Immo Schott

@immoschott.bsky.social

Senior Economist at the Federal Reserve Board of Governors. I am working on macroeconomics, taxation, and finance.

https://sites.google.com/site/immoschott/research

https://sites.google.com/site/immoschott/research

This is a joint paper with Joachim, Matthias, and Timo. This version of the paper is part of the IFDP series, where IFDP stands for "International Finance Discussion Paper" and "International Finance" is the name of the division that I work for at the Federal Reserve Board.

December 9, 2024 at 9:43 PM

This is a joint paper with Joachim, Matthias, and Timo. This version of the paper is part of the IFDP series, where IFDP stands for "International Finance Discussion Paper" and "International Finance" is the name of the division that I work for at the Federal Reserve Board.

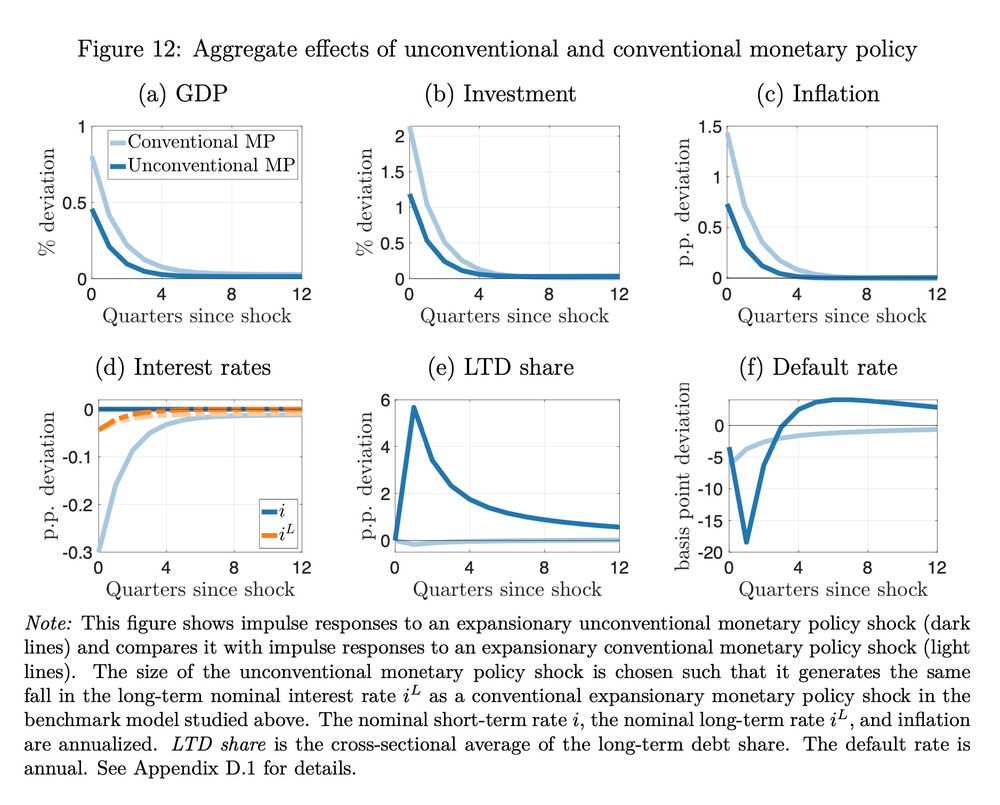

We use the model to study unconventional monetary policy (UMP). UMP lowers long-term rates when the short-term rate is at the ZLB. This has the effect that firms borrow at longer durations. The increase in debt overhang makes UMP less effective than conventional monetary policy.

December 9, 2024 at 9:43 PM

We use the model to study unconventional monetary policy (UMP). UMP lowers long-term rates when the short-term rate is at the ZLB. This has the effect that firms borrow at longer durations. The increase in debt overhang makes UMP less effective than conventional monetary policy.

