Ryan Swift

@ryanswiftbca.bsky.social

Managing Editor of US Bond Strategy at BCA Research

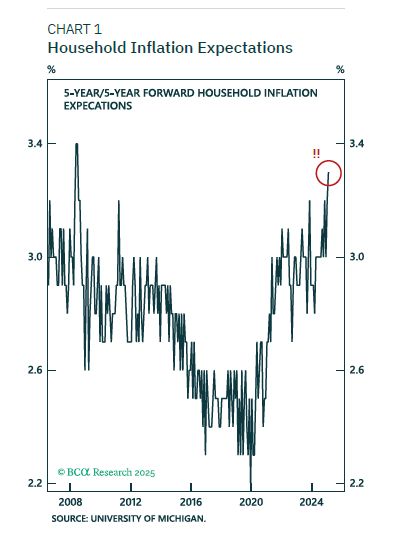

Stock investors shouldn't expect any near-term relief from the Fed. With long-dated inflation expectations the highest since 1993, the Fed simply can't risk easing policy as tariffs cause inflation to come in hot. We'll eventually get rate cuts, but not until the labor market cracks.

April 4, 2025 at 5:08 PM

Stock investors shouldn't expect any near-term relief from the Fed. With long-dated inflation expectations the highest since 1993, the Fed simply can't risk easing policy as tariffs cause inflation to come in hot. We'll eventually get rate cuts, but not until the labor market cracks.

Recession Watch Update:

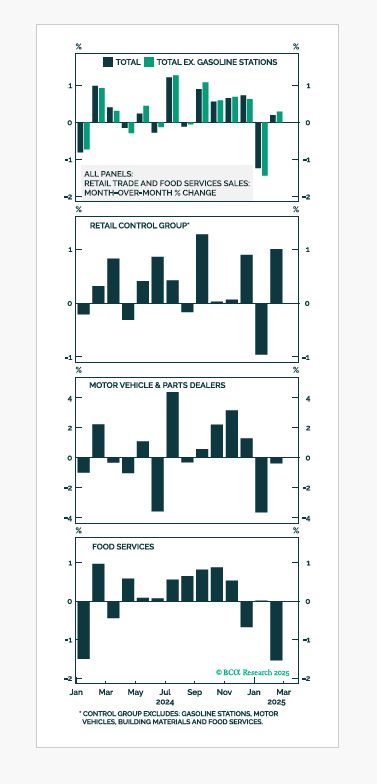

Still just February data, but all indications are that the US consumer is struggling. And this is before we even see an impact from tariffs. We'll get our first look at March data next week with vehicle sales on Tuesday and Payrolls on Friday.

Still just February data, but all indications are that the US consumer is struggling. And this is before we even see an impact from tariffs. We'll get our first look at March data next week with vehicle sales on Tuesday and Payrolls on Friday.

March 28, 2025 at 5:36 PM

Recession Watch Update:

Still just February data, but all indications are that the US consumer is struggling. And this is before we even see an impact from tariffs. We'll get our first look at March data next week with vehicle sales on Tuesday and Payrolls on Friday.

Still just February data, but all indications are that the US consumer is struggling. And this is before we even see an impact from tariffs. We'll get our first look at March data next week with vehicle sales on Tuesday and Payrolls on Friday.

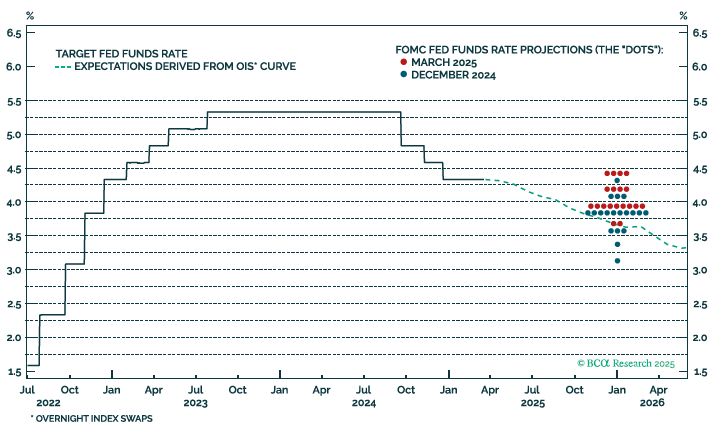

The market reaction to yesterday's Fed meeting looks overdone. Investors could be in for a hawkish surprise when it becomes apparent that the Fed won’t ease policy into higher tariff-driven inflation prints.

