@itaxjournal.bsky.social

Tax lotteries incentivize consumers to ask for receipts, but effectiveness depends on design. Prizes are skewed toward high-income taxpayers, business owners, and the self-employed, driven by greater transaction volumes. These groups alter their behavior the least after winning.

October 3, 2025 at 8:20 PM

Tax lotteries incentivize consumers to ask for receipts, but effectiveness depends on design. Prizes are skewed toward high-income taxpayers, business owners, and the self-employed, driven by greater transaction volumes. These groups alter their behavior the least after winning.

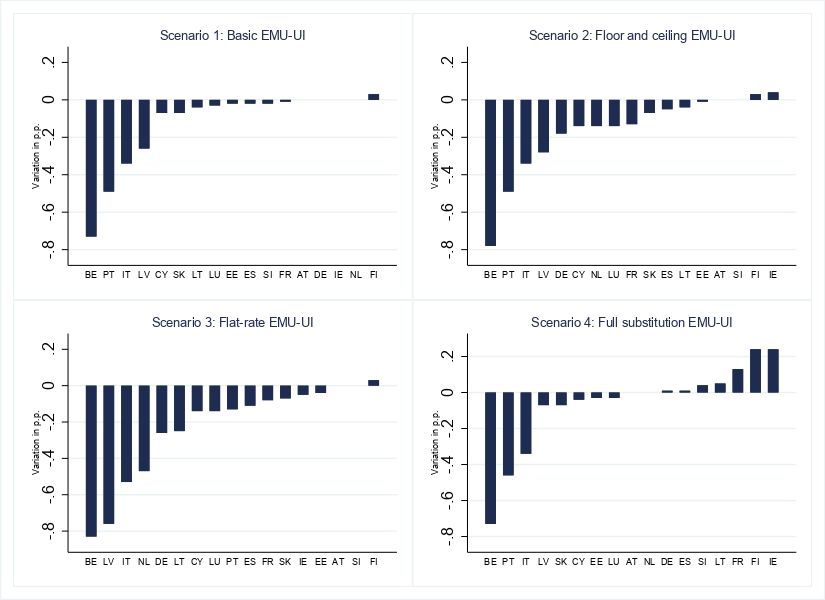

Simulations of a common unemployment benefit system across European countries indicate that a common replacement rate, paired with country-specific floors and ceilings, reduces poverty while keeping labour supply responses and budgetary costs modest.

October 2, 2025 at 4:39 PM

Simulations of a common unemployment benefit system across European countries indicate that a common replacement rate, paired with country-specific floors and ceilings, reduces poverty while keeping labour supply responses and budgetary costs modest.

Uganda’s 2012–13 tax reform increased revenue and modestly reduced inequality. Reported incomes of most top 1% stayed unchanged, though high earners in small firms reduced their incomes, with some employers shifting wages into dividends to lower tax.

October 1, 2025 at 5:33 PM

Uganda’s 2012–13 tax reform increased revenue and modestly reduced inequality. Reported incomes of most top 1% stayed unchanged, though high earners in small firms reduced their incomes, with some employers shifting wages into dividends to lower tax.

In China, many firms evade social insurance payments. The Golden Tax Project Phase III (GTPIII) — a digital tax upgrade — helped boost companies’ participation and payment rates by improving data sharing and closing loopholes. Gains were biggest among small, low-profit firms.

October 1, 2025 at 5:25 PM

In China, many firms evade social insurance payments. The Golden Tax Project Phase III (GTPIII) — a digital tax upgrade — helped boost companies’ participation and payment rates by improving data sharing and closing loopholes. Gains were biggest among small, low-profit firms.

Bastani's new paper provides a guide to the Marginal Value of Public Funds (MVPF), bridging theory and practice, and showing how to translate tax elasticities into welfare conclusions. It reorients the discussion, shifting focus from public spending to tax policy.

September 26, 2025 at 3:20 PM

Bastani's new paper provides a guide to the Marginal Value of Public Funds (MVPF), bridging theory and practice, and showing how to translate tax elasticities into welfare conclusions. It reorients the discussion, shifting focus from public spending to tax policy.

