Simon Toussaint

@simontoussaint.nl

PhD in Economics, Utrecht School of Economics | Dynamics of wealth concentration | Macro + (Public) Finance + Econ History | Cellist and Baritone

www.simontoussaint.nl

www.simontoussaint.nl

Successfully defended my PhD on the wealth distribution! Many thanks to my supervisors, the committee (@basjacobs.bsky.social, @danielwaldenstrom.bsky.social @cmtneztt.bsky.social et al), my paranymphs and all who attended!

My dissertation can be found here: research-portal.uu.nl/en/publicati...

My dissertation can be found here: research-portal.uu.nl/en/publicati...

February 16, 2025 at 3:04 PM

Successfully defended my PhD on the wealth distribution! Many thanks to my supervisors, the committee (@basjacobs.bsky.social, @danielwaldenstrom.bsky.social @cmtneztt.bsky.social et al), my paranymphs and all who attended!

My dissertation can be found here: research-portal.uu.nl/en/publicati...

My dissertation can be found here: research-portal.uu.nl/en/publicati...

Good choice! I am personally even more partial to appelbeignets

November 19, 2024 at 9:24 AM

Good choice! I am personally even more partial to appelbeignets

I'm a @jmwooldridge.bsky.social stan

November 18, 2024 at 8:57 PM

I'm a @jmwooldridge.bsky.social stan

Post a picture you took (no description) to bring some zen to the timeline

November 17, 2024 at 4:42 PM

Post a picture you took (no description) to bring some zen to the timeline

I show that accounting returns are flat or even decreasing in firm size, in contradiction with the theoretical literature.

Happily, my adjusted returns do show a steep & positive gradient, consistent with theory 14/

Happily, my adjusted returns do show a steep & positive gradient, consistent with theory 14/

November 14, 2024 at 5:17 PM

I show that accounting returns are flat or even decreasing in firm size, in contradiction with the theoretical literature.

Happily, my adjusted returns do show a steep & positive gradient, consistent with theory 14/

Happily, my adjusted returns do show a steep & positive gradient, consistent with theory 14/

To recap: aggregate firm wealth is both larger & more stable than book values, and aligns more with underlying economic fundamentals.

Top wealth shares also increase strongly: here are the adjusted top 1% shares. They increase by 3-5 pp on average. Top 0.1% also increase by this amount 12/

Top wealth shares also increase strongly: here are the adjusted top 1% shares. They increase by 3-5 pp on average. Top 0.1% also increase by this amount 12/

November 14, 2024 at 5:17 PM

To recap: aggregate firm wealth is both larger & more stable than book values, and aligns more with underlying economic fundamentals.

Top wealth shares also increase strongly: here are the adjusted top 1% shares. They increase by 3-5 pp on average. Top 0.1% also increase by this amount 12/

Top wealth shares also increase strongly: here are the adjusted top 1% shares. They increase by 3-5 pp on average. Top 0.1% also increase by this amount 12/

Why are yellow and blue so different? Well, There is good reason to believe that book values are fiscally manipulated: after 2013, it became tax-advantageous for firm-owners to reallocate their money towards their firms, which you can see in the plot below

My estimates do not suffer from this 11/

My estimates do not suffer from this 11/

November 14, 2024 at 5:17 PM

Why are yellow and blue so different? Well, There is good reason to believe that book values are fiscally manipulated: after 2013, it became tax-advantageous for firm-owners to reallocate their money towards their firms, which you can see in the plot below

My estimates do not suffer from this 11/

My estimates do not suffer from this 11/

What are the results of all this math? First, aggregate firm wealth increases substantially and is more stable! Yellow = true market value, blue = book value, green = initial estimate, red = capital

We see that my procedure is necessary; simply using an initial estimate (green) is insufficient 10/

We see that my procedure is necessary; simply using an initial estimate (green) is insufficient 10/

November 14, 2024 at 5:17 PM

What are the results of all this math? First, aggregate firm wealth increases substantially and is more stable! Yellow = true market value, blue = book value, green = initial estimate, red = capital

We see that my procedure is necessary; simply using an initial estimate (green) is insufficient 10/

We see that my procedure is necessary; simply using an initial estimate (green) is insufficient 10/

I apply my method to the Netherlands, where I can link the universe of incorporated firms to their owners. Private firms matter a lot for top wealth inequality: they are 80% of the top 0.01%'s portfolio!

