Nate

@nategrowswealth.bsky.social

👨👧👦 Dad building wealth for his family

📈 Finance | Personal Growth

Simplifying the complexities of finance, and building wealth.

https://linktr.ee/nategrowswealth

📈 Finance | Personal Growth

Simplifying the complexities of finance, and building wealth.

https://linktr.ee/nategrowswealth

How to retire early on $60k salary?

Here's the path:

1. Save 30% of your salary = $18,000/year

2. Invest it in low cost index funds

3. Let it compound over 25 years

4. You will now have ~$1.5M in your portfolio

You don't need a raise — just a strategy.

Here's the path:

1. Save 30% of your salary = $18,000/year

2. Invest it in low cost index funds

3. Let it compound over 25 years

4. You will now have ~$1.5M in your portfolio

You don't need a raise — just a strategy.

June 18, 2025 at 6:31 PM

How to retire early on $60k salary?

Here's the path:

1. Save 30% of your salary = $18,000/year

2. Invest it in low cost index funds

3. Let it compound over 25 years

4. You will now have ~$1.5M in your portfolio

You don't need a raise — just a strategy.

Here's the path:

1. Save 30% of your salary = $18,000/year

2. Invest it in low cost index funds

3. Let it compound over 25 years

4. You will now have ~$1.5M in your portfolio

You don't need a raise — just a strategy.

What if you invested $500/month for 20 years?

In a total market index fund this is what you would return:

• At 6% return: ~ $233K

• At 8% return: ~ $296K

• At 10% return: ~ $378K

The 🔑 is consistency, not timing the market..

#InvestingMadeSimple #CompoundGrowth #FIREMovement

In a total market index fund this is what you would return:

• At 6% return: ~ $233K

• At 8% return: ~ $296K

• At 10% return: ~ $378K

The 🔑 is consistency, not timing the market..

#InvestingMadeSimple #CompoundGrowth #FIREMovement

June 17, 2025 at 1:30 AM

What if you invested $500/month for 20 years?

In a total market index fund this is what you would return:

• At 6% return: ~ $233K

• At 8% return: ~ $296K

• At 10% return: ~ $378K

The 🔑 is consistency, not timing the market..

#InvestingMadeSimple #CompoundGrowth #FIREMovement

In a total market index fund this is what you would return:

• At 6% return: ~ $233K

• At 8% return: ~ $296K

• At 10% return: ~ $378K

The 🔑 is consistency, not timing the market..

#InvestingMadeSimple #CompoundGrowth #FIREMovement

Step 5 Continued

What if we got crazy and picked up a side hustle which allowed us to contribute $1k a month

Now we're cooking with gas 🔥

We would have $2.3M at retirement following the rule of 4% we could withdraw $92,000 a year without impacting this balance.

What if we got crazy and picked up a side hustle which allowed us to contribute $1k a month

Now we're cooking with gas 🔥

We would have $2.3M at retirement following the rule of 4% we could withdraw $92,000 a year without impacting this balance.

May 14, 2025 at 7:01 PM

Step 5 Continued

What if we got crazy and picked up a side hustle which allowed us to contribute $1k a month

Now we're cooking with gas 🔥

We would have $2.3M at retirement following the rule of 4% we could withdraw $92,000 a year without impacting this balance.

What if we got crazy and picked up a side hustle which allowed us to contribute $1k a month

Now we're cooking with gas 🔥

We would have $2.3M at retirement following the rule of 4% we could withdraw $92,000 a year without impacting this balance.

Step 5: Get to the number you want

Lets say we have some wiggle room and we can contribute $750/ month. So simply go back to the calculator and change teh contributions.

After we do that we have ..... $1.8M at retirement and now we see that we will have what we need for retirement.

But what if..

Lets say we have some wiggle room and we can contribute $750/ month. So simply go back to the calculator and change teh contributions.

After we do that we have ..... $1.8M at retirement and now we see that we will have what we need for retirement.

But what if..

May 14, 2025 at 7:01 PM

Step 5: Get to the number you want

Lets say we have some wiggle room and we can contribute $750/ month. So simply go back to the calculator and change teh contributions.

After we do that we have ..... $1.8M at retirement and now we see that we will have what we need for retirement.

But what if..