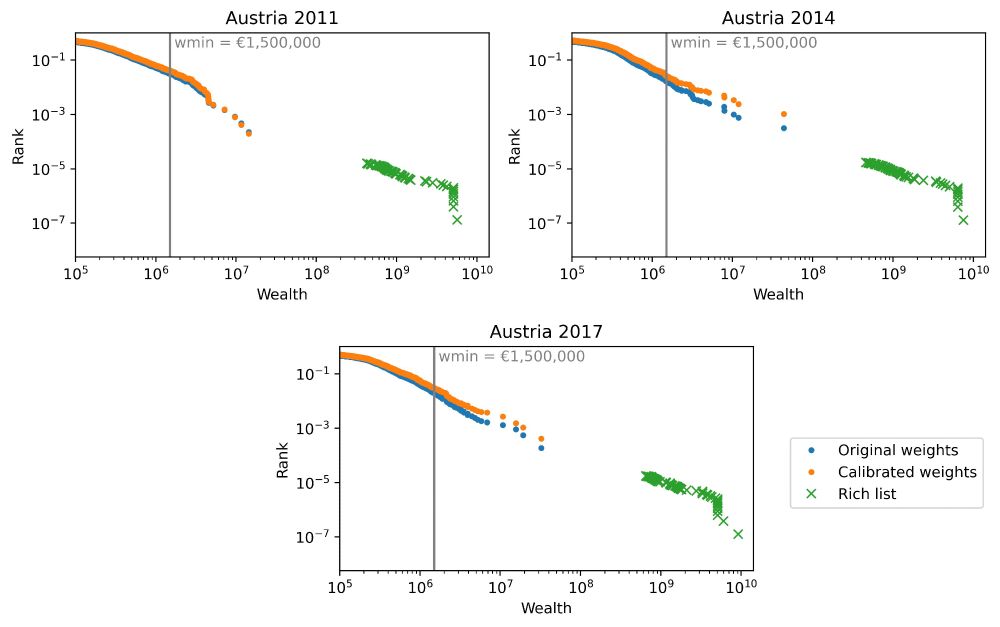

Wealth surveys suffer from the 'missing rich' problem. This paper proposes a new method to improve representativeness by calibrating the survey’s income distribution using income tax data.

July 8, 2025 at 1:23 PM

Wealth surveys suffer from the 'missing rich' problem. This paper proposes a new method to improve representativeness by calibrating the survey’s income distribution using income tax data.

