Emily Fry

@emilyfry.bsky.social

Senior Economist at Resolution Foundation, researching trade, growth and living standards.

Instead, what matters is where high-value firms & functions - like headquarters - cluster.

FTSE listed companies are most likely to headquarter in London, and much less likely to headquarter in Birmingham, for example.

FTSE listed companies are most likely to headquarter in London, and much less likely to headquarter in Birmingham, for example.

June 23, 2025 at 11:04 AM

Instead, what matters is where high-value firms & functions - like headquarters - cluster.

FTSE listed companies are most likely to headquarter in London, and much less likely to headquarter in Birmingham, for example.

FTSE listed companies are most likely to headquarter in London, and much less likely to headquarter in Birmingham, for example.

So what about differences in industry mix, occupations and firm size across England? We find that these explain little of the differences in pay between places. Most of the variation in pay is within industries and within firm size (the light blue bars in the chart below).

June 23, 2025 at 11:04 AM

So what about differences in industry mix, occupations and firm size across England? We find that these explain little of the differences in pay between places. Most of the variation in pay is within industries and within firm size (the light blue bars in the chart below).

So, how does place drive regional pay inequality?

One explanation is agglomeration - i.e. larger labour markets pay more. But we find that doubling a labour market’s size lifts pay by only 3.9 per cent, explaining just 24 per cent of the place premium.

One explanation is agglomeration - i.e. larger labour markets pay more. But we find that doubling a labour market’s size lifts pay by only 3.9 per cent, explaining just 24 per cent of the place premium.

June 23, 2025 at 11:04 AM

So, how does place drive regional pay inequality?

One explanation is agglomeration - i.e. larger labour markets pay more. But we find that doubling a labour market’s size lifts pay by only 3.9 per cent, explaining just 24 per cent of the place premium.

One explanation is agglomeration - i.e. larger labour markets pay more. But we find that doubling a labour market’s size lifts pay by only 3.9 per cent, explaining just 24 per cent of the place premium.

Previously, research found that just 12% of the differences in pay was due to place. But using new methods, and new data, we find that *one-third* (34%) of the pay gap between areas is place.

Move an average worker from Dudley to Harrogate and they pocket an extra £1,300 a year (~5 per cent).

Move an average worker from Dudley to Harrogate and they pocket an extra £1,300 a year (~5 per cent).

June 23, 2025 at 11:04 AM

Previously, research found that just 12% of the differences in pay was due to place. But using new methods, and new data, we find that *one-third* (34%) of the pay gap between areas is place.

Move an average worker from Dudley to Harrogate and they pocket an extra £1,300 a year (~5 per cent).

Move an average worker from Dudley to Harrogate and they pocket an extra £1,300 a year (~5 per cent).

Pay varies hugely across England: in 2024 weekly pay was just £610 in Liskeard to £1,130 in London.

Is this because high‑earning areas attract inherently higher‑earning people, or because the jobs located there pay more to any worker?

Our new @resfoundation.bsky.social report finds out.

Is this because high‑earning areas attract inherently higher‑earning people, or because the jobs located there pay more to any worker?

Our new @resfoundation.bsky.social report finds out.

June 23, 2025 at 11:04 AM

Pay varies hugely across England: in 2024 weekly pay was just £610 in Liskeard to £1,130 in London.

Is this because high‑earning areas attract inherently higher‑earning people, or because the jobs located there pay more to any worker?

Our new @resfoundation.bsky.social report finds out.

Is this because high‑earning areas attract inherently higher‑earning people, or because the jobs located there pay more to any worker?

Our new @resfoundation.bsky.social report finds out.

As of February, the biggest contributor to that surge is... non-ferrous metals.

Exports of non-ferrous metals to the US (aluminium, copper, and *precious metals*) are up 1,358% since Feb 2024.

This isn't a global trend: exports to the RoW fell 50% since Feb 2024.

Exports of non-ferrous metals to the US (aluminium, copper, and *precious metals*) are up 1,358% since Feb 2024.

This isn't a global trend: exports to the RoW fell 50% since Feb 2024.

May 1, 2025 at 11:16 AM

As of February, the biggest contributor to that surge is... non-ferrous metals.

Exports of non-ferrous metals to the US (aluminium, copper, and *precious metals*) are up 1,358% since Feb 2024.

This isn't a global trend: exports to the RoW fell 50% since Feb 2024.

Exports of non-ferrous metals to the US (aluminium, copper, and *precious metals*) are up 1,358% since Feb 2024.

This isn't a global trend: exports to the RoW fell 50% since Feb 2024.

There has been a lot of focus on the UK's direct export exposure to the US, but this chart is the one that worries me.

In 2019, $24bn worth of UK motor vehicle value added ended up in the US via supply chains.