Lets say we have some wiggle room and we can contribute $750/ month. So simply go back to the calculator and change teh contributions.

After we do that we have ..... $1.8M at retirement and now we see that we will have what we need for retirement.

But what if..

Step 4: Observe your forecasted retirement balance.

Based on the information I entered this individual will have $1.3M when they retire.

You can then apply the rule of 4% and estimate your annual retirement income which would be $1.3M *0.04 = $52,000 /year

Don't like the number? lets tweak it!

Based on the information I entered this individual will have $1.3M when they retire.

You can then apply the rule of 4% and estimate your annual retirement income which would be $1.3M *0.04 = $52,000 /year

Don't like the number? lets tweak it!

May 14, 2025 at 7:01 PM

Step 4: Observe your forecasted retirement balance.

Based on the information I entered this individual will have $1.3M when they retire.

You can then apply the rule of 4% and estimate your annual retirement income which would be $1.3M *0.04 = $52,000 /year

Don't like the number? lets tweak it!

Based on the information I entered this individual will have $1.3M when they retire.

You can then apply the rule of 4% and estimate your annual retirement income which would be $1.3M *0.04 = $52,000 /year

Don't like the number? lets tweak it!

Step 3: Follow me to this website: https://www.nerdwallet.com/calculator/retirement-calculator shoutout @nerdwallet

Once you arrive enter in your information like this:

Once you arrive enter in your information like this:

May 14, 2025 at 7:01 PM

Step 3: Follow me to this website: https://www.nerdwallet.com/calculator/retirement-calculator shoutout @nerdwallet

Once you arrive enter in your information like this:

Once you arrive enter in your information like this:

Step 5 Continued

What if we got crazy and picked up a side hustle which allowed us to contribute $1k a month

Now we're cooking with gas 🔥

We would have $2.3M at retirement following the rule of 4% we could withdraw $92,000 a year without impacting this balance.

What if we got crazy and picked up a side hustle which allowed us to contribute $1k a month

Now we're cooking with gas 🔥

We would have $2.3M at retirement following the rule of 4% we could withdraw $92,000 a year without impacting this balance.

May 10, 2025 at 1:02 AM

Step 5 Continued

What if we got crazy and picked up a side hustle which allowed us to contribute $1k a month

Now we're cooking with gas 🔥

We would have $2.3M at retirement following the rule of 4% we could withdraw $92,000 a year without impacting this balance.

What if we got crazy and picked up a side hustle which allowed us to contribute $1k a month

Now we're cooking with gas 🔥

We would have $2.3M at retirement following the rule of 4% we could withdraw $92,000 a year without impacting this balance.

Step 5: Get to the number you want

Lets say we have some wiggle room and we can contribute $750/ month. So simply go back to the calculator and change teh contributions.

After we do that we have ..... $1.8M at retirement and now we see that we will have what we need for retirement.

But what if..

Lets say we have some wiggle room and we can contribute $750/ month. So simply go back to the calculator and change teh contributions.

After we do that we have ..... $1.8M at retirement and now we see that we will have what we need for retirement.

But what if..

May 10, 2025 at 1:02 AM

Step 5: Get to the number you want

Lets say we have some wiggle room and we can contribute $750/ month. So simply go back to the calculator and change teh contributions.

After we do that we have ..... $1.8M at retirement and now we see that we will have what we need for retirement.

But what if..

Lets say we have some wiggle room and we can contribute $750/ month. So simply go back to the calculator and change teh contributions.

After we do that we have ..... $1.8M at retirement and now we see that we will have what we need for retirement.

But what if..

Step 4: Observe your forecasted retirement balance.

Based ont he information I entered this individual will ahve $1.3M when they retire.

You can then apply the rule of 4% and estimate your annual retirement income which would be $1.3M *0.04 = $52,000 / year

Don't like the number? lets tweak it!

Based ont he information I entered this individual will ahve $1.3M when they retire.

You can then apply the rule of 4% and estimate your annual retirement income which would be $1.3M *0.04 = $52,000 / year

Don't like the number? lets tweak it!

May 10, 2025 at 1:02 AM

Step 4: Observe your forecasted retirement balance.

Based ont he information I entered this individual will ahve $1.3M when they retire.

