Sylvain Catherine

@sylvain-catherine.bsky.social

Finance professor at Wharton

6️⃣This decline in research productivity explains most of the 📉 in growth and 📈in market value.

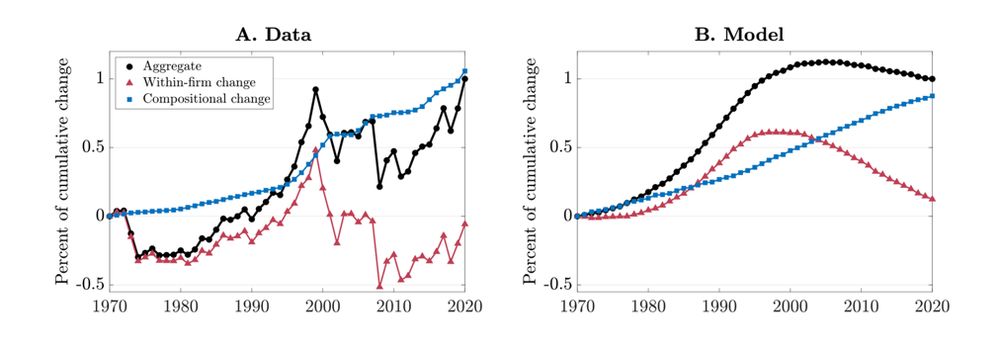

As in the data, all of the market boom comes from a reallocation to high-valuation firms.

Why? High-valuation firms shift from R&D to M&A, concentrating production in their hands

As in the data, all of the market boom comes from a reallocation to high-valuation firms.

Why? High-valuation firms shift from R&D to M&A, concentrating production in their hands

December 2, 2024 at 1:43 PM

6️⃣This decline in research productivity explains most of the 📉 in growth and 📈in market value.

As in the data, all of the market boom comes from a reallocation to high-valuation firms.

Why? High-valuation firms shift from R&D to M&A, concentrating production in their hands

As in the data, all of the market boom comes from a reallocation to high-valuation firms.

Why? High-valuation firms shift from R&D to M&A, concentrating production in their hands

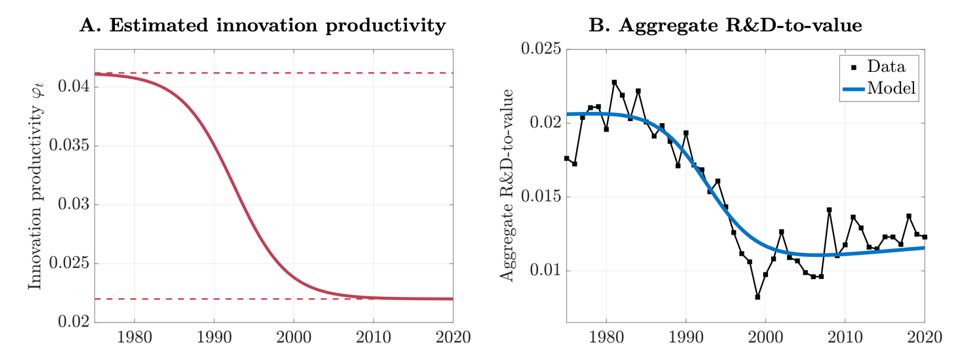

5️⃣He estimates that the decline in R&D-to-value implies that research productivity fell by ~50% since 1975.

In other words, it is half as easy to come up with a new idea today as it was 50 years ago.

In other words, it is half as easy to come up with a new idea today as it was 50 years ago.

December 2, 2024 at 1:43 PM

5️⃣He estimates that the decline in R&D-to-value implies that research productivity fell by ~50% since 1975.

In other words, it is half as easy to come up with a new idea today as it was 50 years ago.

In other words, it is half as easy to come up with a new idea today as it was 50 years ago.

