@pedroserodio.com

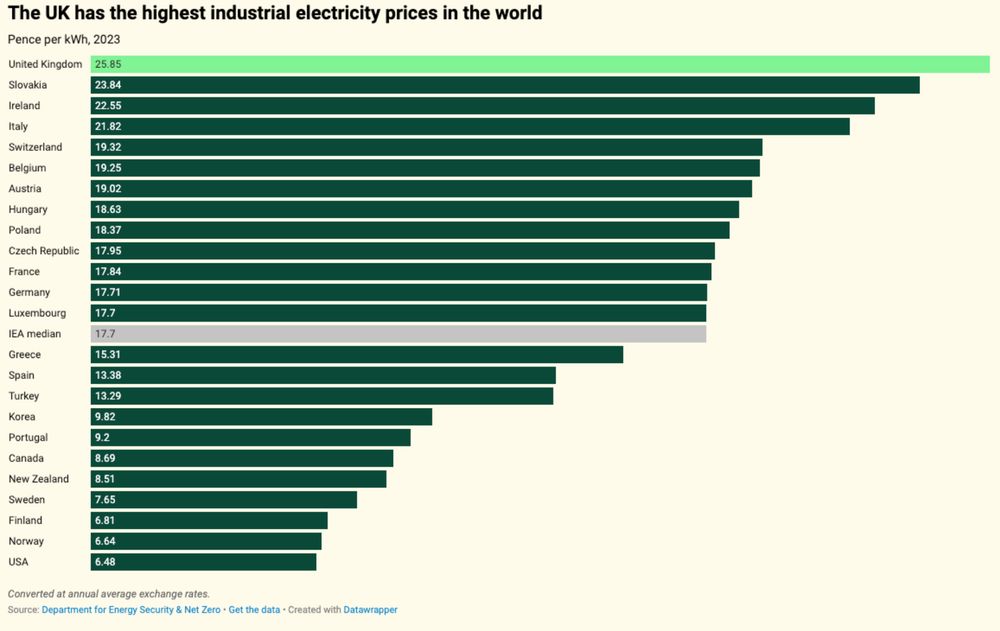

Overall, these effects are second-order. The fundamental issues of high input costs and availability: energy, industrial locations, and limited housing availability in key clusters create systematic disadvantages that no amount of capital can overcome.

June 19, 2025 at 7:54 AM

Overall, these effects are second-order. The fundamental issues of high input costs and availability: energy, industrial locations, and limited housing availability in key clusters create systematic disadvantages that no amount of capital can overcome.

The difference? Fintech operates where Britain has advantages: a strong sectoral cluster, low physical footprint, deep talent pools. Manufacturing firms or data centres face high energy costs and planning complexity.

June 19, 2025 at 7:54 AM

The difference? Fintech operates where Britain has advantages: a strong sectoral cluster, low physical footprint, deep talent pools. Manufacturing firms or data centres face high energy costs and planning complexity.

We can see this in the divide between different types of companies: UK fintech (Revolut, Monzo) readily access capital.

Manufacturing firms or those dependent on access to infrastructure struggle. Same financial system, very different outcomes.

Manufacturing firms or those dependent on access to infrastructure struggle. Same financial system, very different outcomes.

June 19, 2025 at 7:54 AM

We can see this in the divide between different types of companies: UK fintech (Revolut, Monzo) readily access capital.

Manufacturing firms or those dependent on access to infrastructure struggle. Same financial system, very different outcomes.

Manufacturing firms or those dependent on access to infrastructure struggle. Same financial system, very different outcomes.

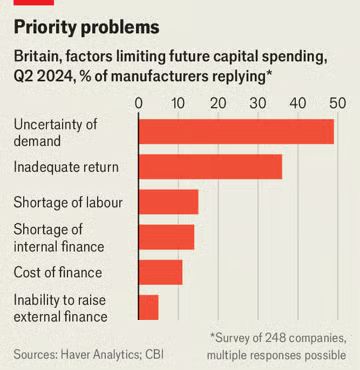

Forcing savers to invest in British companies addresses a symptom, but misses the underlying cause.

It also ignores what companies are telling us. UK manufacturers cite 'uncertainty of demand' and 'inadequate returns' as their main investment barriers, not the 'cost of finance'.

It also ignores what companies are telling us. UK manufacturers cite 'uncertainty of demand' and 'inadequate returns' as their main investment barriers, not the 'cost of finance'.