You can then apply the rule of 4% and estimate your annual retirement income which would be $1.3M *0.04 = $52,000 / year

Don't like the number? lets tweak it!

Based ont he information I entered this individual will ahve $1.3M when they retire.

You can then apply the rule of 4% and estimate your annual retirement income which would be $1.3M *0.04 = $52,000 / year

Don't like the number? lets tweak it!

Step 3: Follow me to this website: https://www.nerdwallet.com/calculator/retirement-calculator shoutout @nerdwallet

Once you arrive enter in your information like this:

Once you arrive enter in your information like this:

May 10, 2025 at 1:02 AM

Step 3: Follow me to this website: https://www.nerdwallet.com/calculator/retirement-calculator shoutout @nerdwallet

Once you arrive enter in your information like this:

Once you arrive enter in your information like this:

Uh oh….

I better pay for those unpaid tolls…

The state I live in has no tolls and never has 🤔

Be careful out there scammy texts have been up lately for me!

I better pay for those unpaid tolls…

The state I live in has no tolls and never has 🤔

Be careful out there scammy texts have been up lately for me!

May 7, 2025 at 9:10 PM

Uh oh….

I better pay for those unpaid tolls…

The state I live in has no tolls and never has 🤔

Be careful out there scammy texts have been up lately for me!

I better pay for those unpaid tolls…

The state I live in has no tolls and never has 🤔

Be careful out there scammy texts have been up lately for me!

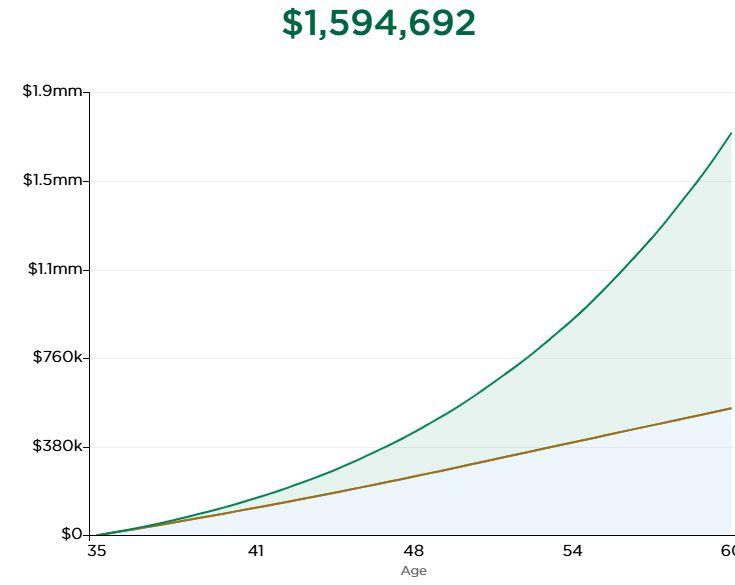

If Adam contributes 20% of his paycheck every year for 40 years, he will have the following:

Total Contributed: $811,682

Total Return: $2,978,239

Total for Retirement: $3,789,922

Total Contributed: $811,682

Total Return: $2,978,239

Total for Retirement: $3,789,922

May 6, 2025 at 9:31 PM

If Adam contributes 20% of his paycheck every year for 40 years, he will have the following:

Total Contributed: $811,682

Total Return: $2,978,239

Total for Retirement: $3,789,922

Total Contributed: $811,682

Total Return: $2,978,239

Total for Retirement: $3,789,922

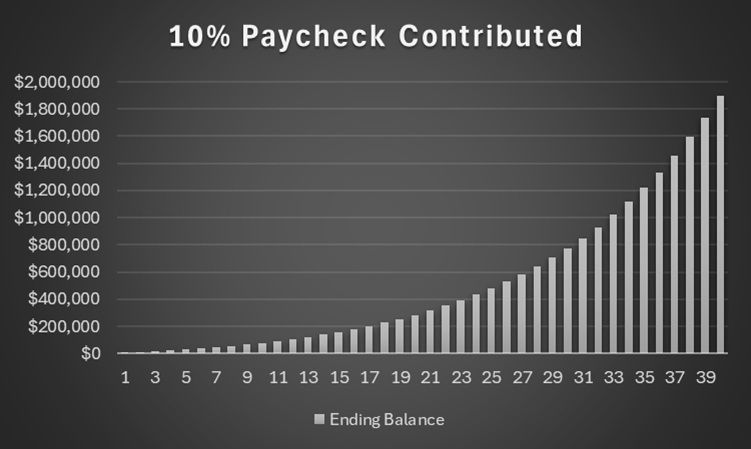

If Adam contributes 10% of his paycheck every year for 40 years, he will have the following:

Total Contributed: $401,041

Total Return: $1,493,919

Total for Retirement: $1,894,961

That's double what we saw previously, But would increasing this to 20% of his income make a big difference?