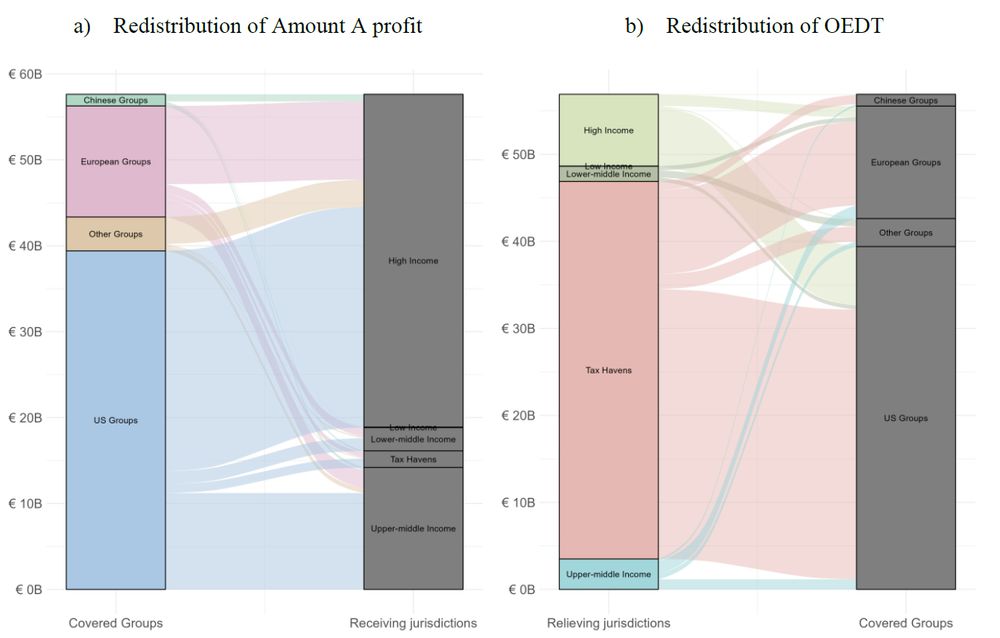

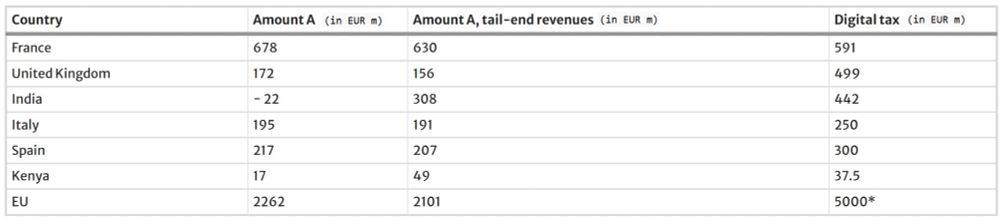

Pillar 1 Amount A reallocates taxing rights on the largest/most profitable MNEs based on final consumers' location. In 2022, it would yield €10.9B. High-income countries gain the most while tax havens bear the brunt of the cost. Net benefits compared to DSTs are ambiguous.

July 1, 2025 at 3:06 PM

Pillar 1 Amount A reallocates taxing rights on the largest/most profitable MNEs based on final consumers' location. In 2022, it would yield €10.9B. High-income countries gain the most while tax havens bear the brunt of the cost. Net benefits compared to DSTs are ambiguous.

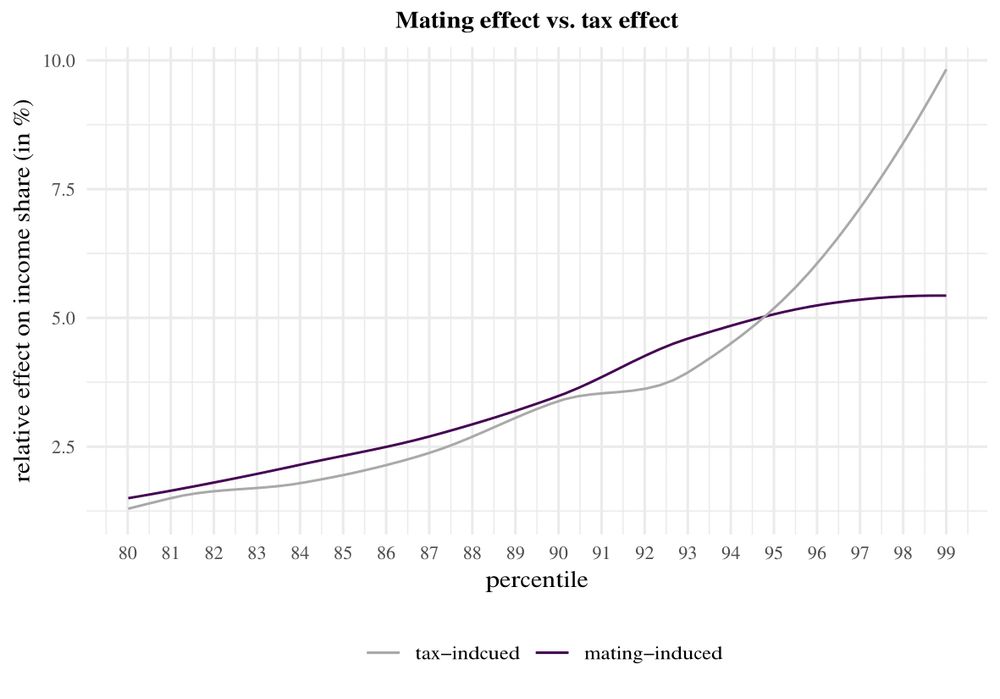

We show how marital sorting in Switzerland offsets parts of the tax system’s redistributive effect - intensifying income inequality.

June 30, 2025 at 8:49 AM

We show how marital sorting in Switzerland offsets parts of the tax system’s redistributive effect - intensifying income inequality.