8/

8/

November 14, 2024 at 5:17 PM

I apply my method to the Netherlands, where I can link the universe of incorporated firms to their owners. Private firms matter a lot for top wealth inequality: they are 80% of the top 0.01%'s portfolio!

8/

8/

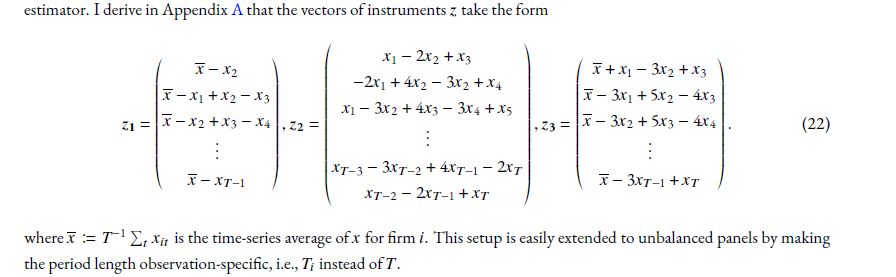

Griliches & Hausman formalize this intuition and I use their framework to derive several valid IVs. Since there is only one endogenous variable (the capital stock), we can test overidentifying restrictions.

Then, fitted values from this IV/GMM regression will be error-free market values 7/

Then, fitted values from this IV/GMM regression will be error-free market values 7/

November 14, 2024 at 5:17 PM

Griliches & Hausman formalize this intuition and I use their framework to derive several valid IVs. Since there is only one endogenous variable (the capital stock), we can test overidentifying restrictions.

Then, fitted values from this IV/GMM regression will be error-free market values 7/

Then, fitted values from this IV/GMM regression will be error-free market values 7/

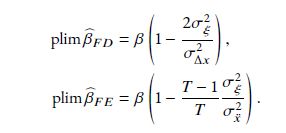

Consider a variable x with measurement error ξ. Compare the first-dif estimator to the fixed-effects estimator, and they will be biased like below

But this is 2 equations in 2 unknowns (β and variance of ξ)! Intuitively, the differences in bias betw the regs gives identifying information 6/

But this is 2 equations in 2 unknowns (β and variance of ξ)! Intuitively, the differences in bias betw the regs gives identifying information 6/

November 14, 2024 at 5:17 PM

Consider a variable x with measurement error ξ. Compare the first-dif estimator to the fixed-effects estimator, and they will be biased like below

But this is 2 equations in 2 unknowns (β and variance of ξ)! Intuitively, the differences in bias betw the regs gives identifying information 6/

But this is 2 equations in 2 unknowns (β and variance of ξ)! Intuitively, the differences in bias betw the regs gives identifying information 6/

What is this regression? Well, in neoclassical investment theory, it is simply the equation for Tobin's q!

But this holds more generally: I show that even when firms have markups and/or decreasing returns to scale, firm value is approx linear in their capital stock

4/

But this holds more generally: I show that even when firms have markups and/or decreasing returns to scale, firm value is approx linear in their capital stock

4/

November 14, 2024 at 5:17 PM

What is this regression? Well, in neoclassical investment theory, it is simply the equation for Tobin's q!

But this holds more generally: I show that even when firms have markups and/or decreasing returns to scale, firm value is approx linear in their capital stock

4/

But this holds more generally: I show that even when firms have markups and/or decreasing returns to scale, firm value is approx linear in their capital stock

4/

📯 Job Market Paper Alert 📯

Private businesses make up 50% of sales & profits and are the main wealth component of the wealthiest households. So, what is their value? Well, that's difficult, since they're not listed: their value is unobservable by definition!

