Jay Kahn

@jstatistic.bsky.social

Economist working on repo, Treasuries and money markets. Views are my own.

We discuss it some more here www.financialresearch.gov/briefs/files...

www.financialresearch.gov

March 4, 2025 at 8:27 PM

We discuss it some more here www.financialresearch.gov/briefs/files...

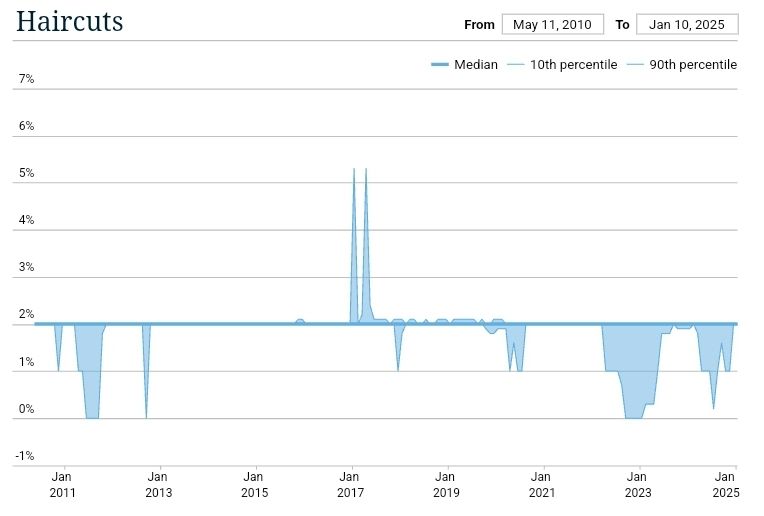

Even with these reasons in hand, that triparty haircuts are so uniformly at or near 2% regardless of market conditions suggests this may be a useful convention for traders trying to pack a lot of transactions into very little time, rather than carefully calibrated protection.

February 18, 2025 at 2:32 PM

Even with these reasons in hand, that triparty haircuts are so uniformly at or near 2% regardless of market conditions suggests this may be a useful convention for traders trying to pack a lot of transactions into very little time, rather than carefully calibrated protection.

Reason 3: Many tri-party lenders are money market funds bound by 2a-7.