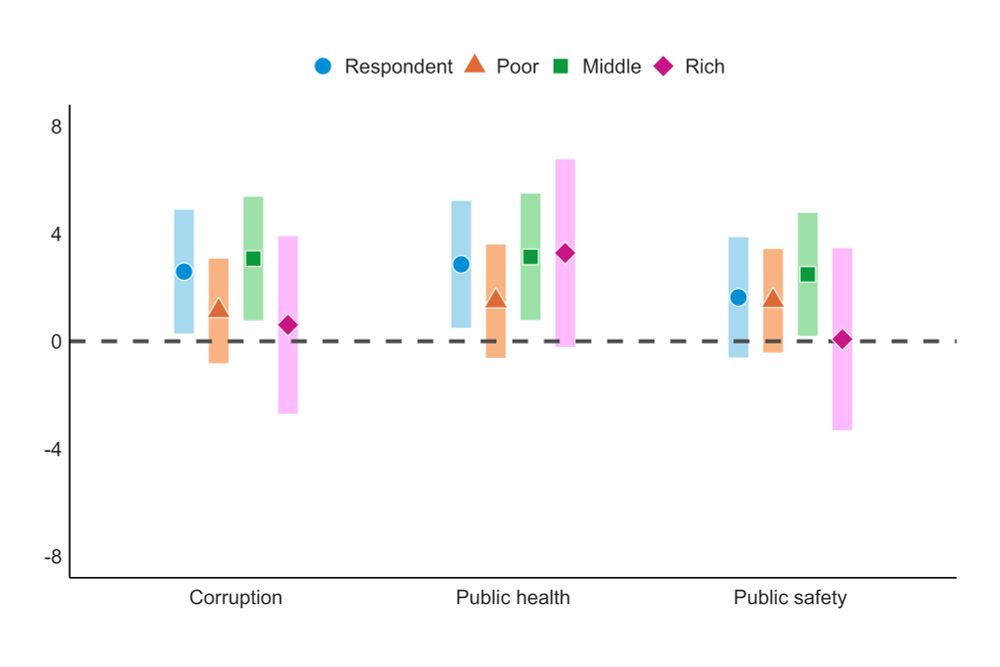

What drives support for higher taxes in Mexico? Information about eliminating corruption or improving public health raises willingness to pay, but not support for tax progressivity. The gap between inequality awareness and redistributive action persists.

June 24, 2025 at 4:10 PM

What drives support for higher taxes in Mexico? Information about eliminating corruption or improving public health raises willingness to pay, but not support for tax progressivity. The gap between inequality awareness and redistributive action persists.