That’s 22% of ALL Britain’s motor vehicle output.

In 2019, $24bn worth of UK motor vehicle value added ended up in the US via supply chains.

That’s 22% of ALL Britain’s motor vehicle output.

April 14, 2025 at 4:22 PM

There has been a lot of focus on the UK's direct export exposure to the US, but this chart is the one that worries me.

In 2019, $24bn worth of UK motor vehicle value added ended up in the US via supply chains.

That’s 22% of ALL Britain’s motor vehicle output.

In 2019, $24bn worth of UK motor vehicle value added ended up in the US via supply chains.

That’s 22% of ALL Britain’s motor vehicle output.

New analysis from the OBR reckons that - depending on how many countries are affected by US tariffs and if countries retaliate - the impact to the UK could peak at a 1% hit to GDP in 2026-27, and a 0.75% hit to GDP in the medium term.

obr.uk/efo/economic...

obr.uk/efo/economic...

March 28, 2025 at 11:27 AM

New analysis from the OBR reckons that - depending on how many countries are affected by US tariffs and if countries retaliate - the impact to the UK could peak at a 1% hit to GDP in 2026-27, and a 0.75% hit to GDP in the medium term.

obr.uk/efo/economic...

obr.uk/efo/economic...

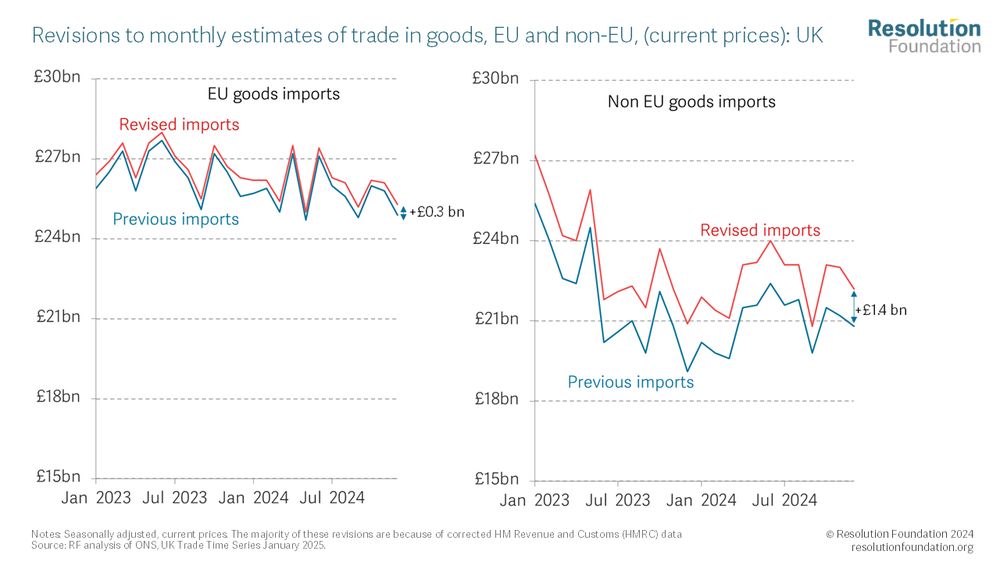

Goods imports have been revised upwards too, driven mainly by an increase in imports from Non-EU of 7.2% in 2023 (mainly from China and Japan rather than the US). Imports from the EU were revised upwards - by 1.4% in 2023.

March 28, 2025 at 11:16 AM

Goods imports have been revised upwards too, driven mainly by an increase in imports from Non-EU of 7.2% in 2023 (mainly from China and Japan rather than the US). Imports from the EU were revised upwards - by 1.4% in 2023.

First, services trade has been revised upwards by 4.1% in 2023 & 6.7% in 2024, driven by stronger services exports in particular (up 5.1% in 2023 & 7.3% in 2024, in total worth £34.3 bn in 2024).

Services imports were also revised upwards (up 2.7% in 2023 & 5.7% in 2024, worth £17.1 bn in 2024)

Services imports were also revised upwards (up 2.7% in 2023 & 5.7% in 2024, worth £17.1 bn in 2024)

March 28, 2025 at 11:16 AM

First, services trade has been revised upwards by 4.1% in 2023 & 6.7% in 2024, driven by stronger services exports in particular (up 5.1% in 2023 & 7.3% in 2024, in total worth £34.3 bn in 2024).

Services imports were also revised upwards (up 2.7% in 2023 & 5.7% in 2024, worth £17.1 bn in 2024)

Services imports were also revised upwards (up 2.7% in 2023 & 5.7% in 2024, worth £17.1 bn in 2024)

Btw Dec 2024 & Jan 2025, goods exports rose by 6.3%, driven by strong growth in exports to Non-EU. Monthly goods data is volatile so we shouldn't read too much into this rise.

