Macrodispatch

@macrodispatch.bsky.social

Stir/energy/macro/ai-->(graphs)--> are cool

Transforming macro into charts one data point at a time

Formerly @stoneX @macrohive @themacrocompass

#finsky #econsky

Heres part of my work:

Macrodispatch.com

Transforming macro into charts one data point at a time

Formerly @stoneX @macrohive @themacrocompass

#finsky #econsky

Heres part of my work:

Macrodispatch.com

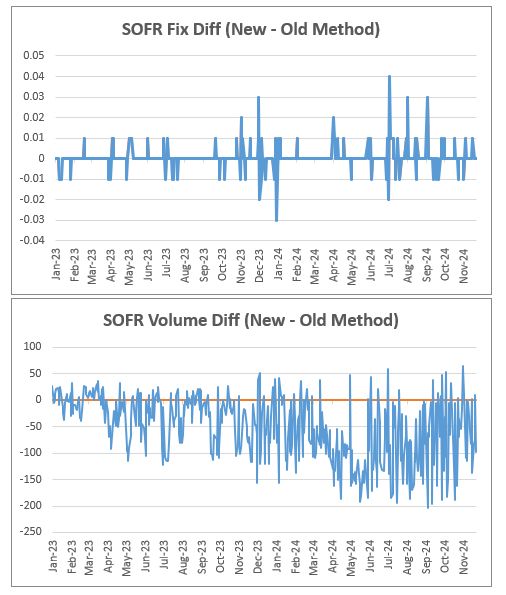

Mt mate @arishisays.bsky.social calculated we can expect SOFR volumes to fall a bit because some transactions are out..

And month end fixes can be 1bp wider.

And month end fixes can be 1bp wider.

November 27, 2024 at 10:35 PM

Mt mate @arishisays.bsky.social calculated we can expect SOFR volumes to fall a bit because some transactions are out..

And month end fixes can be 1bp wider.

And month end fixes can be 1bp wider.

So TLDR,

Lower specials impact

Ad-hoc affiliated institutions Triming,

=

Cleaner Read of repo conditions of money markets and not specific collateral demand.

Lower specials impact

Ad-hoc affiliated institutions Triming,

=

Cleaner Read of repo conditions of money markets and not specific collateral demand.

November 27, 2024 at 10:35 PM

So TLDR,

Lower specials impact

Ad-hoc affiliated institutions Triming,

=

Cleaner Read of repo conditions of money markets and not specific collateral demand.

Lower specials impact

Ad-hoc affiliated institutions Triming,

=

Cleaner Read of repo conditions of money markets and not specific collateral demand.

For the New people repo on "Specials" are collateral that is in higher demand then Others, thefore trade at a lower level since dealers may compete for it to offer it to its final clients (Normally HF in the non-cleared repo segment).

November 27, 2024 at 10:35 PM

For the New people repo on "Specials" are collateral that is in higher demand then Others, thefore trade at a lower level since dealers may compete for it to offer it to its final clients (Normally HF in the non-cleared repo segment).

it would eliminate trades that were in the 25th volume-weighted percentile rate of the DVP FICC

November 27, 2024 at 10:35 PM

it would eliminate trades that were in the 25th volume-weighted percentile rate of the DVP FICC

The second modification adjusts the mechanism applied to mitigate the influence of “specials” transactions by removing a consistent 20 percent of the lowest-rate transaction volume in FICC DVP Repos

How was it before?

How was it before?

November 27, 2024 at 10:35 PM

The second modification adjusts the mechanism applied to mitigate the influence of “specials” transactions by removing a consistent 20 percent of the lowest-rate transaction volume in FICC DVP Repos

How was it before?

How was it before?

Transactions will be excluded on a "best efforts" basis, where neither of the affiliated institutions appears to be acting in a fiduciary capacity.

November 27, 2024 at 10:35 PM

Transactions will be excluded on a "best efforts" basis, where neither of the affiliated institutions appears to be acting in a fiduciary capacity.

1. The New York Fed excludes transactions between affiliated institutions when relevant and when the data to make such exclusions are available.

how you may ask?

how you may ask?

November 27, 2024 at 10:35 PM

1. The New York Fed excludes transactions between affiliated institutions when relevant and when the data to make such exclusions are available.

how you may ask?

how you may ask?

November 22, 2024 at 4:13 PM

6/ I’ve built a visual mapping of these flows to make the paper’s insights easier to understand. Stay tuned for the release and check out the live repo monitor here:

November 18, 2024 at 5:27 PM

6/ I’ve built a visual mapping of these flows to make the paper’s insights easier to understand. Stay tuned for the release and check out the live repo monitor here:

5/ This complex process matches collateral speculators with cash lenders, keeping the repo market liquid and busting the liquidity in the deepest market of the world

US Bonds Markets

With the OFR’s initiative, we gain a clearer view of the mechanisms behind the most liquid market in the world.

