be not ot panic like back then.

In 2022, and start of 2023 cloud revenues decelerated forcing a period of adjustment. It’s very likely something similar happens here. Point imo will be not ot panic like back then.

November 12, 2025 at 9:54 AM

In 2021, Sundar Pichai said Google cloud are focused on revenue growth and investing aggressively ahead of demand.

In 2022, and start of 2023 cloud revenues decelerated forcing a period of adjustment. It’s very likely something similar happens here. Point imo will be not ot panic like back then.

In 2022, and start of 2023 cloud revenues decelerated forcing a period of adjustment. It’s very likely something similar happens here. Point imo will be not ot panic like back then.

For now, it’s about tracking rising backlogs and their effective durations. Nadella has said the bulk of their $400bn cloud backlog has a duration of just 2 years! Thats a potential revenue bump of $100bn plus a year from committee contracts which then provides room for upselling other services.

November 12, 2025 at 9:53 AM

For now, it’s about tracking rising backlogs and their effective durations. Nadella has said the bulk of their $400bn cloud backlog has a duration of just 2 years! Thats a potential revenue bump of $100bn plus a year from committee contracts which then provides room for upselling other services.

The point is this hyper focus on the infrastructure layer of Hyperscalers just seems misplaced.

It’s possible depreciation expenses eventually hurt future returns. That’s a short to median term margin issue rather than a long term one.

Neoclouds are way more screwed imo as they are GPU shells

It’s possible depreciation expenses eventually hurt future returns. That’s a short to median term margin issue rather than a long term one.

Neoclouds are way more screwed imo as they are GPU shells

November 12, 2025 at 9:50 AM

The point is this hyper focus on the infrastructure layer of Hyperscalers just seems misplaced.

It’s possible depreciation expenses eventually hurt future returns. That’s a short to median term margin issue rather than a long term one.

Neoclouds are way more screwed imo as they are GPU shells

It’s possible depreciation expenses eventually hurt future returns. That’s a short to median term margin issue rather than a long term one.

Neoclouds are way more screwed imo as they are GPU shells

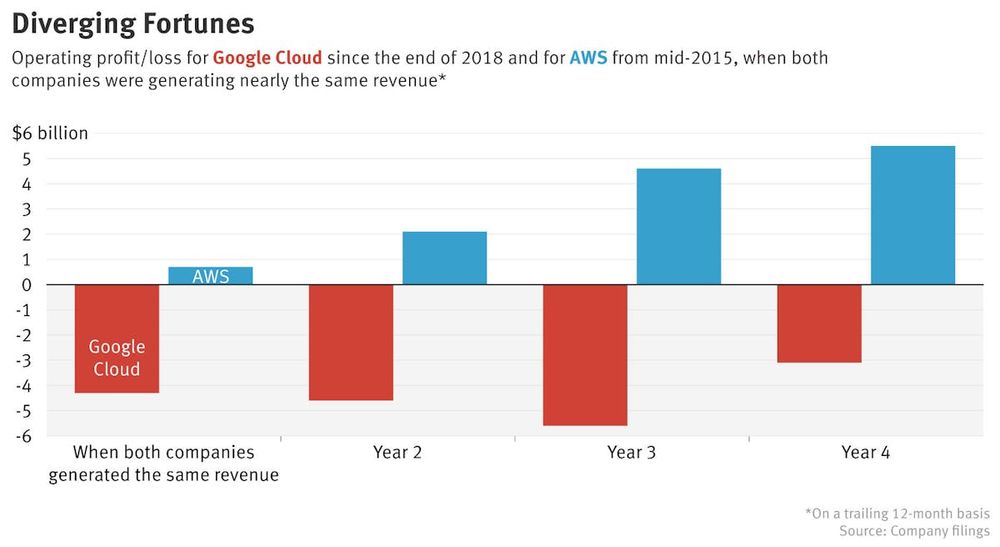

Also it wasn’t like people weren’t skeptical back then:

www.theinformation.com/articles/why...

www.bloomberg.com/news/article...

www.theregister.com/2022/02/02/a...

www.theinformation.com/articles/why...

www.bloomberg.com/news/article...

www.theregister.com/2022/02/02/a...

Why AWS Makes Money and Google Cloud Doesn’t

Google’s cloud computing arm is the company’s biggest hope of creating a substantial moneymaker outside of advertising, but it has been struggling to make up meaningful ground against industry pioneer...

www.theinformation.com

November 12, 2025 at 9:49 AM

Also it wasn’t like people weren’t skeptical back then:

www.theinformation.com/articles/why...

www.bloomberg.com/news/article...

www.theregister.com/2022/02/02/a...

www.theinformation.com/articles/why...

www.bloomberg.com/news/article...

www.theregister.com/2022/02/02/a...