Vasudeva Ramaswamy

@vramaswamy.bsky.social

Postdoctoral Fellow at the Institute for Macroeconomic Policy & Analysis. Econ PhD Job Market Candidate from American University. Macroeconomics, Inequality, Economic History, Financial Markets. https://vasudeva-ram.github.io.

Because worker effort affects measured productivity over the cycle, it has important implications for inflation and business cycle dynamics. We have a paper covering that, and labor effort plays a big role there.

bsky.app/profile/vram...

bsky.app/profile/vram...

On the #EconJobMarket!

When does inflation increase slowly ("hump-shaped") vs rapidly? When do different drivers (wages, markups, etc) play bigger roles?

My #JMP explores these Qs by bringing a key variable back to the center of the debate: capacity utilization

A thread 🧵👇

When does inflation increase slowly ("hump-shaped") vs rapidly? When do different drivers (wages, markups, etc) play bigger roles?

My #JMP explores these Qs by bringing a key variable back to the center of the debate: capacity utilization

A thread 🧵👇

January 30, 2025 at 10:21 PM

Because worker effort affects measured productivity over the cycle, it has important implications for inflation and business cycle dynamics. We have a paper covering that, and labor effort plays a big role there.

bsky.app/profile/vram...

bsky.app/profile/vram...

Lewis & Villa (2019) is a working paper that looks at labor effort and productivity in the Euro area. Vivian Lewis has another paper with Dossche and Gazzani in RED on the role of effort in the OECD countries.

January 30, 2025 at 10:16 PM

Lewis & Villa (2019) is a working paper that looks at labor effort and productivity in the Euro area. Vivian Lewis has another paper with Dossche and Gazzani in RED on the role of effort in the OECD countries.

Thank you for reading! Grateful to my co-author

@Nacho2G

and PhD advisors for their support.

More on my profile: vasudeva-ram.github.io

Full paper and other research: vasudeva-ram.github.io/research/

Comments welcome!

@Nacho2G

and PhD advisors for their support.

More on my profile: vasudeva-ram.github.io

Full paper and other research: vasudeva-ram.github.io/research/

Comments welcome!

Vasudeva Ramaswamy

Personal website of Vasudeva Ramaswamy, post-doctoral fellow at the Institute for Macroeconomic and Policy Analysis.

vasudeva-ram.github.io

November 27, 2024 at 7:15 PM

Thank you for reading! Grateful to my co-author

@Nacho2G

and PhD advisors for their support.

More on my profile: vasudeva-ram.github.io

Full paper and other research: vasudeva-ram.github.io/research/

Comments welcome!

@Nacho2G

and PhD advisors for their support.

More on my profile: vasudeva-ram.github.io

Full paper and other research: vasudeva-ram.github.io/research/

Comments welcome!

Policy relevance 2️⃣

Markups, wages, profits are state-dependent on rate of capacity utilization. This has implications for

→ Wealth and income inequality over cycle

→ Optimal tax & transfer design over cycle

Future work: optimal monetary & tax policy in this framework

Markups, wages, profits are state-dependent on rate of capacity utilization. This has implications for

→ Wealth and income inequality over cycle

→ Optimal tax & transfer design over cycle

Future work: optimal monetary & tax policy in this framework

November 27, 2024 at 7:15 PM

Policy relevance 2️⃣

Markups, wages, profits are state-dependent on rate of capacity utilization. This has implications for

→ Wealth and income inequality over cycle

→ Optimal tax & transfer design over cycle

Future work: optimal monetary & tax policy in this framework

Markups, wages, profits are state-dependent on rate of capacity utilization. This has implications for

→ Wealth and income inequality over cycle

→ Optimal tax & transfer design over cycle

Future work: optimal monetary & tax policy in this framework

Policy relevance 1️⃣

Provides framework to study key trade-off for monetary policy when capacity is tight:

⭐️Textbook: R ⬆️ → demand ⬇️ →inflation ⬇️ 😀

⭐️But also: R ⬆️ → slow capacity expansion → markups ⬆️ →inflation ⬆️ 😡

Echoes recent analysis by

@employamerica.bsky.social

Provides framework to study key trade-off for monetary policy when capacity is tight:

⭐️Textbook: R ⬆️ → demand ⬇️ →inflation ⬇️ 😀

⭐️But also: R ⬆️ → slow capacity expansion → markups ⬆️ →inflation ⬆️ 😡

Echoes recent analysis by

@employamerica.bsky.social

November 27, 2024 at 7:15 PM

Policy relevance 1️⃣

Provides framework to study key trade-off for monetary policy when capacity is tight:

⭐️Textbook: R ⬆️ → demand ⬇️ →inflation ⬇️ 😀

⭐️But also: R ⬆️ → slow capacity expansion → markups ⬆️ →inflation ⬆️ 😡

Echoes recent analysis by

@employamerica.bsky.social

Provides framework to study key trade-off for monetary policy when capacity is tight:

⭐️Textbook: R ⬆️ → demand ⬇️ →inflation ⬇️ 😀

⭐️But also: R ⬆️ → slow capacity expansion → markups ⬆️ →inflation ⬆️ 😡

Echoes recent analysis by

@employamerica.bsky.social

Do the data support this mechanism? Yes.