US Bonds Markets

With the OFR’s initiative, we gain a clearer view of the mechanisms behind the most liquid market in the world.

November 18, 2024 at 5:27 PM

5/ This complex process matches collateral speculators with cash lenders, keeping the repo market liquid and busting the liquidity in the deepest market of the world

US Bonds Markets

With the OFR’s initiative, we gain a clearer view of the mechanisms behind the most liquid market in the world.

US Bonds Markets

With the OFR’s initiative, we gain a clearer view of the mechanisms behind the most liquid market in the world.

4/ Repo dealers in the study earn in this transaction based on spreads of rehypothecation data:

$175 million for Treasuries.

$209 million for non-Treasuries.

These margins are driven by offsetting transactions with rehypothecated collateral.

$175 million for Treasuries.

$209 million for non-Treasuries.

These margins are driven by offsetting transactions with rehypothecated collateral.

November 18, 2024 at 5:27 PM

4/ Repo dealers in the study earn in this transaction based on spreads of rehypothecation data:

$175 million for Treasuries.

$209 million for non-Treasuries.

These margins are driven by offsetting transactions with rehypothecated collateral.

$175 million for Treasuries.

$209 million for non-Treasuries.

These margins are driven by offsetting transactions with rehypothecated collateral.

3/ Visualizing these flows offers insight into where most rehypothecation happens.

For example, dealers often reuse GC collateral in tri-party repos to raise cash.

That cash can then be lent into NCCBR and DVP markets.

For example, dealers often reuse GC collateral in tri-party repos to raise cash.

That cash can then be lent into NCCBR and DVP markets.

November 18, 2024 at 5:27 PM

3/ Visualizing these flows offers insight into where most rehypothecation happens.

For example, dealers often reuse GC collateral in tri-party repos to raise cash.

That cash can then be lent into NCCBR and DVP markets.

For example, dealers often reuse GC collateral in tri-party repos to raise cash.

That cash can then be lent into NCCBR and DVP markets.

2/ A new OFR paper (dropped Friday) dives deep into this dynamic, providing fresh flow data.

Here's what it uncovered:

65% of received collateral is rehypothecated.

This is below the Federal Reserve's Regulation T limit of 140%.

Here's what it uncovered:

65% of received collateral is rehypothecated.

This is below the Federal Reserve's Regulation T limit of 140%.

November 18, 2024 at 5:27 PM

2/ A new OFR paper (dropped Friday) dives deep into this dynamic, providing fresh flow data.

Here's what it uncovered:

65% of received collateral is rehypothecated.

This is below the Federal Reserve's Regulation T limit of 140%.

Here's what it uncovered:

65% of received collateral is rehypothecated.

This is below the Federal Reserve's Regulation T limit of 140%.

Whos been Buying Brazilian Equitties

November 17, 2024 at 6:20 PM

Whos been Buying Brazilian Equitties

Also, cant that be just that the higher fiscal response from the US Relative to peers helped create demand for high wage industries, there fore better avg job oportunitties

November 14, 2024 at 1:35 PM

Also, cant that be just that the higher fiscal response from the US Relative to peers helped create demand for high wage industries, there fore better avg job oportunitties

for free eia interactive analytics 5 minutes after release, i be dropping it here on bluesky

www.macrodispatch.com/weekly-energy/

www.macrodispatch.com/weekly-energy/

November 13, 2024 at 3:24 PM

for free eia interactive analytics 5 minutes after release, i be dropping it here on bluesky

www.macrodispatch.com/weekly-energy/

www.macrodispatch.com/weekly-energy/

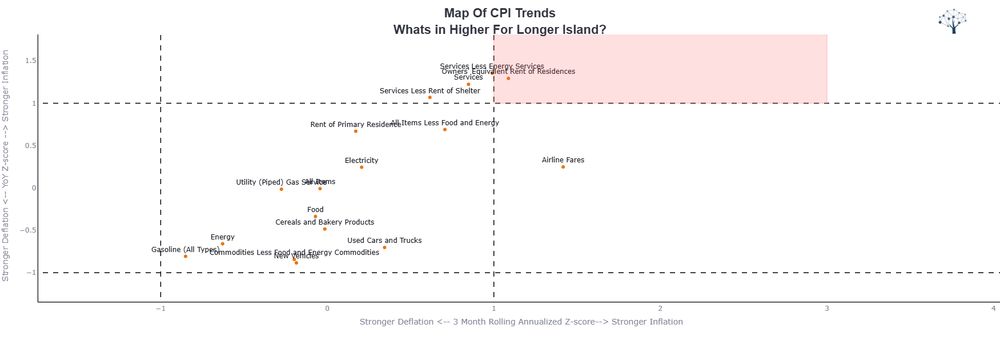

OER and Services Having the Highest Inflation Pressure on a YoY and 3M annualized basis

November 13, 2024 at 3:00 PM

OER and Services Having the Highest Inflation Pressure on a YoY and 3M annualized basis