My #EconJMP tackles this problem 1/

Private businesses make up 50% of sales & profits and are the main wealth component of the wealthiest households. So, what is their value? Well, that's difficult, since they're not listed: their value is unobservable by definition!

My #EconJMP tackles this problem 1/

![Robust Estimation of Private Business Wealth*

Job Market Paper

Simon J. Toussaint†

November 14, 2024

[Most recent version here]

Abstract

Estimating the market value of private businesses is essential for understanding both aggregate firm dynamics and top wealth

inequality, yet these values are inherently unobservable. This paper introduces an econometric approach that treats the gap

between true market values and initial estimates as measurement error. I employ time-series restrictions on these errors as

moment conditions within a GMM framework, and use the fitted values from these estimations as error-free estimates of

private business wealth and capital stocks. Applying this method to Dutch administrative data linking the universe of firms

to their owners, I find that aggregate private business wealth increases by 30% of GDP initially, and is more stable than the

unadjusted series. Top 1% and 0.1% wealth shares increase by 3–5 percentage points, peaking at 38% and 20%, respectively.

Adjusted returns to firm wealth exhibit a steeper gradient across the wealth distribution than unadjusted returns, consistent

with models of return heterogeneity.](https://cdn.bsky.app/img/feed_thumbnail/plain/did:plc:wus4g34bpbzjefp547irpkeu/bafkreibg34g2k7zwmjqytkllrcxfsj5tnov22hdny74qz7ks5jwa5csbou@jpeg)

November 14, 2024 at 5:17 PM

📯 Job Market Paper Alert 📯

Private businesses make up 50% of sales & profits and are the main wealth component of the wealthiest households. So, what is their value? Well, that's difficult, since they're not listed: their value is unobservable by definition!

My #EconJMP tackles this problem 1/

Private businesses make up 50% of sales & profits and are the main wealth component of the wealthiest households. So, what is their value? Well, that's difficult, since they're not listed: their value is unobservable by definition!

My #EconJMP tackles this problem 1/

Took me a while to make the jump

November 7, 2024 at 4:49 PM

Took me a while to make the jump

Happy to be in Stockholm, presenting my paper "Robust Estimation of Private Business Wealth" tomorrow at the IFN! #EconSky

Very special to catch a Yo-Yo Ma concert this evening, finally seeing him live!

Very special to catch a Yo-Yo Ma concert this evening, finally seeing him live!

November 3, 2024 at 8:30 PM

Happy to be in Stockholm, presenting my paper "Robust Estimation of Private Business Wealth" tomorrow at the IFN! #EconSky

Very special to catch a Yo-Yo Ma concert this evening, finally seeing him live!

Very special to catch a Yo-Yo Ma concert this evening, finally seeing him live!

Happy to be in Paris to present my paper "Top Wealth is Distributed Weibull, not Pareto" at the Paris School of Economics!

March 21, 2024 at 8:27 AM

Happy to be in Paris to present my paper "Top Wealth is Distributed Weibull, not Pareto" at the Paris School of Economics!

What are implications for models that use Pareto? One major one is for optimal tax. The Diamond-Saez formula for the optimal top tax rate converges to a constant with Pareto income. With Weibull, that is no longer so (at least if the behavioral elasticity stays constant) 8/

November 23, 2023 at 12:40 PM

What are implications for models that use Pareto? One major one is for optimal tax. The Diamond-Saez formula for the optimal top tax rate converges to a constant with Pareto income. With Weibull, that is no longer so (at least if the behavioral elasticity stays constant) 8/

How can we microfound Gompertz/Weibull? One possibility we like is that on stochastic networks, the length distribution of *Self-Avoiding-Walks* is Gompertz. These are paths that do not visit a node twice, like the game Snake.