We estimate our model using Bayesian IRF matching and find a very good fit for key variables to MP shocks.

Bottom line: NK models with capacity utilization can potentially explain both recent as well as historical inflation behavior

We estimate our model using Bayesian IRF matching and find a very good fit for key variables to MP shocks.

Bottom line: NK models with capacity utilization can potentially explain both recent as well as historical inflation behavior

November 27, 2024 at 7:15 PM

Do the data support this mechanism? Yes.

We estimate our model using Bayesian IRF matching and find a very good fit for key variables to MP shocks.

Bottom line: NK models with capacity utilization can potentially explain both recent as well as historical inflation behavior

We estimate our model using Bayesian IRF matching and find a very good fit for key variables to MP shocks.

Bottom line: NK models with capacity utilization can potentially explain both recent as well as historical inflation behavior

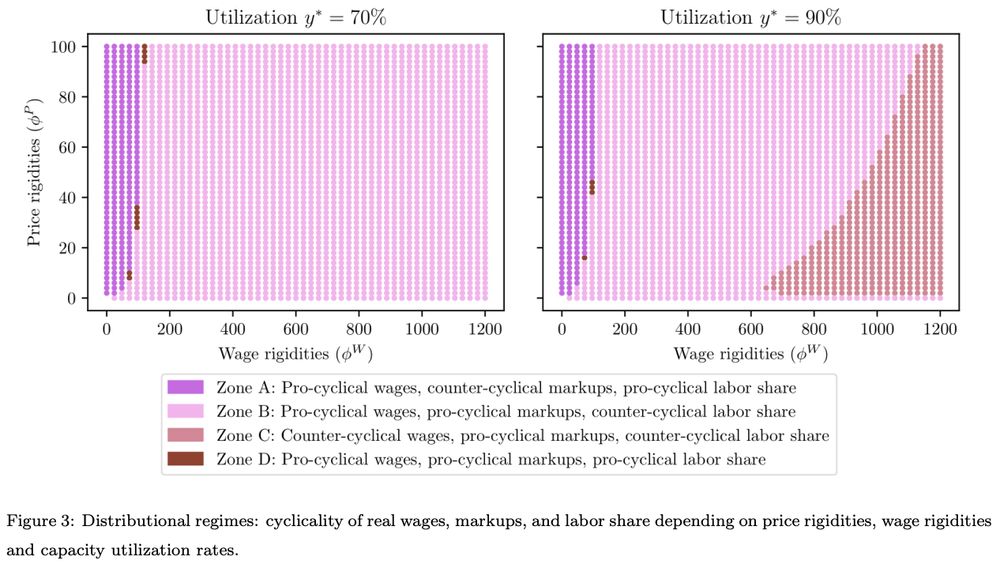

Do markups always increase following expansionary shocks? Not necessarily!

Procyclical markups are more likely when:

➡️ High utilization rate y* when shock occurs

➡️ Prices have relatively lower nominal rigidities than wages

Procyclical markups are more likely when:

➡️ High utilization rate y* when shock occurs

➡️ Prices have relatively lower nominal rigidities than wages

November 27, 2024 at 7:15 PM

Do markups always increase following expansionary shocks? Not necessarily!

Procyclical markups are more likely when:

➡️ High utilization rate y* when shock occurs

➡️ Prices have relatively lower nominal rigidities than wages

Procyclical markups are more likely when:

➡️ High utilization rate y* when shock occurs

➡️ Prices have relatively lower nominal rigidities than wages

In technical terms, the linearized Phillips Curve depends on the point around which it is linearized

⭐️ Capacity utilization rate y* appears as a state variable in the linearized PC

⭐️ Reflects nonlinearities due to *product market* tightness

⭐️ Capacity utilization rate y* appears as a state variable in the linearized PC

⭐️ Reflects nonlinearities due to *product market* tightness

November 27, 2024 at 7:15 PM

In technical terms, the linearized Phillips Curve depends on the point around which it is linearized

⭐️ Capacity utilization rate y* appears as a state variable in the linearized PC

⭐️ Reflects nonlinearities due to *product market* tightness

⭐️ Capacity utilization rate y* appears as a state variable in the linearized PC

⭐️ Reflects nonlinearities due to *product market* tightness

⭐️When y* is low → productivity effects dominate, inflation displays typical "hump-shaped" response (left panel)

⭐️When y* is high → inflation responds immediately, driven primarily by higher markups and muted productivity effects (right panel)

⭐️When y* is high → inflation responds immediately, driven primarily by higher markups and muted productivity effects (right panel)

November 27, 2024 at 7:15 PM

⭐️When y* is low → productivity effects dominate, inflation displays typical "hump-shaped" response (left panel)

⭐️When y* is high → inflation responds immediately, driven primarily by higher markups and muted productivity effects (right panel)

⭐️When y* is high → inflation responds immediately, driven primarily by higher markups and muted productivity effects (right panel)

Inflation reflects competing pressures:

⭐️Higher markups + wages → upward pressure

⭐️Higher productivity → downward pressure

Final inflation response therefore depends on which effects dominate and depends nonlinearly on utilization rate (y*).

