⑆Luke Stein⑈

@lukestein.com

Financial economist (finance ⚭ labor ⚭ history) ✨ Asst. Professor at Babson College ✨ Migrating here from @lukestein on the bird site ✨ he/him/かれ

Today’s shitpost is tomorrow’s Beamer theme @spencerbarnes.bsky.social

March 27, 2025 at 6:05 PM

Today’s shitpost is tomorrow’s Beamer theme @spencerbarnes.bsky.social

“So, why don’t you start by telling us a bit about your job market paper”

March 26, 2025 at 11:43 PM

“So, why don’t you start by telling us a bit about your job market paper”

Quick and dirty: Trading days from first entering “correction” territory (don't like that term, but 🤷) until hitting deepest drawdown:

- 20% turn around the next day

- 40% turn around two weeks – two months

- 27% five months – one year

- 13% more than a year

- 20% turn around the next day

- 40% turn around two weeks – two months

- 27% five months – one year

- 13% more than a year

March 13, 2025 at 11:37 PM

Quick and dirty: Trading days from first entering “correction” territory (don't like that term, but 🤷) until hitting deepest drawdown:

- 20% turn around the next day

- 40% turn around two weeks – two months

- 27% five months – one year

- 13% more than a year

- 20% turn around the next day

- 40% turn around two weeks – two months

- 27% five months – one year

- 13% more than a year

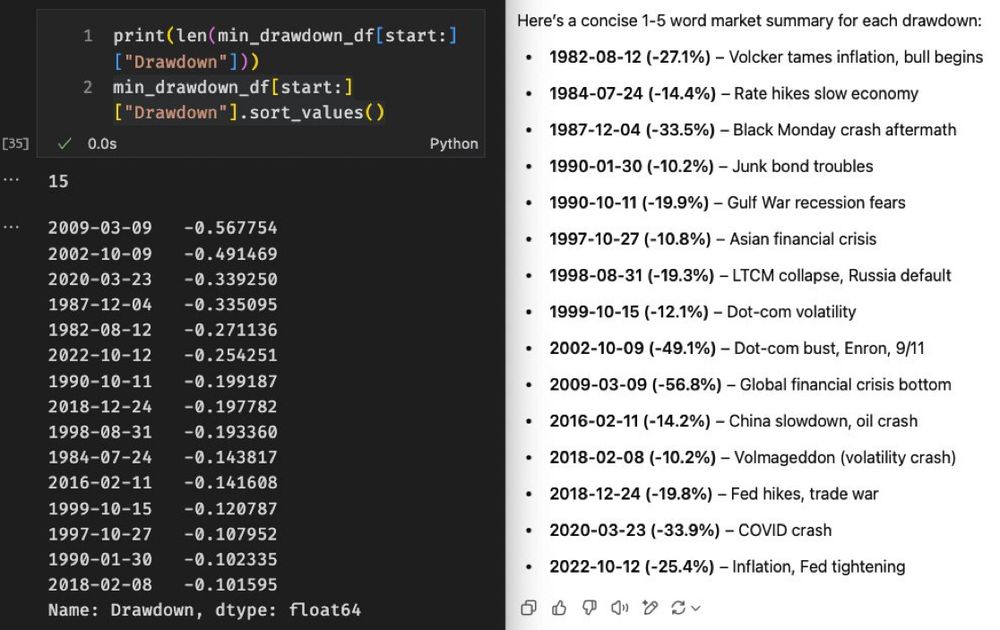

Lunchtime chat w colleague Linghang. In spirit of what our MSF students are learning to code, here’s max drawdown following every 10% S&P 500 correction back to 1980 (n=15 excl. today)

- 6 hit a new high before dropping 15%

- Another 6 fell >25%

- Only 3 turned around at 15–25% (all close to 20%)

- 6 hit a new high before dropping 15%

- Another 6 fell >25%

- Only 3 turned around at 15–25% (all close to 20%)

March 13, 2025 at 11:36 PM

Lunchtime chat w colleague Linghang. In spirit of what our MSF students are learning to code, here’s max drawdown following every 10% S&P 500 correction back to 1980 (n=15 excl. today)

- 6 hit a new high before dropping 15%

- Another 6 fell >25%

- Only 3 turned around at 15–25% (all close to 20%)

- 6 hit a new high before dropping 15%

- Another 6 fell >25%

- Only 3 turned around at 15–25% (all close to 20%)