Goods imports were unchanged overall, although imports from the EU fell by 2.6%, while imports from Non-EU rose by 2.9%.

Goods imports were unchanged overall, although imports from the EU fell by 2.6%, while imports from Non-EU rose by 2.9%.

March 28, 2025 at 11:16 AM

Btw Dec 2024 & Jan 2025, goods exports rose by 6.3%, driven by strong growth in exports to Non-EU. Monthly goods data is volatile so we shouldn't read too much into this rise.

Goods imports were unchanged overall, although imports from the EU fell by 2.6%, while imports from Non-EU rose by 2.9%.

Goods imports were unchanged overall, although imports from the EU fell by 2.6%, while imports from Non-EU rose by 2.9%.

5) This leaves slightly smaller cuts to unprotected departments than expected in the Autumn (now £8.6bn vs £9.7bn of cuts). But they face feast and famine: distributed evenly these cuts mean 4.5% cuts for each unprotected department, undoing two-thirds of the front loaded Autumn spending injections.

March 27, 2025 at 11:38 AM

5) This leaves slightly smaller cuts to unprotected departments than expected in the Autumn (now £8.6bn vs £9.7bn of cuts). But they face feast and famine: distributed evenly these cuts mean 4.5% cuts for each unprotected department, undoing two-thirds of the front loaded Autumn spending injections.

4) Even with this change, much of the spending increase is front loaded. Growth in real RDEL per capita is set to slow sharply to just 0.8% between 2025-26 and 2029-30, only slightly higher than the 0.5% at the 2024 Spring Budget (although much higher than 1.7% annual cuts during austerity).

March 27, 2025 at 11:38 AM

4) Even with this change, much of the spending increase is front loaded. Growth in real RDEL per capita is set to slow sharply to just 0.8% between 2025-26 and 2029-30, only slightly higher than the 0.5% at the 2024 Spring Budget (although much higher than 1.7% annual cuts during austerity).

3) How are we getting to 2.5% of GDP on Defence by the end of the Parliament? Capital spending: 92% (£6.4 billion) of the rise in Defence spending by 2029-30 is investment, with only 8 per cent coming in the form of higher RDEL.

March 27, 2025 at 11:38 AM

3) How are we getting to 2.5% of GDP on Defence by the end of the Parliament? Capital spending: 92% (£6.4 billion) of the rise in Defence spending by 2029-30 is investment, with only 8 per cent coming in the form of higher RDEL.

2) The cuts to overseas aid last month were billed as paying for higher defence spending. But we learned yesterday that only one-fifth of the cut to ODA RDEL in 2029-30 has been reallocated to defence (£0.6 billion), leaving £2.6 billion available for other departments.

March 27, 2025 at 11:38 AM

2) The cuts to overseas aid last month were billed as paying for higher defence spending. But we learned yesterday that only one-fifth of the cut to ODA RDEL in 2029-30 has been reallocated to defence (£0.6 billion), leaving £2.6 billion available for other departments.

A couple of striking charts from our spending response to the Chancellor's Spring Statement yesterday.

1) Despite it being billed as a spending consolidation, real terms spending will be +£1.1 billion higher over the years of the 2025 Spending Review than it was expected to be in the Autumn Budget.

1) Despite it being billed as a spending consolidation, real terms spending will be +£1.1 billion higher over the years of the 2025 Spending Review than it was expected to be in the Autumn Budget.

March 27, 2025 at 11:38 AM

A couple of striking charts from our spending response to the Chancellor's Spring Statement yesterday.

1) Despite it being billed as a spending consolidation, real terms spending will be +£1.1 billion higher over the years of the 2025 Spending Review than it was expected to be in the Autumn Budget.

1) Despite it being billed as a spending consolidation, real terms spending will be +£1.1 billion higher over the years of the 2025 Spending Review than it was expected to be in the Autumn Budget.

Basic metals production is heavily concentrated in West Wales, East Wales, East Yorkshire, Northern Lincolnshire & South Yorkshire—so these areas will feel the impact most.

March 12, 2025 at 1:32 PM

Basic metals production is heavily concentrated in West Wales, East Wales, East Yorkshire, Northern Lincolnshire & South Yorkshire—so these areas will feel the impact most.