June 19, 2025 at 7:54 AM

Forcing savers to invest in British companies addresses a symptom, but misses the underlying cause.

It also ignores what companies are telling us. UK manufacturers cite 'uncertainty of demand' and 'inadequate returns' as their main investment barriers, not the 'cost of finance'.

It also ignores what companies are telling us. UK manufacturers cite 'uncertainty of demand' and 'inadequate returns' as their main investment barriers, not the 'cost of finance'.

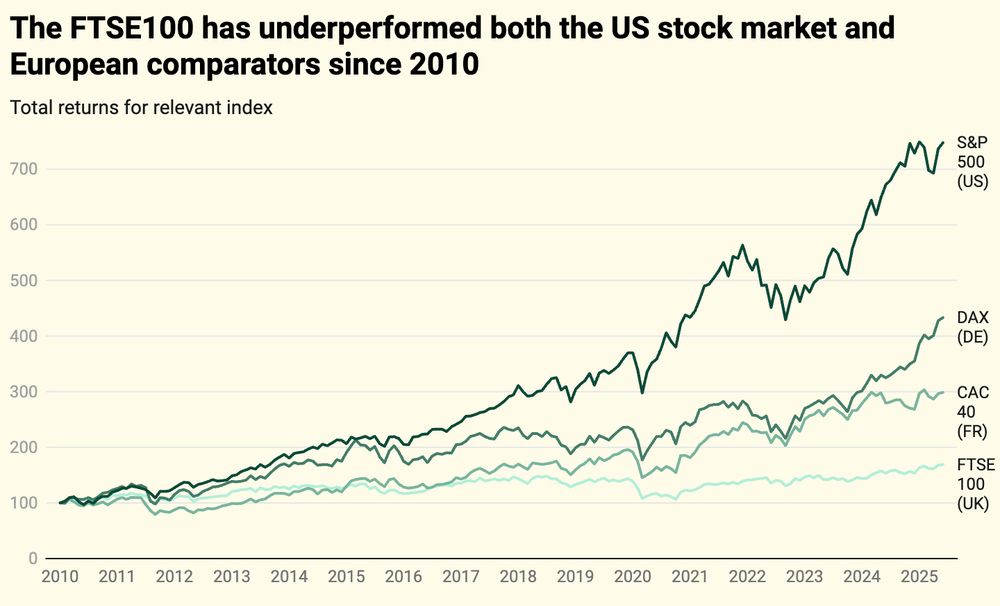

Will throwing more money at British companies actually help our economy?

Politicians keep threatening to direct British savings & pensions to UK equities. But this won’t fix the underlying reasons for Britain’s low investment & productivity – and could deliver worse returns. 🧵

Politicians keep threatening to direct British savings & pensions to UK equities. But this won’t fix the underlying reasons for Britain’s low investment & productivity – and could deliver worse returns. 🧵

June 19, 2025 at 7:54 AM

Will throwing more money at British companies actually help our economy?

Politicians keep threatening to direct British savings & pensions to UK equities. But this won’t fix the underlying reasons for Britain’s low investment & productivity – and could deliver worse returns. 🧵

Politicians keep threatening to direct British savings & pensions to UK equities. But this won’t fix the underlying reasons for Britain’s low investment & productivity – and could deliver worse returns. 🧵

When HMG policy is shaped by OBR forecasts, and Govt is pushing on reforms that the OBR toolkit wasn’t built for (like reg. reform), it creates a pressure to reshape the OBR's role and question whether it has become a political institution.

March 27, 2025 at 1:22 PM

When HMG policy is shaped by OBR forecasts, and Govt is pushing on reforms that the OBR toolkit wasn’t built for (like reg. reform), it creates a pressure to reshape the OBR's role and question whether it has become a political institution.

The approach underlying all OBR forecasting is now very far from the state of the art in macroeconomics.

Empirical evidence produced at the research frontier becomes less useful for forecasts - forcing the OBR to rely more on other sources, like Government produced figures.

Empirical evidence produced at the research frontier becomes less useful for forecasts - forcing the OBR to rely more on other sources, like Government produced figures.

March 27, 2025 at 1:22 PM

The approach underlying all OBR forecasting is now very far from the state of the art in macroeconomics.

Empirical evidence produced at the research frontier becomes less useful for forecasts - forcing the OBR to rely more on other sources, like Government produced figures.