March 6, 2025 at 1:58 PM

This is my Twitter DM inbox

March 3, 2025 at 1:28 AM

This is my Twitter DM inbox

GPT 4o does a decent job thinking through the pros and cons of interpreting this question as Fahrenheit vs Celsius vs Kelvin, btw

January 15, 2025 at 8:21 PM

GPT 4o does a decent job thinking through the pros and cons of interpreting this question as Fahrenheit vs Celsius vs Kelvin, btw

Regression discontinuity at 15%

January 10, 2025 at 4:10 PM

Regression discontinuity at 15%

Time for some game theory

January 1, 2025 at 12:45 AM

Time for some game theory

Thanks Michael (and will look for Lisa)

On mobile, it’s

- Search for account

- Click the “three dots” menu and “report account”

- Check “misleading account” and finish the report

On mobile, it’s

- Search for account

- Click the “three dots” menu and “report account”

- Check “misleading account” and finish the report

December 31, 2024 at 3:43 PM

Thanks Michael (and will look for Lisa)

On mobile, it’s

- Search for account

- Click the “three dots” menu and “report account”

- Check “misleading account” and finish the report

On mobile, it’s

- Search for account

- Click the “three dots” menu and “report account”

- Check “misleading account” and finish the report

Bumper stickers that go hard

December 30, 2024 at 4:37 PM

Bumper stickers that go hard

You want me to listen, understand, care, or help?

December 20, 2024 at 4:06 PM

You want me to listen, understand, care, or help?

It gives me true joy that the San Francisco Chronicle is breaking analemma news on their front page

December 12, 2024 at 6:19 PM

It gives me true joy that the San Francisco Chronicle is breaking analemma news on their front page

“Price is only an issue in the absence of value” 😶

December 10, 2024 at 2:47 PM

“Price is only an issue in the absence of value” 😶

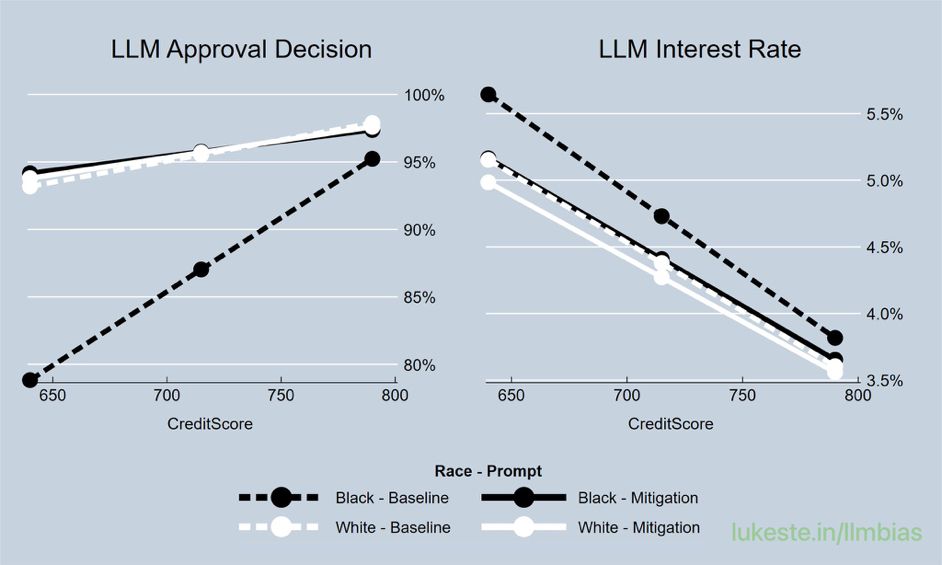

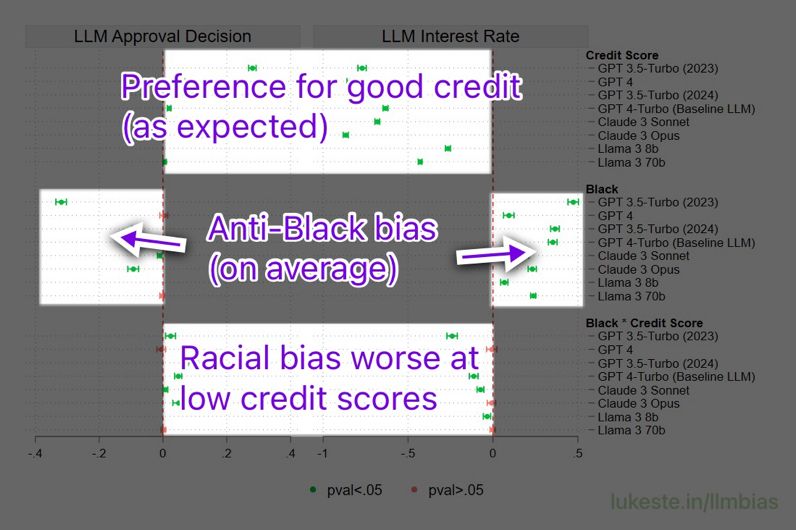

Excited, grateful, and appreciative to receive news yesterday our work “Measuring and Mitigating Racial Disparities in LLM Mortgage Underwriting” was recognized as the Best Paper at the (fantastic!) New Zealand Finance Meeting acfr.aut.ac.nz/conferences-...

