Mattias Vermeiren

@mattvermeir.bsky.social

Associate Professor of International Political Economy at Ghent University

ECB Executives argued that dampening demand was needed not only to cool off labour markets but also to force firms to absorb higher wage costs into lower profit margins, leading to "profit-led disinflation." Monetary tightening was presented as distributionally neutral, even as real wages fell.

October 20, 2025 at 12:16 PM

ECB Executives argued that dampening demand was needed not only to cool off labour markets but also to force firms to absorb higher wage costs into lower profit margins, leading to "profit-led disinflation." Monetary tightening was presented as distributionally neutral, even as real wages fell.

After initially blaming "transitory" external factors, their narrative shifted to the risk of second-round effects and "tit-for-tat" inflation: they increasingly stressed the role of overly tight labour markets while also acknowledging the role of profits.

October 20, 2025 at 12:11 PM

After initially blaming "transitory" external factors, their narrative shifted to the risk of second-round effects and "tit-for-tat" inflation: they increasingly stressed the role of overly tight labour markets while also acknowledging the role of profits.

We identify 2 discursive strategies:

1. NECESSITATION: Framing tightening as essential to anchor inflation expectations and fix demand-supply imbalances

2. DIFFUSION: Masking the anti-labour bias by arguing that rate hikes curb both wage and profit inflation and are distributionally neutral in LT

1. NECESSITATION: Framing tightening as essential to anchor inflation expectations and fix demand-supply imbalances

2. DIFFUSION: Masking the anti-labour bias by arguing that rate hikes curb both wage and profit inflation and are distributionally neutral in LT

October 20, 2025 at 12:04 PM

We identify 2 discursive strategies:

1. NECESSITATION: Framing tightening as essential to anchor inflation expectations and fix demand-supply imbalances

2. DIFFUSION: Masking the anti-labour bias by arguing that rate hikes curb both wage and profit inflation and are distributionally neutral in LT

1. NECESSITATION: Framing tightening as essential to anchor inflation expectations and fix demand-supply imbalances

2. DIFFUSION: Masking the anti-labour bias by arguing that rate hikes curb both wage and profit inflation and are distributionally neutral in LT

First two points are well taken but data from (presumably?) more reliable sources like the IEA point on the same direction, right? Sure, China is dominant. But it’s also happening elsewhere in the GS. www.iea.org/reports/rene...

February 26, 2025 at 10:47 AM

First two points are well taken but data from (presumably?) more reliable sources like the IEA point on the same direction, right? Sure, China is dominant. But it’s also happening elsewhere in the GS. www.iea.org/reports/rene...

I keep finding it difficult to square @brettchristophers.bsky.social’s perceptive analysis of the lack of profitability of renewable energy investment with the rapid expansion in capex on renewables in the Global North and the Global South. Evidence of massive derisking? rmi.org/wp-content/u...

February 26, 2025 at 10:21 AM

I keep finding it difficult to square @brettchristophers.bsky.social’s perceptive analysis of the lack of profitability of renewable energy investment with the rapid expansion in capex on renewables in the Global North and the Global South. Evidence of massive derisking? rmi.org/wp-content/u...

I happened to have done a similar exercise for my euro class last November

February 11, 2025 at 9:43 PM

I happened to have done a similar exercise for my euro class last November

February 11, 2025 at 5:58 PM

A content analysis of transcripts of legislative hearings of the ECB president and the Fed chair indicates that members of the US House of Representatives (USHR) were considerably more dovish than MEPs, where hawkish legislators usually outnumber dovish legislators (11/n)

January 15, 2025 at 9:07 AM

A content analysis of transcripts of legislative hearings of the ECB president and the Fed chair indicates that members of the US House of Representatives (USHR) were considerably more dovish than MEPs, where hawkish legislators usually outnumber dovish legislators (11/n)

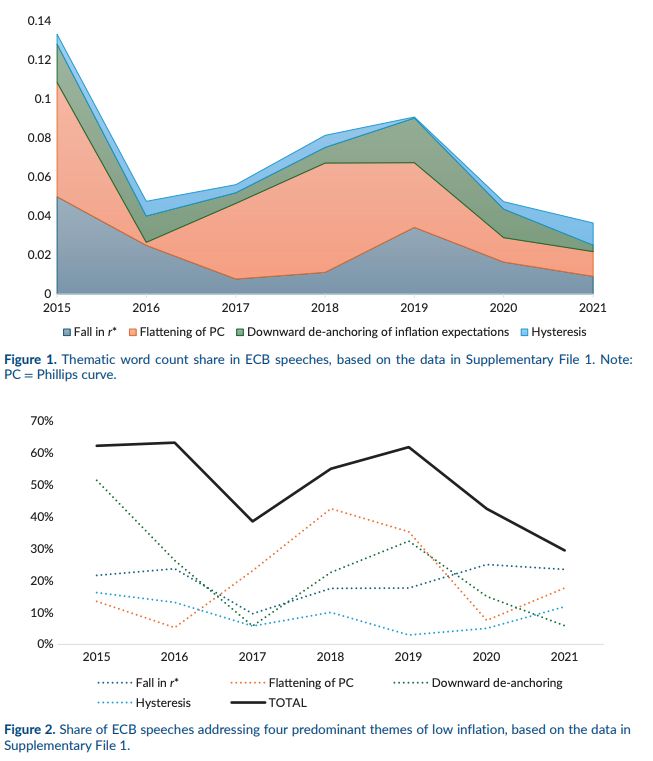

To shift the blame for too low inflation, they consistently referred to (a) the fall in the “neutral” interest rate and (b) the flattening of the Phillips curve. Yet, they were still concerned about (c) the risk of downward de-anchoring of inflation expectations undermining their credibility (8/n)

January 15, 2025 at 9:03 AM

To shift the blame for too low inflation, they consistently referred to (a) the fall in the “neutral” interest rate and (b) the flattening of the Phillips curve. Yet, they were still concerned about (c) the risk of downward de-anchoring of inflation expectations undermining their credibility (8/n)

Before 2020/21 BoE and ECB policymakers were also very dismissive of the idea of greening their corporate asset purchases, relying on the self-imposed principle of “market neutrality” (5/n)

February 15, 2024 at 10:12 AM

Before 2020/21 BoE and ECB policymakers were also very dismissive of the idea of greening their corporate asset purchases, relying on the self-imposed principle of “market neutrality” (5/n)

Relying on the literature on bureaucratic reputation, we distinguish legal-procedural, socio-political, performative, and technical reputation. Reputational concerns can be enabling or constraining depending on how central bankers value their different audiences’ opinions (3/n)

February 15, 2024 at 10:10 AM

Relying on the literature on bureaucratic reputation, we distinguish legal-procedural, socio-political, performative, and technical reputation. Reputational concerns can be enabling or constraining depending on how central bankers value their different audiences’ opinions (3/n)