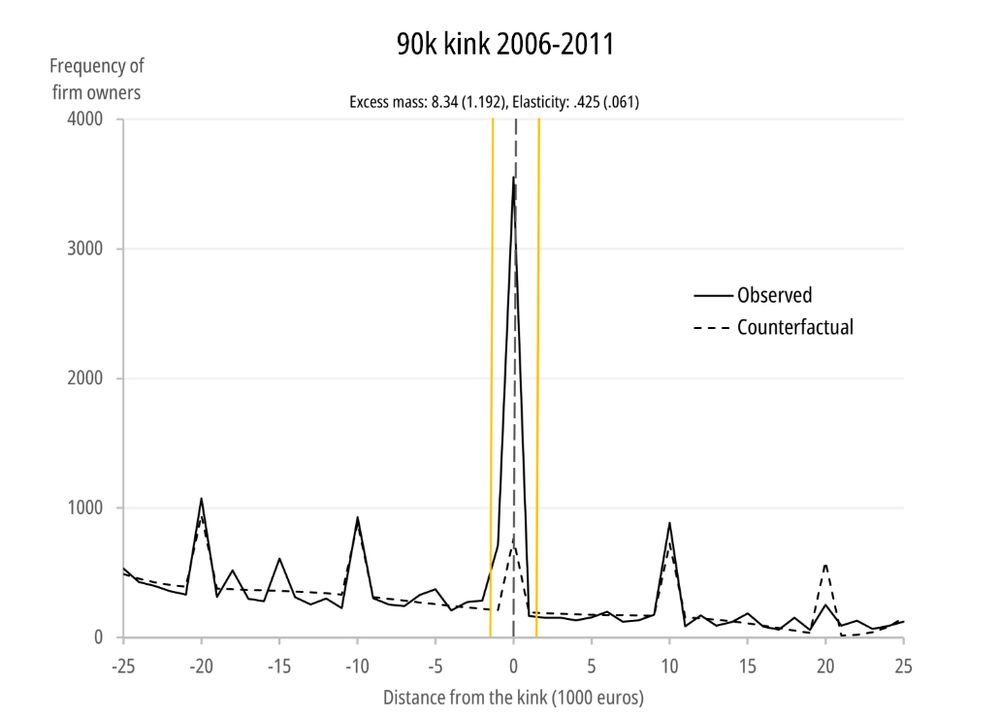

This study shows Finnish firm owners avoid higher dividend tax brackets by retaining earnings in the firm, strongly incentivized by the tax schedule, and via income-shifting between wages and dividends. Experienced and lower-income owners indicate higher tax base elasticities.

April 14, 2025 at 9:32 PM

This study shows Finnish firm owners avoid higher dividend tax brackets by retaining earnings in the firm, strongly incentivized by the tax schedule, and via income-shifting between wages and dividends. Experienced and lower-income owners indicate higher tax base elasticities.

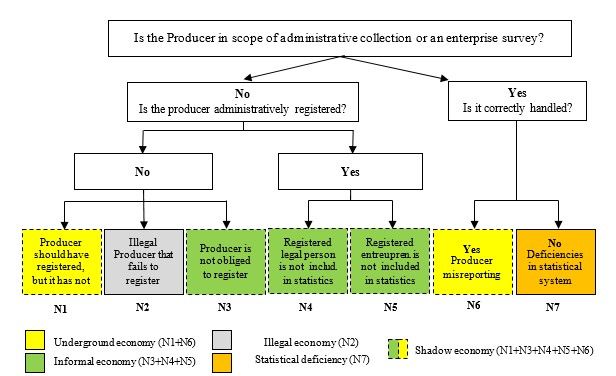

We propose a hybrid national accounts (NA)–macroeconometric approach to estimate underground, informal, and illegal economies in 22 European countries (2000–2020), bridging the gap between the demand for data on informality and the limited availability of NA-based estimates.

April 11, 2025 at 6:10 PM

We propose a hybrid national accounts (NA)–macroeconometric approach to estimate underground, informal, and illegal economies in 22 European countries (2000–2020), bridging the gap between the demand for data on informality and the limited availability of NA-based estimates.

Mandatory electronic cash registers (ECR) in Sweden raised reported revenues by 4%, but the effect faded within months—firms adapted quickly to continue underreporting. #TaxCompliance #ECR

April 10, 2025 at 8:13 PM

Mandatory electronic cash registers (ECR) in Sweden raised reported revenues by 4%, but the effect faded within months—firms adapted quickly to continue underreporting. #TaxCompliance #ECR

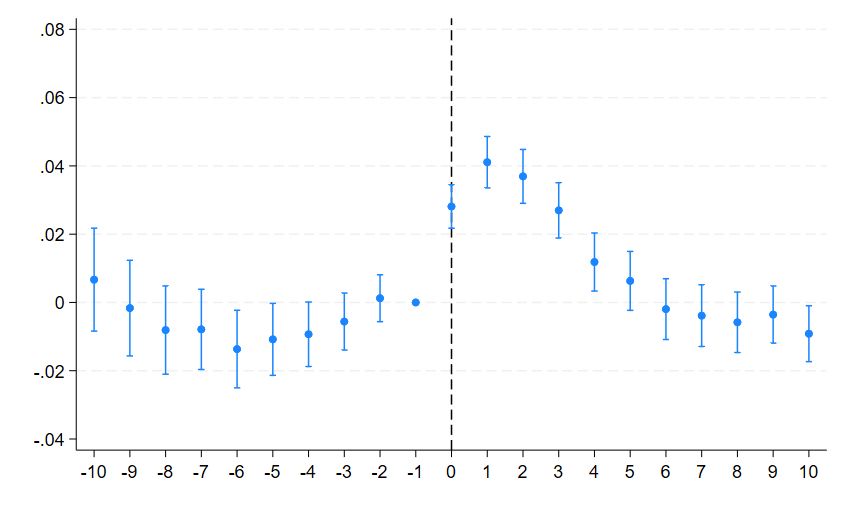

#EvidenceBasedPolicy relies on solid evaluations of policy effectiveness. We quantify the findings of #EUCohesionPolicy evaluations and show that these do not square with impact estimates of academics. Misaligned incentives or institutional frictions explain this divergence.