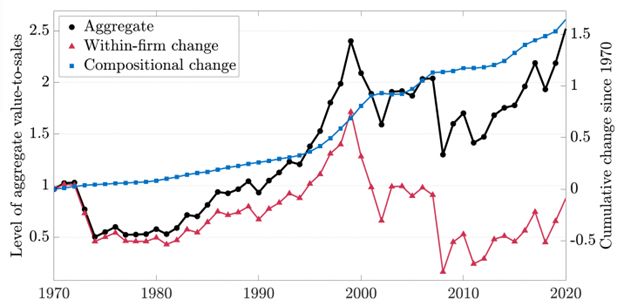

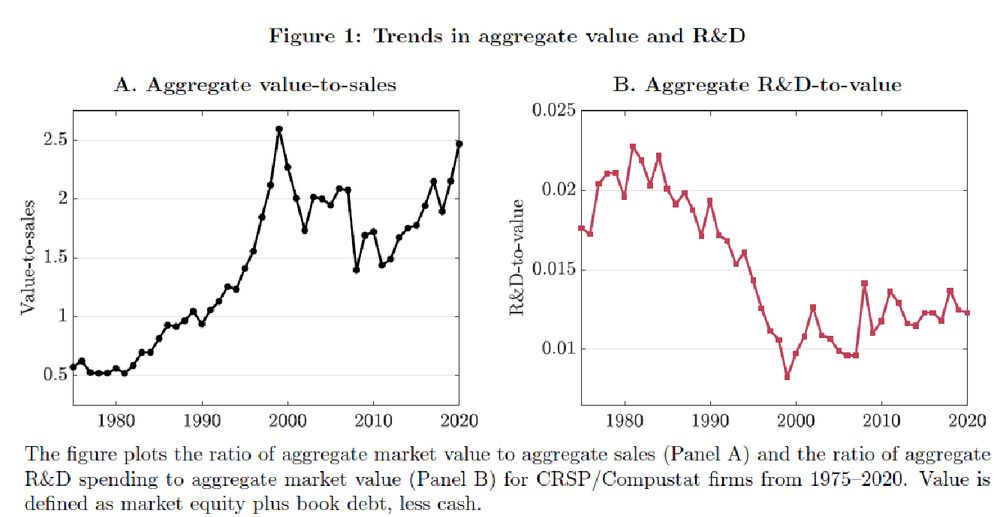

3️⃣ He documents 3 key stylized facts about 1970–2020:

– Aggregate R&D fell relative to value

– Aggregate M&A doubled relative to R&D

– A compositional change explains the rise in aggregate valuation ratios: markets are more and more dominated by firms high valuation ratios

– Aggregate R&D fell relative to value

– Aggregate M&A doubled relative to R&D

– A compositional change explains the rise in aggregate valuation ratios: markets are more and more dominated by firms high valuation ratios

December 2, 2024 at 1:41 PM

3️⃣ He documents 3 key stylized facts about 1970–2020:

– Aggregate R&D fell relative to value

– Aggregate M&A doubled relative to R&D

– A compositional change explains the rise in aggregate valuation ratios: markets are more and more dominated by firms high valuation ratios

– Aggregate R&D fell relative to value

– Aggregate M&A doubled relative to R&D

– A compositional change explains the rise in aggregate valuation ratios: markets are more and more dominated by firms high valuation ratios

2️⃣ The rising market valuation of profits since 1970 should have encouraged firms to innovate, but R&D investment fell.

🧩How do we reconcile stagnating growth (and R&D) with a booming stock market?

James solves this puzzle using micro data and a Schumpeterian growth model.

🧩How do we reconcile stagnating growth (and R&D) with a booming stock market?

James solves this puzzle using micro data and a Schumpeterian growth model.

December 2, 2024 at 1:41 PM

2️⃣ The rising market valuation of profits since 1970 should have encouraged firms to innovate, but R&D investment fell.

🧩How do we reconcile stagnating growth (and R&D) with a booming stock market?

James solves this puzzle using micro data and a Schumpeterian growth model.

🧩How do we reconcile stagnating growth (and R&D) with a booming stock market?

James solves this puzzle using micro data and a Schumpeterian growth model.

🧵My coauthor James Paron is on the market!

His paper reconciles apparently contradictory trends since 1970:

📉declining economic growth

📈rising stock market valuations

His explanation: Innovation got harder➡️ R&D fell, M&A rose ➡️ top firms pushed the aggregate stock market up

His paper reconciles apparently contradictory trends since 1970:

📉declining economic growth

📈rising stock market valuations

His explanation: Innovation got harder➡️ R&D fell, M&A rose ➡️ top firms pushed the aggregate stock market up

December 2, 2024 at 1:40 PM

🧵My coauthor James Paron is on the market!

His paper reconciles apparently contradictory trends since 1970:

📉declining economic growth

📈rising stock market valuations

His explanation: Innovation got harder➡️ R&D fell, M&A rose ➡️ top firms pushed the aggregate stock market up

His paper reconciles apparently contradictory trends since 1970:

📉declining economic growth

📈rising stock market valuations

His explanation: Innovation got harder➡️ R&D fell, M&A rose ➡️ top firms pushed the aggregate stock market up