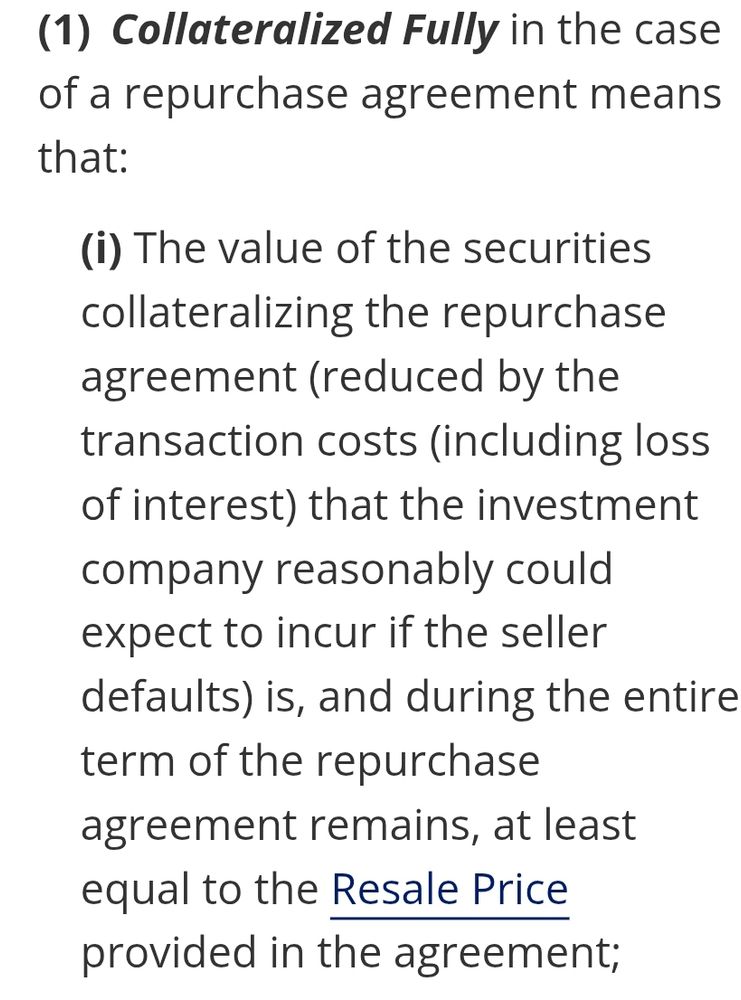

They are allowed to treat repo as an investment in the underlying security only if it is "collateralized fully," which may be interpreted as requiring a strictly positive haircut under the definition below.

They are allowed to treat repo as an investment in the underlying security only if it is "collateralized fully," which may be interpreted as requiring a strictly positive haircut under the definition below.

February 18, 2025 at 2:32 PM

Reason 3: Many tri-party lenders are money market funds bound by 2a-7.

They are allowed to treat repo as an investment in the underlying security only if it is "collateralized fully," which may be interpreted as requiring a strictly positive haircut under the definition below.

They are allowed to treat repo as an investment in the underlying security only if it is "collateralized fully," which may be interpreted as requiring a strictly positive haircut under the definition below.

Reason 2: Triparty is a general collateral market meaning that dealers have an incentive to use their worst collateral. So they aren't concerned about losing collateral.

Bilateral is specific collateral and may be used to source securities the borrower doesn't want to lose.

Bilateral is specific collateral and may be used to source securities the borrower doesn't want to lose.

February 18, 2025 at 2:32 PM

Reason 2: Triparty is a general collateral market meaning that dealers have an incentive to use their worst collateral. So they aren't concerned about losing collateral.

Bilateral is specific collateral and may be used to source securities the borrower doesn't want to lose.

Bilateral is specific collateral and may be used to source securities the borrower doesn't want to lose.

Meanwhile, bilateral features a lot of both borrowing and lending by hedge funds to dealers, so sometimes it may be the dealer-borrower who need protection rather than the lender.

www.financialresearch.gov/briefs/files...

www.financialresearch.gov/briefs/files...

February 18, 2025 at 2:32 PM

Meanwhile, bilateral features a lot of both borrowing and lending by hedge funds to dealers, so sometimes it may be the dealer-borrower who need protection rather than the lender.

www.financialresearch.gov/briefs/files...

www.financialresearch.gov/briefs/files...

Three big reasons for the gap:

Reason 1: Counterparty risk in triparty is generally lower—triparty is mostly safe banks and money market funds lending to riskier dealers—so lenders generally demand protection.

www.federalreserve.gov/econres/note...

Reason 1: Counterparty risk in triparty is generally lower—triparty is mostly safe banks and money market funds lending to riskier dealers—so lenders generally demand protection.

www.federalreserve.gov/econres/note...

February 18, 2025 at 2:32 PM

Three big reasons for the gap:

Reason 1: Counterparty risk in triparty is generally lower—triparty is mostly safe banks and money market funds lending to riskier dealers—so lenders generally demand protection.

www.federalreserve.gov/econres/note...

Reason 1: Counterparty risk in triparty is generally lower—triparty is mostly safe banks and money market funds lending to riskier dealers—so lenders generally demand protection.

www.federalreserve.gov/econres/note...

2% haircuts have become a fixation for many thinking about hypothetical minimum margins.

Since we've had the triparty data for a long time, people have gotten used to thinking 2% was "correct," but as we point out in the note triparty is a very different market from bilateral.

Since we've had the triparty data for a long time, people have gotten used to thinking 2% was "correct," but as we point out in the note triparty is a very different market from bilateral.

February 18, 2025 at 2:32 PM

2% haircuts have become a fixation for many thinking about hypothetical minimum margins.

Since we've had the triparty data for a long time, people have gotten used to thinking 2% was "correct," but as we point out in the note triparty is a very different market from bilateral.