March 20, 2025 at 12:04 PM

The market reaction to yesterday's Fed meeting looks overdone. Investors could be in for a hawkish surprise when it becomes apparent that the Fed won’t ease policy into higher tariff-driven inflation prints.

Atlanta Fed's GDPNow tracker didn't like the retail sales print. Some upward pressure on goods spending from the control group was more than offset by very weak Food Services spending on the services side.

March 17, 2025 at 5:41 PM

Atlanta Fed's GDPNow tracker didn't like the retail sales print. Some upward pressure on goods spending from the control group was more than offset by very weak Food Services spending on the services side.

Not much bounceback in February retail sales from a very weak January. The control group that feeds into GDP was strong, but weak auto sales and restaurant spending are a cause for concern. The US consumer looks fragile, and recession risk remains high.

March 17, 2025 at 2:05 PM

Not much bounceback in February retail sales from a very weak January. The control group that feeds into GDP was strong, but weak auto sales and restaurant spending are a cause for concern. The US consumer looks fragile, and recession risk remains high.

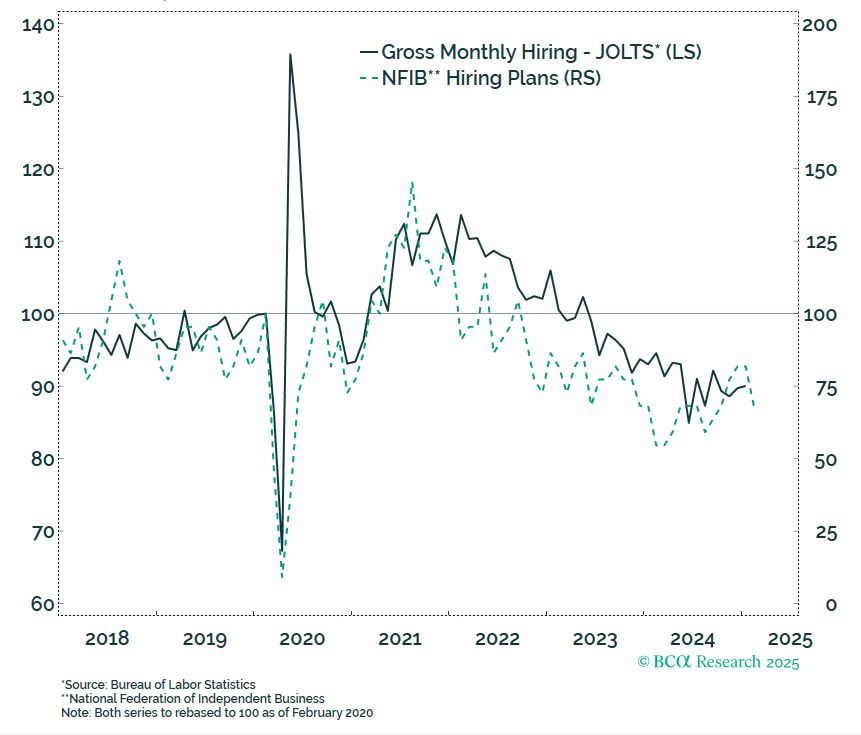

We're on recession watch here at #bcaresearch, looking for signs that rising tariffs and consumer weakness are leading to cracks in the US labor market. Not much evidence of this in the data so far as hiring has been roughly flat for the past few months (note that JOLTS data only go to January).

March 11, 2025 at 3:28 PM

We're on recession watch here at #bcaresearch, looking for signs that rising tariffs and consumer weakness are leading to cracks in the US labor market. Not much evidence of this in the data so far as hiring has been roughly flat for the past few months (note that JOLTS data only go to January).

Solid employment growth for February at +151k, but I suspect that will be the high point for a while. Job growth was flattered by +34k from Goods-Producing sectors (well above last year's average of +6k) and the DOGE firings have only just started to hit the Government sector.