These shifts in goods and services trade, and normalising of energy prices, mean that the UK’s terms of trade recovered throughout 2024, returning in the final quarter of 2024 to levels last seen in 2018

February 13, 2025 at 9:02 AM

These shifts in goods and services trade, and normalising of energy prices, mean that the UK’s terms of trade recovered throughout 2024, returning in the final quarter of 2024 to levels last seen in 2018

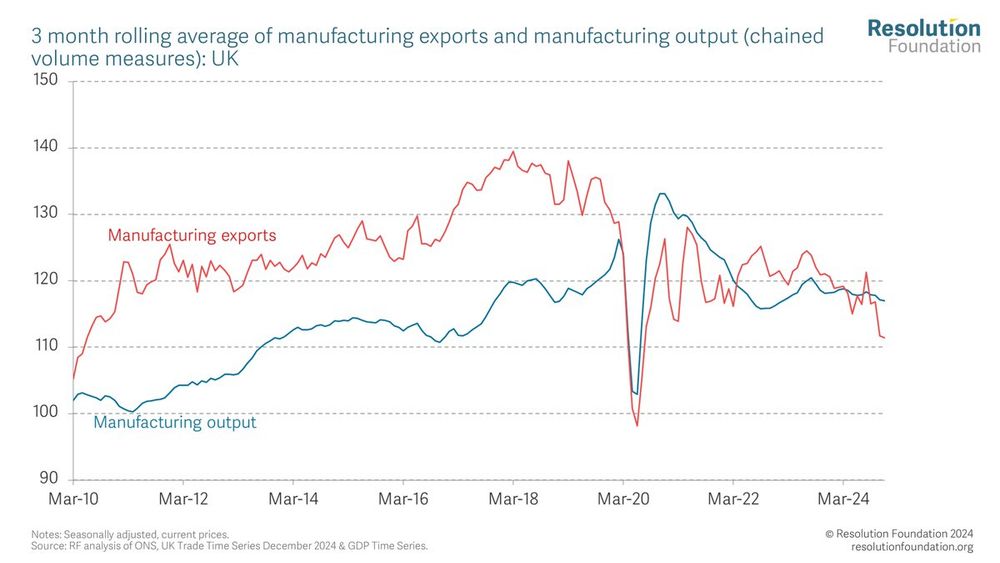

In goods, the weakness in UK exports has been broad based since 2019. Aside from crude materials, all categories have declined - especially chemicals and miscellaneous manufactures. Overall, between 2019 and 2024, goods exports fell by 16.2%, while goods imports dropped by 4.7% in volume terms.

February 13, 2025 at 9:02 AM

In goods, the weakness in UK exports has been broad based since 2019. Aside from crude materials, all categories have declined - especially chemicals and miscellaneous manufactures. Overall, between 2019 and 2024, goods exports fell by 16.2%, while goods imports dropped by 4.7% in volume terms.

Professional services are booming outside London - especially in the East and Scotland - while London’s information and communication sector has grown by 15% a year since 2016.

February 13, 2025 at 9:02 AM

Professional services are booming outside London - especially in the East and Scotland - while London’s information and communication sector has grown by 15% a year since 2016.

For services, a key question is where this activity is taking place? New data for 2022 offers good news: while London still dominates in total exports, cities like Manchester, Edinburgh, and Belfast have grown their services exports faster than London between 2016 and 2022.

February 13, 2025 at 9:02 AM

For services, a key question is where this activity is taking place? New data for 2022 offers good news: while London still dominates in total exports, cities like Manchester, Edinburgh, and Belfast have grown their services exports faster than London between 2016 and 2022.

This is in line with UK GDP which grew 0.1% in Q4 2024, driven by strong services. Meanwhile, production output fell by 0.8% between Q3 and Q4 2024, driven by a decline in manufacturing output which matches the decline in goods exports.

February 13, 2025 at 9:02 AM

This is in line with UK GDP which grew 0.1% in Q4 2024, driven by strong services. Meanwhile, production output fell by 0.8% between Q3 and Q4 2024, driven by a decline in manufacturing output which matches the decline in goods exports.

First, the UK’s quarterly performance (Q3 vs Q4 2024) was weak for goods exports in particular: falling 5% to the EU and 5.2% to Non-EU in volume terms. Goods imports from the EU grew 2.1% while they shrunk 0.2% from Non-EU. Services exports grew 1.2% and imports grew 2.1%.

February 13, 2025 at 9:02 AM

First, the UK’s quarterly performance (Q3 vs Q4 2024) was weak for goods exports in particular: falling 5% to the EU and 5.2% to Non-EU in volume terms. Goods imports from the EU grew 2.1% while they shrunk 0.2% from Non-EU. Services exports grew 1.2% and imports grew 2.1%.

What does the UK buy from the US: oil and gas. What does the UK sell to the US: chemicals and cars.

February 3, 2025 at 12:17 PM

What does the UK buy from the US: oil and gas. What does the UK sell to the US: chemicals and cars.

As the UK navigates this uncertainty, it is worth remembering that around 2/3 of our goods are ultimately imported.

February 3, 2025 at 11:26 AM

As the UK navigates this uncertainty, it is worth remembering that around 2/3 of our goods are ultimately imported.