Philipp Lieberknecht

@plieberk.bsky.social

Senior Economist @bundesbank. Monetary policy and financial markets. All views expressed here are my own.

Reposted by Philipp Lieberknecht

How to measure the broader monetary policy stance in the euro area?

In our latest @bundesbank.de report, we present the proxy monetary policy rate, which combines information from the risk-free yield curve and risk assets. 1\ #EconSky @plieberk.bsky.social

In our latest @bundesbank.de report, we present the proxy monetary policy rate, which combines information from the risk-free yield curve and risk assets. 1\ #EconSky @plieberk.bsky.social

March 20, 2025 at 1:36 PM

How to measure the broader monetary policy stance in the euro area?

In our latest @bundesbank.de report, we present the proxy monetary policy rate, which combines information from the risk-free yield curve and risk assets. 1\ #EconSky @plieberk.bsky.social

In our latest @bundesbank.de report, we present the proxy monetary policy rate, which combines information from the risk-free yield curve and risk assets. 1\ #EconSky @plieberk.bsky.social

Reposted by Philipp Lieberknecht

At @bundesbank.de, we have developed 𝗠𝗜𝗟𝗔 (𝗠𝗼𝗻𝗲𝘁𝗮𝗿𝘆-𝗜𝗻𝘁𝗲𝗹𝗹𝗶𝗴𝗲𝗻𝘁 𝗟𝗮𝗻𝗴𝘂𝗮𝗴𝗲 𝗔𝗴𝗲𝗻𝘁) - an AI tool designed to evaluate ECB communication, assessing individual sentences from monetary policy statements and speeches given in-document as well as the macro context. \1 #EconSky

March 18, 2025 at 8:55 PM

At @bundesbank.de, we have developed 𝗠𝗜𝗟𝗔 (𝗠𝗼𝗻𝗲𝘁𝗮𝗿𝘆-𝗜𝗻𝘁𝗲𝗹𝗹𝗶𝗴𝗲𝗻𝘁 𝗟𝗮𝗻𝗴𝘂𝗮𝗴𝗲 𝗔𝗴𝗲𝗻𝘁) - an AI tool designed to evaluate ECB communication, assessing individual sentences from monetary policy statements and speeches given in-document as well as the macro context. \1 #EconSky

Reposted by Philipp Lieberknecht

This is an important observation by @isabelschnabel.bsky.social:

Typically, tight monetary policy transmits also by increasing risk premia on financial markets. Without it, transmission is notably weaker.

During the recent hiking cycle, we did not observe this feature.

bsky.app/profile/flxg...

Typically, tight monetary policy transmits also by increasing risk premia on financial markets. Without it, transmission is notably weaker.

During the recent hiking cycle, we did not observe this feature.

bsky.app/profile/flxg...

Transmission: Our easing has been transmitted smoothly, as seen in short-term rates and bank lending rates. Sovereign bond yields have been broadly stable after a strong repricing in 2022, representing the new normal. Strong risk appetite has boosted equity prices and compressed credit spreads. 9/16

February 19, 2025 at 6:29 PM

This is an important observation by @isabelschnabel.bsky.social:

Typically, tight monetary policy transmits also by increasing risk premia on financial markets. Without it, transmission is notably weaker.

During the recent hiking cycle, we did not observe this feature.

bsky.app/profile/flxg...

Typically, tight monetary policy transmits also by increasing risk premia on financial markets. Without it, transmission is notably weaker.

During the recent hiking cycle, we did not observe this feature.

bsky.app/profile/flxg...

Reposted by Philipp Lieberknecht

Many #ECB watchers have waited for this article. Chart A shows the huge model uncertainty surrounding the estimates. Adding parameter and filter uncertainty, data revisions and considering all models (not just those available for Q4 2024), you can see what we know about r* ... very little.

Updated estimates of the euro area natural interest rate remain broadly unchanged since the end of 2023 following a modest post-pandemic increase, our latest #EconomicBulletin finds.

Read more here www.ecb.europa.eu/press/econom...

Read more here www.ecb.europa.eu/press/econom...

February 7, 2025 at 6:05 PM

Many #ECB watchers have waited for this article. Chart A shows the huge model uncertainty surrounding the estimates. Adding parameter and filter uncertainty, data revisions and considering all models (not just those available for Q4 2024), you can see what we know about r* ... very little.