⭐️Higher markups + wages → upward pressure

⭐️Higher productivity → downward pressure

Final inflation response therefore depends on which effects dominate and depends nonlinearly on utilization rate (y*).

November 27, 2024 at 7:15 PM

Inflation reflects competing pressures:

⭐️Higher markups + wages → upward pressure

⭐️Higher productivity → downward pressure

Final inflation response therefore depends on which effects dominate and depends nonlinearly on utilization rate (y*).

⭐️Higher markups + wages → upward pressure

⭐️Higher productivity → downward pressure

Final inflation response therefore depends on which effects dominate and depends nonlinearly on utilization rate (y*).

After expansionary monetary policy shocks, our model predicts 2 novel outcomes:

1️⃣ Firms have higher productivity due to higher worker effort and utilizing idle capacity

2️⃣ Firms raise prices thru higher markups to manage excess demand & maintain precautionary capacity

1️⃣ Firms have higher productivity due to higher worker effort and utilizing idle capacity

2️⃣ Firms raise prices thru higher markups to manage excess demand & maintain precautionary capacity

November 27, 2024 at 7:15 PM

After expansionary monetary policy shocks, our model predicts 2 novel outcomes:

1️⃣ Firms have higher productivity due to higher worker effort and utilizing idle capacity

2️⃣ Firms raise prices thru higher markups to manage excess demand & maintain precautionary capacity

1️⃣ Firms have higher productivity due to higher worker effort and utilizing idle capacity

2️⃣ Firms raise prices thru higher markups to manage excess demand & maintain precautionary capacity

What we do: introduce capacity utilization in standard NK model

Firms set capacity before observing variable demand → optimal to hold some "precautionary" capacity

When demand manifests, firms produce by utilizing capacity (ala labor effort in Burnside 93)-*upto max capacity*!

Firms set capacity before observing variable demand → optimal to hold some "precautionary" capacity

When demand manifests, firms produce by utilizing capacity (ala labor effort in Burnside 93)-*upto max capacity*!

November 27, 2024 at 7:15 PM

What we do: introduce capacity utilization in standard NK model

Firms set capacity before observing variable demand → optimal to hold some "precautionary" capacity

When demand manifests, firms produce by utilizing capacity (ala labor effort in Burnside 93)-*upto max capacity*!

Firms set capacity before observing variable demand → optimal to hold some "precautionary" capacity

When demand manifests, firms produce by utilizing capacity (ala labor effort in Burnside 93)-*upto max capacity*!

Background evidence:

1️⃣ Typical inflation response to shocks is sluggish & hump-shaped. But sometimes (eg post-Covid) inflation rises sharply

2️⃣ After MP shocks markups⬆️ when GDP⬆️ ("procyclical"), but New Keynesian (NK) models predict opposite

This paper: reconciling 👆

1️⃣ Typical inflation response to shocks is sluggish & hump-shaped. But sometimes (eg post-Covid) inflation rises sharply

2️⃣ After MP shocks markups⬆️ when GDP⬆️ ("procyclical"), but New Keynesian (NK) models predict opposite

This paper: reconciling 👆

November 27, 2024 at 7:15 PM

Background evidence:

1️⃣ Typical inflation response to shocks is sluggish & hump-shaped. But sometimes (eg post-Covid) inflation rises sharply

2️⃣ After MP shocks markups⬆️ when GDP⬆️ ("procyclical"), but New Keynesian (NK) models predict opposite

This paper: reconciling 👆

1️⃣ Typical inflation response to shocks is sluggish & hump-shaped. But sometimes (eg post-Covid) inflation rises sharply

2️⃣ After MP shocks markups⬆️ when GDP⬆️ ("procyclical"), but New Keynesian (NK) models predict opposite

This paper: reconciling 👆

TLDR: Firms want to hold precautionary capacity

After demand (~mon policy) shocks, when demand ⬆️

• if high slack: idle capacity ⬇️ → firm productivity ⬆️ → slow inflation

• if low slack: precautionary capacity ⬇️ → markups ⬆️ (to manage excess demand) → sharp inflation

After demand (~mon policy) shocks, when demand ⬆️

• if high slack: idle capacity ⬇️ → firm productivity ⬆️ → slow inflation

• if low slack: precautionary capacity ⬇️ → markups ⬆️ (to manage excess demand) → sharp inflation

November 27, 2024 at 7:15 PM

TLDR: Firms want to hold precautionary capacity

After demand (~mon policy) shocks, when demand ⬆️

• if high slack: idle capacity ⬇️ → firm productivity ⬆️ → slow inflation

• if low slack: precautionary capacity ⬇️ → markups ⬆️ (to manage excess demand) → sharp inflation

After demand (~mon policy) shocks, when demand ⬆️

• if high slack: idle capacity ⬇️ → firm productivity ⬆️ → slow inflation

• if low slack: precautionary capacity ⬇️ → markups ⬆️ (to manage excess demand) → sharp inflation