Total Contributed: $401,041

Total Return: $1,493,919

Total for Retirement: $1,894,961

That's double what we saw previously, But would increasing this to 20% of his income make a big difference?

May 6, 2025 at 9:31 PM

If Adam contributes 10% of his paycheck every year for 40 years, he will have the following:

Total Contributed: $401,041

Total Return: $1,493,919

Total for Retirement: $1,894,961

That's double what we saw previously, But would increasing this to 20% of his income make a big difference?

Total Contributed: $401,041

Total Return: $1,493,919

Total for Retirement: $1,894,961

That's double what we saw previously, But would increasing this to 20% of his income make a big difference?

If Adam contributes 5% of his paycheck every year for 40 years, he will have the following:

Total Contributed: $202,920

Total Return: $744,759

Total for Retirement: $947,480

Now, let's see what the payoff would be if he increased this to 10% of his income

Total Contributed: $202,920

Total Return: $744,759

Total for Retirement: $947,480

Now, let's see what the payoff would be if he increased this to 10% of his income

May 6, 2025 at 9:31 PM

If Adam contributes 5% of his paycheck every year for 40 years, he will have the following:

Total Contributed: $202,920

Total Return: $744,759

Total for Retirement: $947,480

Now, let's see what the payoff would be if he increased this to 10% of his income

Total Contributed: $202,920

Total Return: $744,759

Total for Retirement: $947,480

Now, let's see what the payoff would be if he increased this to 10% of his income

Want to unlock true wealth? It all starts with owning the most powerful asset you’ll ever have—yourself.

January 7, 2025 at 8:20 PM

Want to unlock true wealth? It all starts with owning the most powerful asset you’ll ever have—yourself.

Want to build wealth without the stress of stock picking? Discover the proven strategy that beats 90% of Wall Street fund managers—it’s simpler than you think!

January 3, 2025 at 9:59 PM

Want to build wealth without the stress of stock picking? Discover the proven strategy that beats 90% of Wall Street fund managers—it’s simpler than you think!