April 8, 2025 at 8:40 PM

#EvidenceBasedPolicy relies on solid evaluations of policy effectiveness. We quantify the findings of #EUCohesionPolicy evaluations and show that these do not square with impact estimates of academics. Misaligned incentives or institutional frictions explain this divergence.

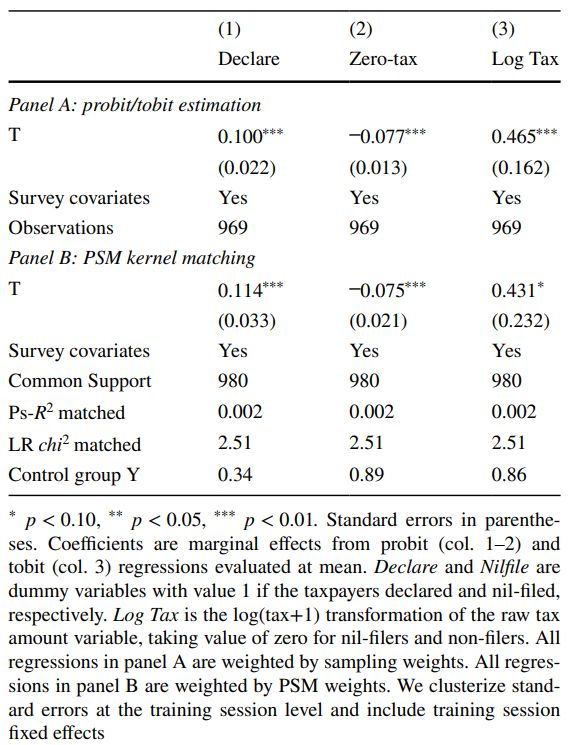

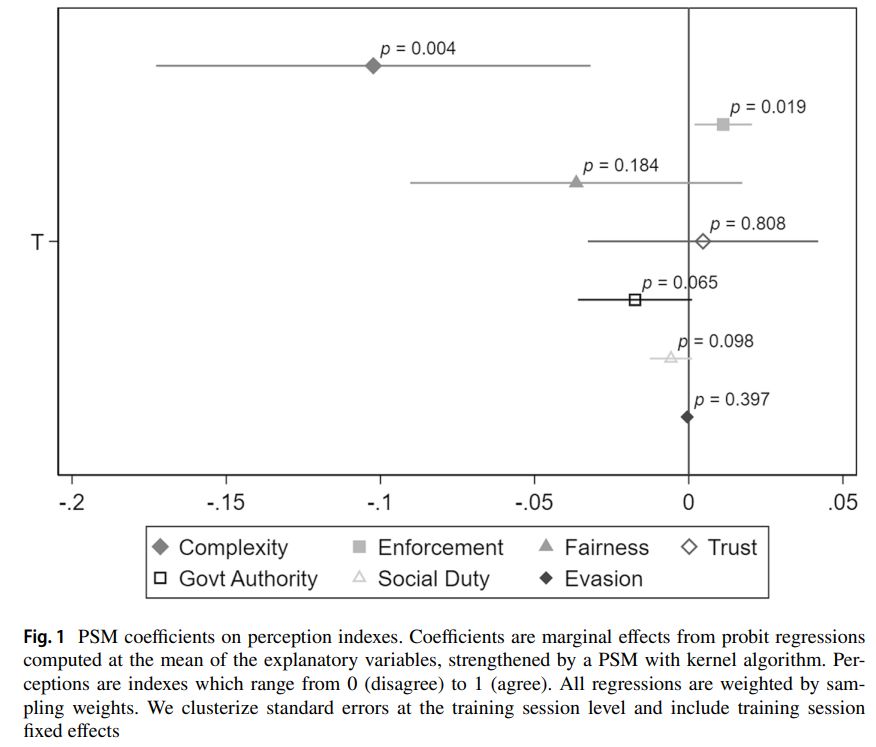

Can taxpayer education improve compliance? Evidence from Rwanda shows that training new taxpayers significantly increases filing, reduces zero-tax reporting, and boosts tax due. Effects persist over time, driven by lower compliance costs and better tax knowledge.