Since we've had the triparty data for a long time, people have gotten used to thinking 2% was "correct," but as we point out in the note triparty is a very different market from bilateral.

We also argue that cross-margining should be applied where practicable, for instance in cash-futures basis trades.

While cross-margining may allow greater leverage, it also reduces risk of firesales if volatility increases by accounting for correlations between cash and futures

While cross-margining may allow greater leverage, it also reduces risk of firesales if volatility increases by accounting for correlations between cash and futures

February 14, 2025 at 3:03 PM

We also argue that cross-margining should be applied where practicable, for instance in cash-futures basis trades.

While cross-margining may allow greater leverage, it also reduces risk of firesales if volatility increases by accounting for correlations between cash and futures

While cross-margining may allow greater leverage, it also reduces risk of firesales if volatility increases by accounting for correlations between cash and futures

More generally, proportionate margins reflect the full set of risks of exposures and collateral surrounding a transaction.

To the extent exposures offset, as for correlated collateral in a "netted package," that should be reflected in margin collected.

To the extent exposures offset, as for correlated collateral in a "netted package," that should be reflected in margin collected.

February 14, 2025 at 3:03 PM

More generally, proportionate margins reflect the full set of risks of exposures and collateral surrounding a transaction.

To the extent exposures offset, as for correlated collateral in a "netted package," that should be reflected in margin collected.

To the extent exposures offset, as for correlated collateral in a "netted package," that should be reflected in margin collected.

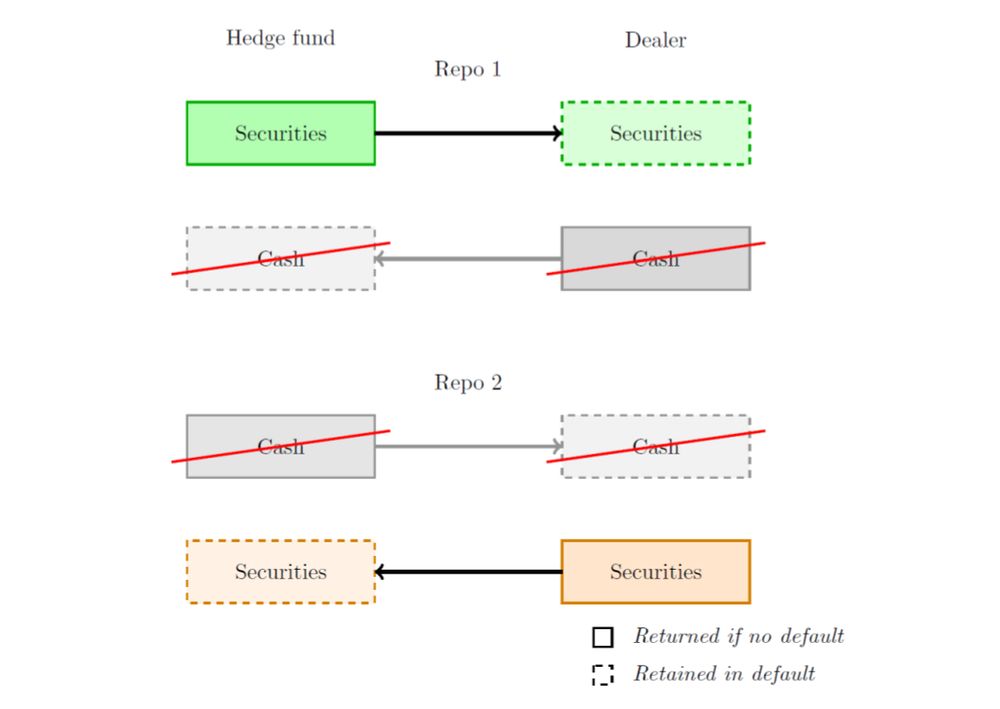

Our previous research showed that in this case, haircuts are often negative, to provide the dealer with protection against the hedge fund.

A consistent minimum haircut would undo this protection, since it would instead require a payment 𝘧𝘳𝘰𝘮 the dealer 𝘵𝘰 the hedge fund.