Empirical evidence produced at the research frontier becomes less useful for forecasts - forcing the OBR to rely more on other sources, like Government produced figures.

This pressure is only going to intensify as governments have to make increasingly difficult choices on spending and taxation while trying to deliver structural reforms.

These affect long-term productivity growth, which the OBR’s toolkit is not designed to forecast.

These affect long-term productivity growth, which the OBR’s toolkit is not designed to forecast.

March 27, 2025 at 1:22 PM

This pressure is only going to intensify as governments have to make increasingly difficult choices on spending and taxation while trying to deliver structural reforms.

These affect long-term productivity growth, which the OBR’s toolkit is not designed to forecast.

These affect long-term productivity growth, which the OBR’s toolkit is not designed to forecast.

OBR forecasts are increasingly contentious; not only do they reflect Government policy, they increasingly shape it.

The 2022 mini-budget fallout is the starkest example of the OBR’s impact.

A 🧵on the pressure this puts on the OBR to get things right 👇

The 2022 mini-budget fallout is the starkest example of the OBR’s impact.

A 🧵on the pressure this puts on the OBR to get things right 👇

March 27, 2025 at 1:22 PM

OBR forecasts are increasingly contentious; not only do they reflect Government policy, they increasingly shape it.

The 2022 mini-budget fallout is the starkest example of the OBR’s impact.

A 🧵on the pressure this puts on the OBR to get things right 👇

The 2022 mini-budget fallout is the starkest example of the OBR’s impact.

A 🧵on the pressure this puts on the OBR to get things right 👇

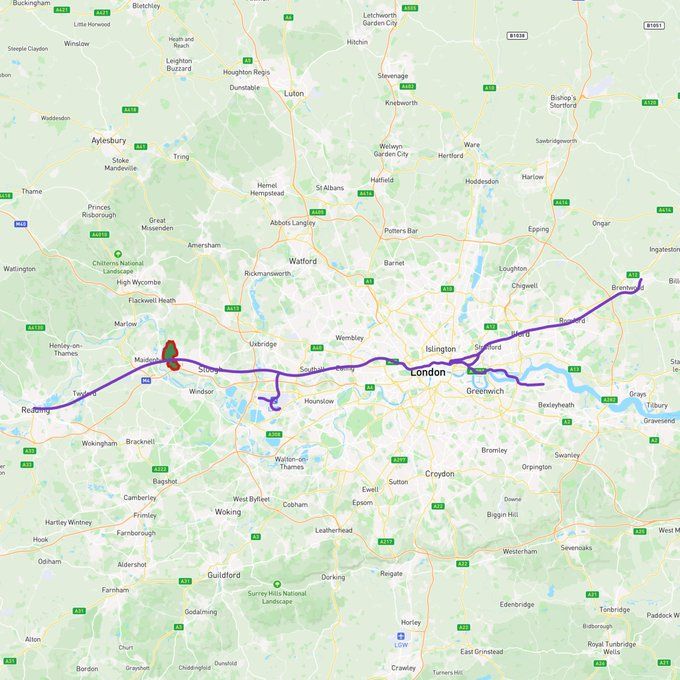

The locations we identified in the report offer good rail links, strong local economies, and underused land. For example, Taplow would allow for more than 20,000 homes being built in an area that would connect people to high-paying jobs.

January 21, 2025 at 2:35 PM

The locations we identified in the report offer good rail links, strong local economies, and underused land. For example, Taplow would allow for more than 20,000 homes being built in an area that would connect people to high-paying jobs.

We propose extensions of already successful areas, like Taplow on the Elizabeth Line or in smaller cities like York. To achieve this, we could deploy value capture mechanisms to ensure local infrastructure could be improved by the associated value uplift.

January 21, 2025 at 2:35 PM

We propose extensions of already successful areas, like Taplow on the Elizabeth Line or in smaller cities like York. To achieve this, we could deploy value capture mechanisms to ensure local infrastructure could be improved by the associated value uplift.

Historically, many towns and cities expanded through extensions of their boundaries, like Edinburgh New Town. This should be a key learning point: new towns should be linked to areas with pre-existing economic opportunity.

January 21, 2025 at 2:35 PM

Historically, many towns and cities expanded through extensions of their boundaries, like Edinburgh New Town. This should be a key learning point: new towns should be linked to areas with pre-existing economic opportunity.