March 7, 2025 at 6:26 PM

Solid employment growth for February at +151k, but I suspect that will be the high point for a while. Job growth was flattered by +34k from Goods-Producing sectors (well above last year's average of +6k) and the DOGE firings have only just started to hit the Government sector.

The bond market is now priced for almost 80 bps of Fed easing over the next 12 months, but 1-year inflation expectations are elevated due to tariff risk (just under 3%). This is an awkward position for the Fed. I expect they'll be reluctant to cut rates into any tariff-induced price shock.

February 28, 2025 at 5:55 PM

The bond market is now priced for almost 80 bps of Fed easing over the next 12 months, but 1-year inflation expectations are elevated due to tariff risk (just under 3%). This is an awkward position for the Fed. I expect they'll be reluctant to cut rates into any tariff-induced price shock.

Fed Governor Chris Waller gave a speech this week in which he said he favors "looking through" the price effects of tariffs when setting monetary policy.

With inflation expectations as high as they are, I'm skeptical about the idea that the Fed will be cutting rates as tariffs cause CPI to jump.

With inflation expectations as high as they are, I'm skeptical about the idea that the Fed will be cutting rates as tariffs cause CPI to jump.

February 19, 2025 at 5:18 PM

Fed Governor Chris Waller gave a speech this week in which he said he favors "looking through" the price effects of tariffs when setting monetary policy.

With inflation expectations as high as they are, I'm skeptical about the idea that the Fed will be cutting rates as tariffs cause CPI to jump.

With inflation expectations as high as they are, I'm skeptical about the idea that the Fed will be cutting rates as tariffs cause CPI to jump.

I'll be looking for two things in Jay Powell's testimony this week:

1) Does he give further insight into how the Fed is thinking about the economic impact of tariffs.

2) Does he shift forward guidance goalposts away from needing to see progress on inflation to needing to see labor market weakness.

1) Does he give further insight into how the Fed is thinking about the economic impact of tariffs.

2) Does he shift forward guidance goalposts away from needing to see progress on inflation to needing to see labor market weakness.

February 11, 2025 at 3:39 PM

I'll be looking for two things in Jay Powell's testimony this week:

1) Does he give further insight into how the Fed is thinking about the economic impact of tariffs.

2) Does he shift forward guidance goalposts away from needing to see progress on inflation to needing to see labor market weakness.

1) Does he give further insight into how the Fed is thinking about the economic impact of tariffs.

2) Does he shift forward guidance goalposts away from needing to see progress on inflation to needing to see labor market weakness.

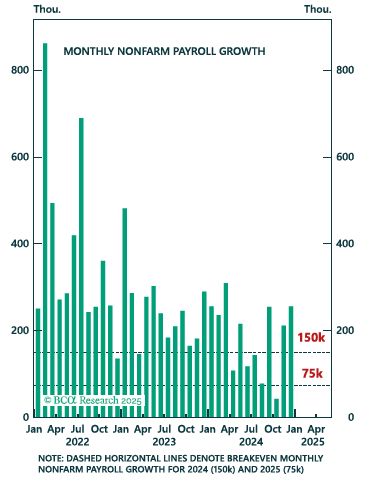

NFP +144k in January, lower than last year's average. But with slower labor force growth in 2025 than 2024, it's still enough to put downward pressure on the unemployment rate. We estimate +75k jobs per month needed to keep the unemployment rate stable this year, compared to 150k last year.

February 7, 2025 at 2:13 PM

NFP +144k in January, lower than last year's average. But with slower labor force growth in 2025 than 2024, it's still enough to put downward pressure on the unemployment rate. We estimate +75k jobs per month needed to keep the unemployment rate stable this year, compared to 150k last year.

For this Friday's NFP the critical number is 75k. Payroll growth > 75k is consistent with a falling unemployment rate. We estimate this breakeven threshold as about half what it was last year, due to much slower expected labor force growth.

February 5, 2025 at 6:28 PM

For this Friday's NFP the critical number is 75k. Payroll growth > 75k is consistent with a falling unemployment rate. We estimate this breakeven threshold as about half what it was last year, due to much slower expected labor force growth.