A consistent minimum haircut would undo this protection, since it would instead require a payment 𝘧𝘳𝘰𝘮 the dealer 𝘵𝘰 the hedge fund.

February 14, 2025 at 3:03 PM

Our previous research showed that in this case, haircuts are often negative, to provide the dealer with protection against the hedge fund.

A consistent minimum haircut would undo this protection, since it would instead require a payment 𝘧𝘳𝘰𝘮 the dealer 𝘵𝘰 the hedge fund.

A consistent minimum haircut would undo this protection, since it would instead require a payment 𝘧𝘳𝘰𝘮 the dealer 𝘵𝘰 the hedge fund.

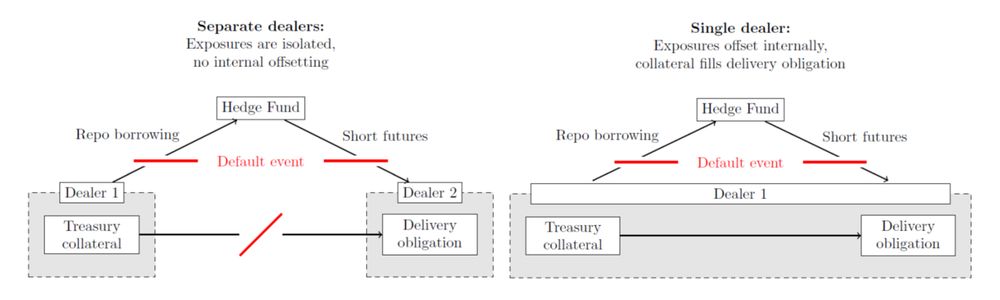

For example, sometimes hedge funds will source a specific Treasury by lending against it to a dealer.

In this case, even though the hedge fund is the lender, the dealer is the one who needs a cushion to protect against losing a valuable security to the hedge fund's default.

In this case, even though the hedge fund is the lender, the dealer is the one who needs a cushion to protect against losing a valuable security to the hedge fund's default.

February 14, 2025 at 3:03 PM

For example, sometimes hedge funds will source a specific Treasury by lending against it to a dealer.

In this case, even though the hedge fund is the lender, the dealer is the one who needs a cushion to protect against losing a valuable security to the hedge fund's default.

In this case, even though the hedge fund is the lender, the dealer is the one who needs a cushion to protect against losing a valuable security to the hedge fund's default.

Instead, proportionate margins should:

1) Protect all participants in a transaction (not just one side),

2) Reflect both counterparty and collateral risk,

3) Account for the full portfolio of exposures between counterparties.

Minimum haircuts don't satisfy these properties.

1) Protect all participants in a transaction (not just one side),

2) Reflect both counterparty and collateral risk,

3) Account for the full portfolio of exposures between counterparties.

Minimum haircuts don't satisfy these properties.

February 14, 2025 at 3:03 PM

Instead, proportionate margins should:

1) Protect all participants in a transaction (not just one side),

2) Reflect both counterparty and collateral risk,

3) Account for the full portfolio of exposures between counterparties.

Minimum haircuts don't satisfy these properties.

1) Protect all participants in a transaction (not just one side),

2) Reflect both counterparty and collateral risk,

3) Account for the full portfolio of exposures between counterparties.

Minimum haircuts don't satisfy these properties.

Recent research by my coauthors and me finds that over 70% of haircuts in non-centrally cleared bilateral repo are zero, leaving no cushion for lenders.

www.financialresearch.gov/briefs/files...

This has, in turn, sparked interest in mandatory minimum haircuts in repo.

www.financialresearch.gov/briefs/files...

This has, in turn, sparked interest in mandatory minimum haircuts in repo.

www.financialresearch.gov

February 14, 2025 at 3:03 PM

Recent research by my coauthors and me finds that over 70% of haircuts in non-centrally cleared bilateral repo are zero, leaving no cushion for lenders.

www.financialresearch.gov/briefs/files...

This has, in turn, sparked interest in mandatory minimum haircuts in repo.

www.financialresearch.gov/briefs/files...

This has, in turn, sparked interest in mandatory minimum haircuts in repo.