Reposted by Philipp Lieberknecht

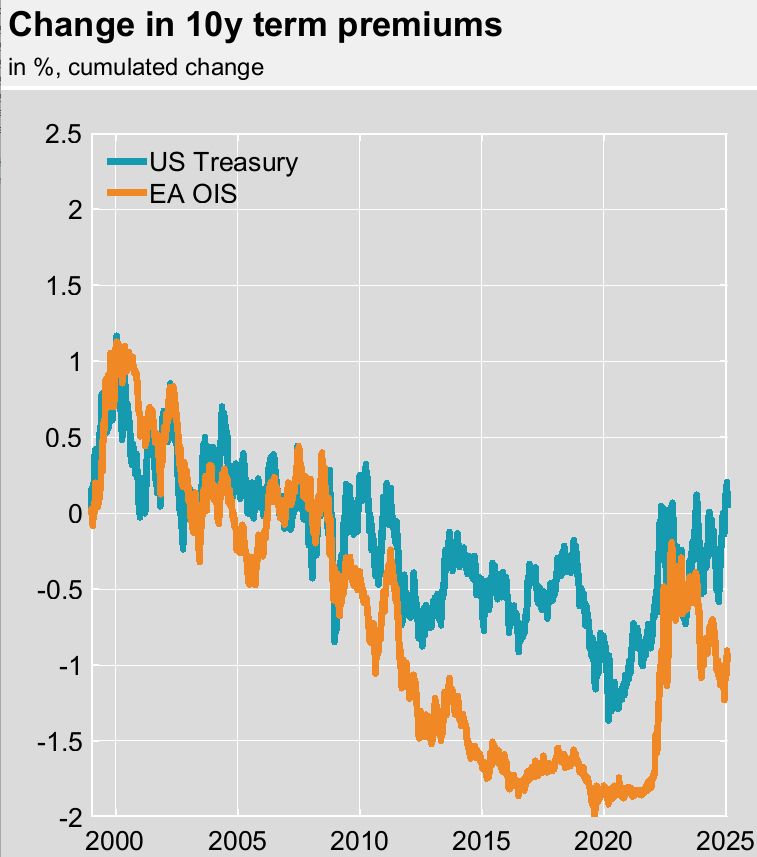

🧵As 𝘁𝗲𝗿𝗺 𝗽𝗿𝗲𝗺𝗶𝘂𝗺𝘀 took center stage these days - Chart depicts dynamics for US and EA 1/n

➡️99-12: strong co-movement

➡️12-20: EA term premium collapses relative to US

➡️22-24: de-compression more pronounced in EA

➡️since mid-24: degree of US term premium rise is only partly matched by EA

#EconSky

➡️99-12: strong co-movement

➡️12-20: EA term premium collapses relative to US

➡️22-24: de-compression more pronounced in EA

➡️since mid-24: degree of US term premium rise is only partly matched by EA

#EconSky

January 31, 2025 at 1:20 PM

🧵As 𝘁𝗲𝗿𝗺 𝗽𝗿𝗲𝗺𝗶𝘂𝗺𝘀 took center stage these days - Chart depicts dynamics for US and EA 1/n

➡️99-12: strong co-movement

➡️12-20: EA term premium collapses relative to US

➡️22-24: de-compression more pronounced in EA

➡️since mid-24: degree of US term premium rise is only partly matched by EA

#EconSky

➡️99-12: strong co-movement

➡️12-20: EA term premium collapses relative to US

➡️22-24: de-compression more pronounced in EA

➡️since mid-24: degree of US term premium rise is only partly matched by EA

#EconSky

Reposted by Philipp Lieberknecht

Important observation by @isabelschnabel.bsky.social

As bond holdings can be unwound only gradually, asset prices remain distorted for a long time. During the most recent tightening cycle, term and risk premia remained compressed, potentially distorting risk-taking behaviour. 1/3

As bond holdings can be unwound only gradually, asset prices remain distorted for a long time. During the most recent tightening cycle, term and risk premia remained compressed, potentially distorting risk-taking behaviour. 1/3

November 16, 2024 at 3:33 PM

Important observation by @isabelschnabel.bsky.social

As bond holdings can be unwound only gradually, asset prices remain distorted for a long time. During the most recent tightening cycle, term and risk premia remained compressed, potentially distorting risk-taking behaviour. 1/3

As bond holdings can be unwound only gradually, asset prices remain distorted for a long time. During the most recent tightening cycle, term and risk premia remained compressed, potentially distorting risk-taking behaviour. 1/3