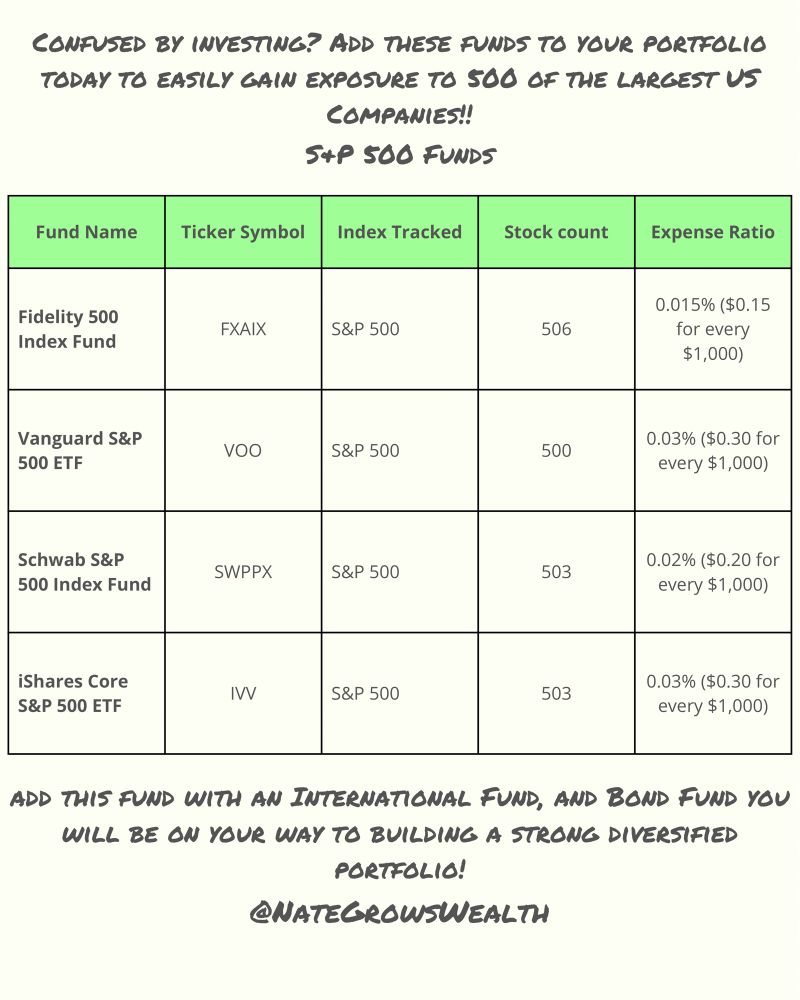

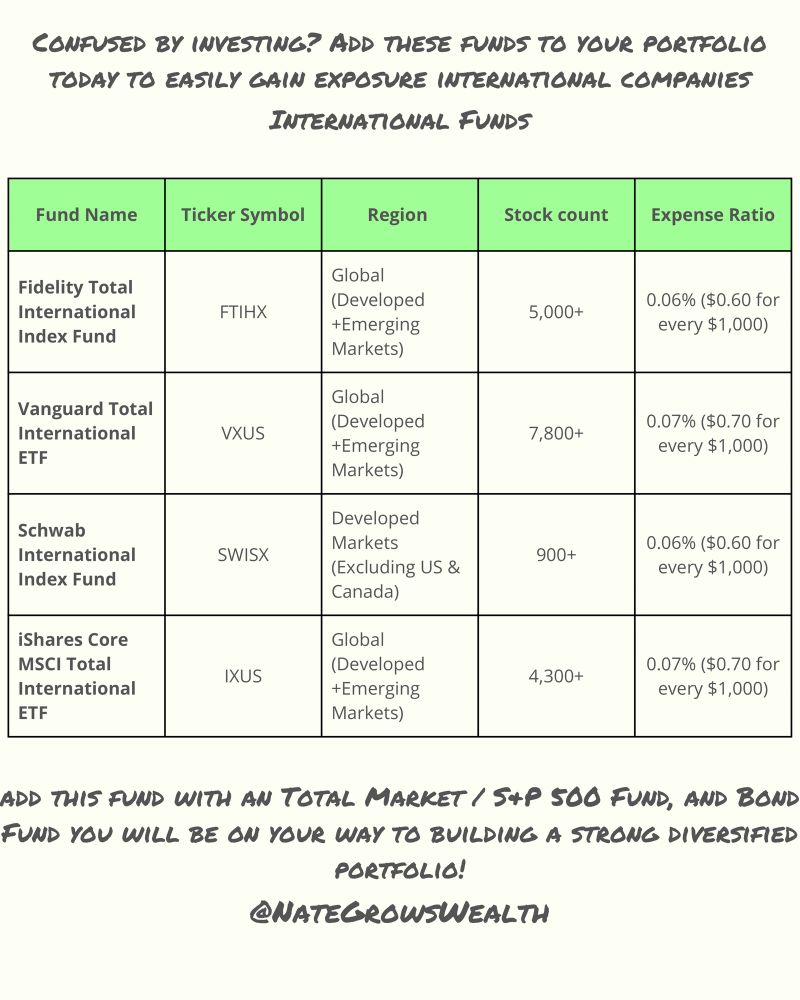

Confused about which index funds to choose for your investment portfolio?

Here’s a simple guide I created to help you decide!

I break down four popular funds for:

- Total Market Index

- S&P 500 Index

- International Index

Here’s a simple guide I created to help you decide!

I break down four popular funds for:

- Total Market Index

- S&P 500 Index

- International Index

January 2, 2025 at 9:44 PM

Confused about which index funds to choose for your investment portfolio?

Here’s a simple guide I created to help you decide!

I break down four popular funds for:

- Total Market Index

- S&P 500 Index

- International Index

Here’s a simple guide I created to help you decide!