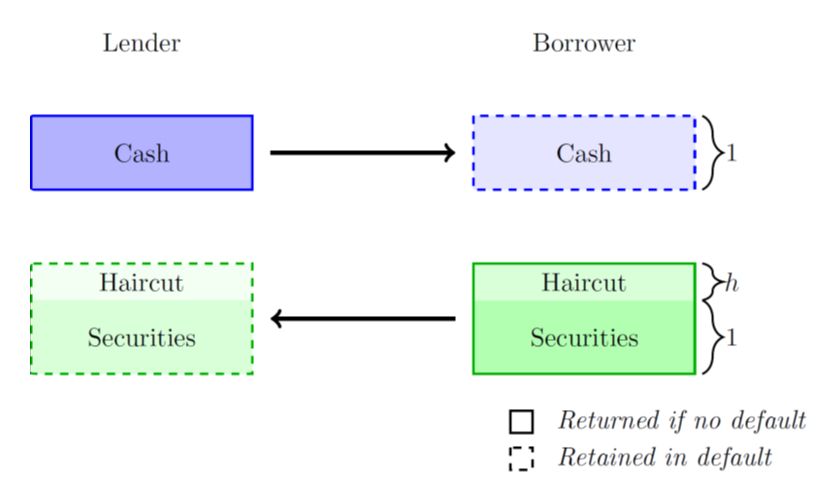

A positive haircut provides a cushion if the borrower defaults, helping the lender recover losses even if the collateral’s value dips or proves costly to liquidate.

February 14, 2025 at 3:03 PM

A positive haircut provides a cushion if the borrower defaults, helping the lender recover losses even if the collateral’s value dips or proves costly to liquidate.

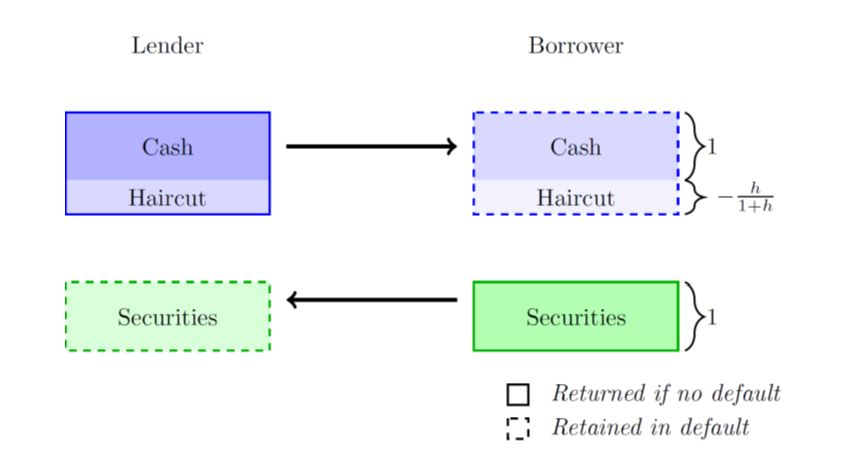

Outside of clearing, repo margining is determined by "haircuts": a degree of overcollateralization that guards against default risk.

For instance, if you lend $100 and require $102 of collateral, the haircut is 2%.

For instance, if you lend $100 and require $102 of collateral, the haircut is 2%.

February 14, 2025 at 3:03 PM

Outside of clearing, repo margining is determined by "haircuts": a degree of overcollateralization that guards against default risk.

For instance, if you lend $100 and require $102 of collateral, the haircut is 2%.

For instance, if you lend $100 and require $102 of collateral, the haircut is 2%.

In the counterfactual, Tyler is stuck behind me in his car as I take up the *full lane* on my bike.

November 22, 2024 at 12:22 AM

In the counterfactual, Tyler is stuck behind me in his car as I take up the *full lane* on my bike.

Going forward I'll be updating this data on a quarterly basis, adding new series and improving the data quality as I go. Any comments or questions are welcome!

November 17, 2024 at 7:13 PM

Going forward I'll be updating this data on a quarterly basis, adding new series and improving the data quality as I go. Any comments or questions are welcome!