How to use this? E.g. City size must be bounded by area already used 7/

How to use this? E.g. City size must be bounded by area already used 7/

November 23, 2023 at 12:39 PM

How can we microfound Gompertz/Weibull? One possibility we like is that on stochastic networks, the length distribution of *Self-Avoiding-Walks* is Gompertz. These are paths that do not visit a node twice, like the game Snake.

How to use this? E.g. City size must be bounded by area already used 7/

How to use this? E.g. City size must be bounded by area already used 7/

Weibull is much more convenient than Pareto because all its moments exist. We can use it to predict mean billionaire wealth for different regions.

The table shows 1) Weibull does extremely well; 2) Pareto fails miserably, with infinite and nonsensically large values in majority of cases 6/

The table shows 1) Weibull does extremely well; 2) Pareto fails miserably, with infinite and nonsensically large values in majority of cases 6/

November 23, 2023 at 12:34 PM

Weibull is much more convenient than Pareto because all its moments exist. We can use it to predict mean billionaire wealth for different regions.

The table shows 1) Weibull does extremely well; 2) Pareto fails miserably, with infinite and nonsensically large values in majority of cases 6/

The table shows 1) Weibull does extremely well; 2) Pareto fails miserably, with infinite and nonsensically large values in majority of cases 6/

Our alternative is (truncated-)Weibull. If W is Weibull, log W is Gompertz. This distribution has an exponentially increasing (cumulative) hazard. If W is Pareto, in contrast, log W has a linear (cumulative) hazard. Judge for yourself below, data for wealth. 5/

November 23, 2023 at 12:32 PM

Our alternative is (truncated-)Weibull. If W is Weibull, log W is Gompertz. This distribution has an exponentially increasing (cumulative) hazard. If W is Pareto, in contrast, log W has a linear (cumulative) hazard. Judge for yourself below, data for wealth. 5/

E[w^k] = k! * α^k; hence, E[w] = α. Substitute back and rescale to obtain our test statistic R_k = E[w^k]/k!*E[w]^k.

R_k should equal 1 if W is Pareto; this is our (sharp) test. See the values of R_2 and R_3 for firm size below: Clearly not equal to 1 (same for wealth & city size).

3/

R_k should equal 1 if W is Pareto; this is our (sharp) test. See the values of R_2 and R_3 for firm size below: Clearly not equal to 1 (same for wealth & city size).

3/

November 23, 2023 at 12:28 PM

E[w^k] = k! * α^k; hence, E[w] = α. Substitute back and rescale to obtain our test statistic R_k = E[w^k]/k!*E[w]^k.

R_k should equal 1 if W is Pareto; this is our (sharp) test. See the values of R_2 and R_3 for firm size below: Clearly not equal to 1 (same for wealth & city size).

3/

R_k should equal 1 if W is Pareto; this is our (sharp) test. See the values of R_2 and R_3 for firm size below: Clearly not equal to 1 (same for wealth & city size).

3/

Hello #EconSky, have I got an exciting new working paper for you!

Coen Teulings and I study three distributions (wealth, city and firm size), which are always thought to be distributed Pareto.

Bottom line: These distributions are *not* Pareto, but Weibull! A thread 1/

Coen Teulings and I study three distributions (wealth, city and firm size), which are always thought to be distributed Pareto.

Bottom line: These distributions are *not* Pareto, but Weibull! A thread 1/

November 23, 2023 at 12:20 PM

Hello #EconSky, have I got an exciting new working paper for you!

Coen Teulings and I study three distributions (wealth, city and firm size), which are always thought to be distributed Pareto.

Bottom line: These distributions are *not* Pareto, but Weibull! A thread 1/

Coen Teulings and I study three distributions (wealth, city and firm size), which are always thought to be distributed Pareto.

Bottom line: These distributions are *not* Pareto, but Weibull! A thread 1/