I break down four popular funds for:

- Total Market Index

- S&P 500 Index

- International Index

Are you tired of never having money set aside for emergencies? Here’s a shocking fact: 53% of Americans have $500 or less saved.

Good news—saving just $501 puts you ahead of half the country.

Want to build an emergency fund? Start small:

1️⃣ Plan

2️⃣ Math it out

3️⃣ Act

4️⃣ Don’t get discouraged

#Finance

Good news—saving just $501 puts you ahead of half the country.

Want to build an emergency fund? Start small:

1️⃣ Plan

2️⃣ Math it out

3️⃣ Act

4️⃣ Don’t get discouraged

#Finance

December 13, 2024 at 5:25 PM

Are you tired of never having money set aside for emergencies? Here’s a shocking fact: 53% of Americans have $500 or less saved.

Good news—saving just $501 puts you ahead of half the country.

Want to build an emergency fund? Start small:

1️⃣ Plan

2️⃣ Math it out

3️⃣ Act

4️⃣ Don’t get discouraged

#Finance

Good news—saving just $501 puts you ahead of half the country.

Want to build an emergency fund? Start small:

1️⃣ Plan

2️⃣ Math it out

3️⃣ Act

4️⃣ Don’t get discouraged

#Finance

What Should I Invest In?!

I have broken out the guides to show S&P 500, Total Market, and lastly international index funds from the most popular firms.

You can easily automate regular investments into one or two of these funds and be invested in up to 7,800 stocks!

#finance #indexfunds #invest

I have broken out the guides to show S&P 500, Total Market, and lastly international index funds from the most popular firms.

You can easily automate regular investments into one or two of these funds and be invested in up to 7,800 stocks!

#finance #indexfunds #invest

December 12, 2024 at 1:49 AM

What Should I Invest In?!

I have broken out the guides to show S&P 500, Total Market, and lastly international index funds from the most popular firms.

You can easily automate regular investments into one or two of these funds and be invested in up to 7,800 stocks!

#finance #indexfunds #invest

I have broken out the guides to show S&P 500, Total Market, and lastly international index funds from the most popular firms.

You can easily automate regular investments into one or two of these funds and be invested in up to 7,800 stocks!

#finance #indexfunds #invest

Tired of being broke all the time?

Allow me to introduce the…

50/30/20 Budget: An guide on how to structure your spending.

Best Practices

1. Track spending

2. Automate your savings

3. Prioritize debt repayment

4. Adjust as lifestyle changes

#budgeting #growwealth #personalfinance

Allow me to introduce the…

50/30/20 Budget: An guide on how to structure your spending.

Best Practices

1. Track spending

2. Automate your savings

3. Prioritize debt repayment

4. Adjust as lifestyle changes

#budgeting #growwealth #personalfinance

December 7, 2024 at 2:20 AM

Tired of being broke all the time?

Allow me to introduce the…

50/30/20 Budget: An guide on how to structure your spending.

Best Practices

1. Track spending

2. Automate your savings

3. Prioritize debt repayment

4. Adjust as lifestyle changes

#budgeting #growwealth #personalfinance

Allow me to introduce the…

50/30/20 Budget: An guide on how to structure your spending.

Best Practices

1. Track spending

2. Automate your savings

3. Prioritize debt repayment

4. Adjust as lifestyle changes

#budgeting #growwealth #personalfinance

Want to be a millionaire by 40? Here’s how:

1️⃣ 10% to your 401k + 5% match

2️⃣ Max Roth IRA

3️⃣ Max HSA

Invest $1,500/month at an 8% return starting at 18, and by 40, you’ll have $1.1M!

Take control of your future—start now. Follow for more tips!

#SimpleInvesting #FinancialFreedom #WealthBuilding

1️⃣ 10% to your 401k + 5% match

2️⃣ Max Roth IRA

3️⃣ Max HSA

Invest $1,500/month at an 8% return starting at 18, and by 40, you’ll have $1.1M!

Take control of your future—start now. Follow for more tips!

#SimpleInvesting #FinancialFreedom #WealthBuilding

November 27, 2024 at 2:21 AM

Want to be a millionaire by 40? Here’s how:

1️⃣ 10% to your 401k + 5% match

2️⃣ Max Roth IRA

3️⃣ Max HSA

Invest $1,500/month at an 8% return starting at 18, and by 40, you’ll have $1.1M!