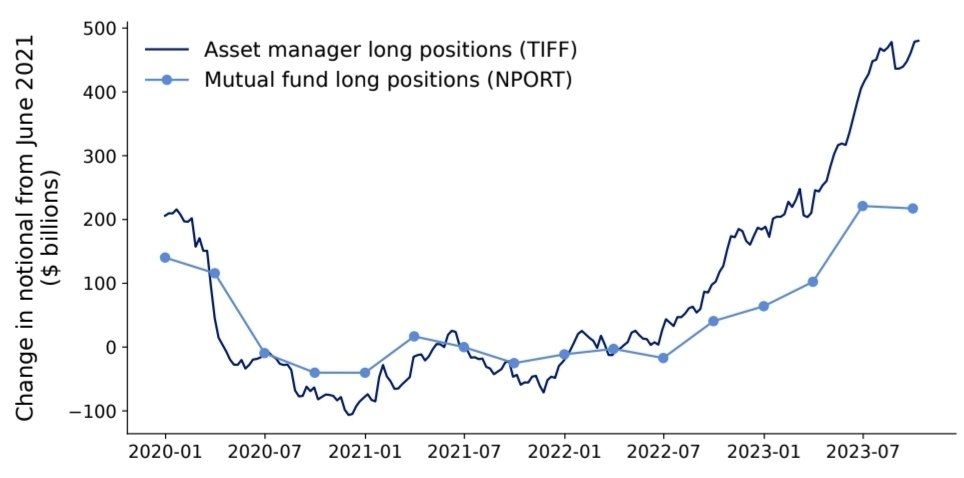

This data was compiled for our paper on mutual funds' use of Treasury futures: papers.ssrn.com/sol3/papers....

It's totally free, but we ask that if you use the data you cite the working paper

It's totally free, but we ask that if you use the data you cite the working paper

November 17, 2024 at 7:13 PM

This data was compiled for our paper on mutual funds' use of Treasury futures: papers.ssrn.com/sol3/papers....

It's totally free, but we ask that if you use the data you cite the working paper

It's totally free, but we ask that if you use the data you cite the working paper

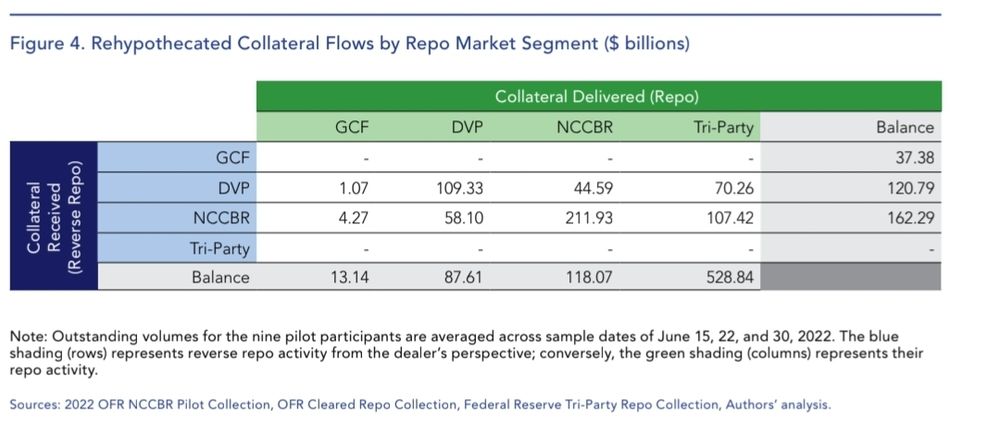

Tracking the flow of collateral across markets allows us to see useful patterns such as the that most tri-party collateral is not sourced from other repo markets (since valuable collateral will be locked up) but bilateral markets are more likely to circulate and reuse collateral.

November 14, 2024 at 5:21 PM

Tracking the flow of collateral across markets allows us to see useful patterns such as the that most tri-party collateral is not sourced from other repo markets (since valuable collateral will be locked up) but bilateral markets are more likely to circulate and reuse collateral.