March 4, 2025 at 11:03 PM

Can taxpayer education improve compliance? Evidence from Rwanda shows that training new taxpayers significantly increases filing, reduces zero-tax reporting, and boosts tax due. Effects persist over time, driven by lower compliance costs and better tax knowledge.

CbCR increases transparency on the global activities of MNEs and can raise effective tax rates of MNEs. But some companies avoid the reporting requirement with private and tax-aggressive firms showing the strongest avoidance response.

February 28, 2025 at 12:28 AM

CbCR increases transparency on the global activities of MNEs and can raise effective tax rates of MNEs. But some companies avoid the reporting requirement with private and tax-aggressive firms showing the strongest avoidance response.

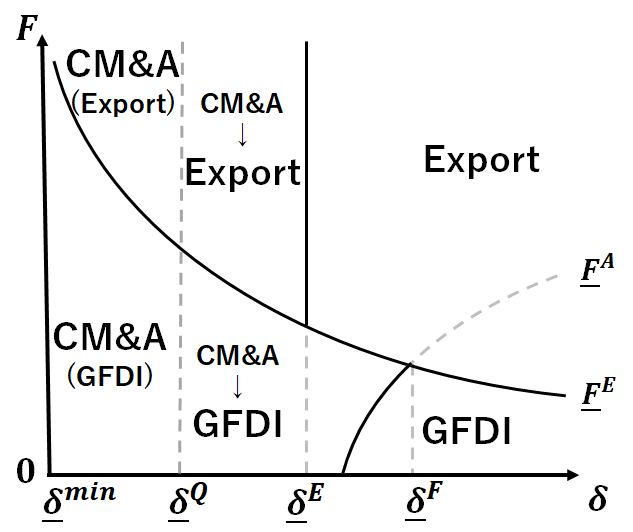

Multinational firms' tax avoidance has been observed, but firms' decisions on entry mode for foreign markets has been often ignored. This paper theoretically shows a firm prefers cross-border M&A to greenfield FDI when transfer pricing regulation is loose.

February 25, 2025 at 8:59 PM

Multinational firms' tax avoidance has been observed, but firms' decisions on entry mode for foreign markets has been often ignored. This paper theoretically shows a firm prefers cross-border M&A to greenfield FDI when transfer pricing regulation is loose.

This study uses anti-corruption investigations in China as an exogenous shock to identify the link between corruption and corporate tax evasion, finding that anti-corruption significantly discourages firm tax evasion and reduces firm tax evasion by at least 0.7%.

February 20, 2025 at 4:47 PM

This study uses anti-corruption investigations in China as an exogenous shock to identify the link between corruption and corporate tax evasion, finding that anti-corruption significantly discourages firm tax evasion and reduces firm tax evasion by at least 0.7%.

Temporary VAT reduction in Germany that was effective in 2020 was largely passed on to supermarket customers. After it was revoked, prices remained notably lower than they were before the VAT reduction.

February 11, 2025 at 11:42 PM

Temporary VAT reduction in Germany that was effective in 2020 was largely passed on to supermarket customers. After it was revoked, prices remained notably lower than they were before the VAT reduction.

Did the TCJA’s $10k SALT deduction cap cause migration out of high-tax states? Taxpayers in the top 1% of the income distribution -- whose SALT deductions were greatly devalued -- reacted quickly to the TCJA’s SALT cap by moving from high-tax states to low- and middle-tax states.

February 7, 2025 at 9:45 PM

Did the TCJA’s $10k SALT deduction cap cause migration out of high-tax states? Taxpayers in the top 1% of the income distribution -- whose SALT deductions were greatly devalued -- reacted quickly to the TCJA’s SALT cap by moving from high-tax states to low- and middle-tax states.