Take control of your future—start now. Follow for more tips!

#SimpleInvesting #FinancialFreedom #WealthBuilding

1️⃣ 10% to your 401k + 5% match

2️⃣ Max Roth IRA

3️⃣ Max HSA

Invest $1,500/month at an 8% return starting at 18, and by 40, you’ll have $1.1M!

Take control of your future—start now. Follow for more tips!

#SimpleInvesting #FinancialFreedom #WealthBuilding

The Power of Investing: My thread last night inspired me to make these visuals. I hope you find value in them, and they motivate you to achieve your financial goals, and the exponential power of compound interest.

Comment below and follow if you found this helpful or inspiring 😊

#investingtips

Comment below and follow if you found this helpful or inspiring 😊

#investingtips

November 22, 2024 at 8:15 PM

The Power of Investing: My thread last night inspired me to make these visuals. I hope you find value in them, and they motivate you to achieve your financial goals, and the exponential power of compound interest.

Comment below and follow if you found this helpful or inspiring 😊

#investingtips

Comment below and follow if you found this helpful or inspiring 😊

#investingtips

Investing used to intimidate me—a LOT! Then I discovered total market funds. These funds track 3,000+ stocks, have low fees, and make investing simple. Here’s a quick guide to 4 major total market funds with key details to help you get started!

#InvestingMadeEasy #IndexFunds #FinanceTips

#InvestingMadeEasy #IndexFunds #FinanceTips

November 20, 2024 at 9:14 PM

Investing used to intimidate me—a LOT! Then I discovered total market funds. These funds track 3,000+ stocks, have low fees, and make investing simple. Here’s a quick guide to 4 major total market funds with key details to help you get started!

#InvestingMadeEasy #IndexFunds #FinanceTips

#InvestingMadeEasy #IndexFunds #FinanceTips

Build your wealth with these 4 must-have accounts!

Each offers unique tax benefits and growth potential. Learn how to maximize them!

Which of these do you use today? Share your thoughts below!

#PersonalFinance #WealthBuilding #FinanceTips #Guide #RetirementSavings #InvestingTips

Each offers unique tax benefits and growth potential. Learn how to maximize them!

Which of these do you use today? Share your thoughts below!

#PersonalFinance #WealthBuilding #FinanceTips #Guide #RetirementSavings #InvestingTips

November 20, 2024 at 12:11 AM

Build your wealth with these 4 must-have accounts!

Each offers unique tax benefits and growth potential. Learn how to maximize them!

Which of these do you use today? Share your thoughts below!

#PersonalFinance #WealthBuilding #FinanceTips #Guide #RetirementSavings #InvestingTips

Each offers unique tax benefits and growth potential. Learn how to maximize them!

Which of these do you use today? Share your thoughts below!

#PersonalFinance #WealthBuilding #FinanceTips #Guide #RetirementSavings #InvestingTips

Hey, Bsky!

I made this guide to break down the Boglehead asset allocation strategy inspired by John Bogle’s Little Book of Common Sense Investing. Simple, low-cost, and focused on long-term growth!

If you find this insightful, please share!

#Bogleheads #InvestingTips #FinancialLiteracy #FIRE

I made this guide to break down the Boglehead asset allocation strategy inspired by John Bogle’s Little Book of Common Sense Investing. Simple, low-cost, and focused on long-term growth!

If you find this insightful, please share!

#Bogleheads #InvestingTips #FinancialLiteracy #FIRE

November 16, 2024 at 2:31 PM

Hey, Bsky!

I made this guide to break down the Boglehead asset allocation strategy inspired by John Bogle’s Little Book of Common Sense Investing. Simple, low-cost, and focused on long-term growth!

If you find this insightful, please share!

#Bogleheads #InvestingTips #FinancialLiteracy #FIRE

I made this guide to break down the Boglehead asset allocation strategy inspired by John Bogle’s Little Book of Common Sense Investing. Simple, low-cost, and focused on long-term growth!

If you find this insightful, please share!

#Bogleheads #InvestingTips #FinancialLiteracy #FIRE