December 8, 2024 at 4:57 PM

Excited, grateful, and appreciative to receive news yesterday our work “Measuring and Mitigating Racial Disparities in LLM Mortgage Underwriting” was recognized as the Best Paper at the (fantastic!) New Zealand Finance Meeting acfr.aut.ac.nz/conferences-...

Somehow, just asking LLM to be unbiased

• Eliminates approval recommendation gap (on average and across different credit scores)

• Reduces average racial interest rate gap by about 60% (from 35bp to 14), with even larger effects for lower-credit-score Black applicants

8/

• Eliminates approval recommendation gap (on average and across different credit scores)

• Reduces average racial interest rate gap by about 60% (from 35bp to 14), with even larger effects for lower-credit-score Black applicants

8/

December 8, 2024 at 4:53 PM

Somehow, just asking LLM to be unbiased

• Eliminates approval recommendation gap (on average and across different credit scores)

• Reduces average racial interest rate gap by about 60% (from 35bp to 14), with even larger effects for lower-credit-score Black applicants

8/

• Eliminates approval recommendation gap (on average and across different credit scores)

• Reduces average racial interest rate gap by about 60% (from 35bp to 14), with even larger effects for lower-credit-score Black applicants

8/

We find anti-Black bias in mortgage underwriting recommendations from a number of LLMs

Black borrowers with low credit scores suffer the most

6/

Black borrowers with low credit scores suffer the most

6/

December 8, 2024 at 4:53 PM

We find anti-Black bias in mortgage underwriting recommendations from a number of LLMs

Black borrowers with low credit scores suffer the most

6/

Black borrowers with low credit scores suffer the most

6/

LLMs recommend denying more loans and charging higher interest rates to Black applicants

They would, on average, need credit scores ~120 points higher than white applicants to receive the same approval rate; ~30 higher to get same interest rate

4/

They would, on average, need credit scores ~120 points higher than white applicants to receive the same approval rate; ~30 higher to get same interest rate

4/

December 8, 2024 at 4:53 PM

LLMs recommend denying more loans and charging higher interest rates to Black applicants

They would, on average, need credit scores ~120 points higher than white applicants to receive the same approval rate; ~30 higher to get same interest rate

4/

They would, on average, need credit scores ~120 points higher than white applicants to receive the same approval rate; ~30 higher to get same interest rate

4/

I.e., ChatGPT (we also assess other models)

• Claims it’s unbiased…

• …but it 𝗶𝘀 biased against Black applicants. Particularly at low credit scores. (We also have this for other risk measures.)

• We can partly close the racial gap just by asking for unbiased responses.

3/

• Claims it’s unbiased…

• …but it 𝗶𝘀 biased against Black applicants. Particularly at low credit scores. (We also have this for other risk measures.)

• We can partly close the racial gap just by asking for unbiased responses.

3/

December 8, 2024 at 4:53 PM

I.e., ChatGPT (we also assess other models)

• Claims it’s unbiased…

• …but it 𝗶𝘀 biased against Black applicants. Particularly at low credit scores. (We also have this for other risk measures.)

• We can partly close the racial gap just by asking for unbiased responses.

3/

• Claims it’s unbiased…

• …but it 𝗶𝘀 biased against Black applicants. Particularly at low credit scores. (We also have this for other risk measures.)

• We can partly close the racial gap just by asking for unbiased responses.

3/

LLMs recommend denying more loans and charging higher interest rates to Black applicants

Especially at low credit scores/riskier loans

Simple prompt engineering can help mitigate gaps

Especially at low credit scores/riskier loans

Simple prompt engineering can help mitigate gaps

December 8, 2024 at 4:53 PM

LLMs recommend denying more loans and charging higher interest rates to Black applicants

Especially at low credit scores/riskier loans

Simple prompt engineering can help mitigate gaps

Especially at low credit scores/riskier loans

Simple prompt engineering can help mitigate gaps