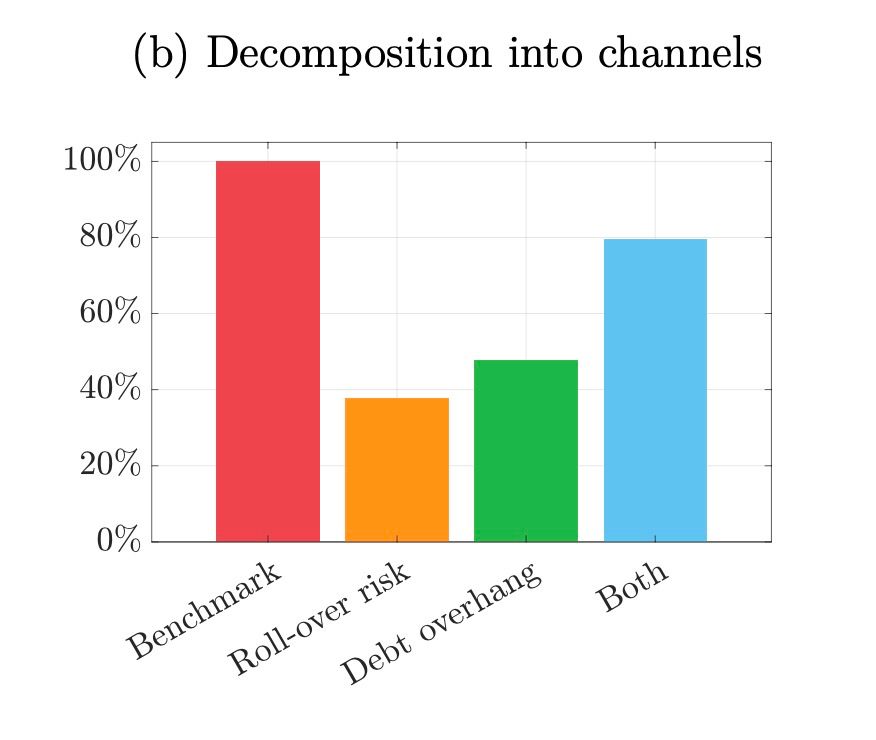

2) Debt overhang means that firms lower their investment if a part of the benefit goes to its long-term creditors. A contractionary monetary policy shock worsens debt overhang, because tighter monetary policy is deflationary, increasing the real burden of outstanding debt.

December 9, 2024 at 9:43 PM

2) Debt overhang means that firms lower their investment if a part of the benefit goes to its long-term creditors. A contractionary monetary policy shock worsens debt overhang, because tighter monetary policy is deflationary, increasing the real burden of outstanding debt.

Two channels explain our result: 1) Rollover-risk implies that if a lot of debt matures at the time when interest rates have gone up, this increases firms' cost of capital, lowering investment.

December 9, 2024 at 9:43 PM

Two channels explain our result: 1) Rollover-risk implies that if a lot of debt matures at the time when interest rates have gone up, this increases firms' cost of capital, lowering investment.

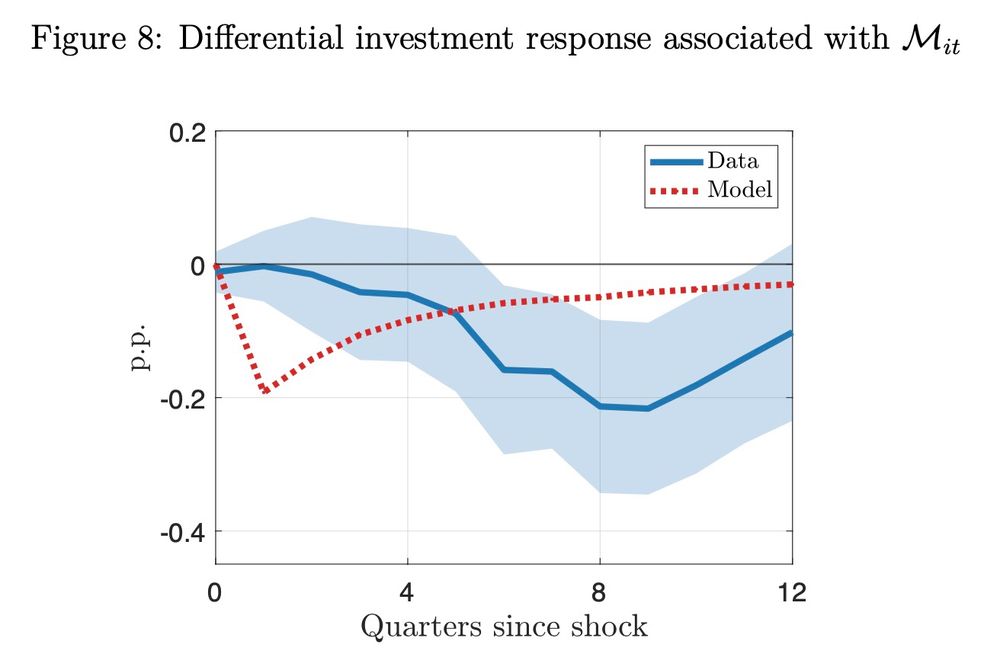

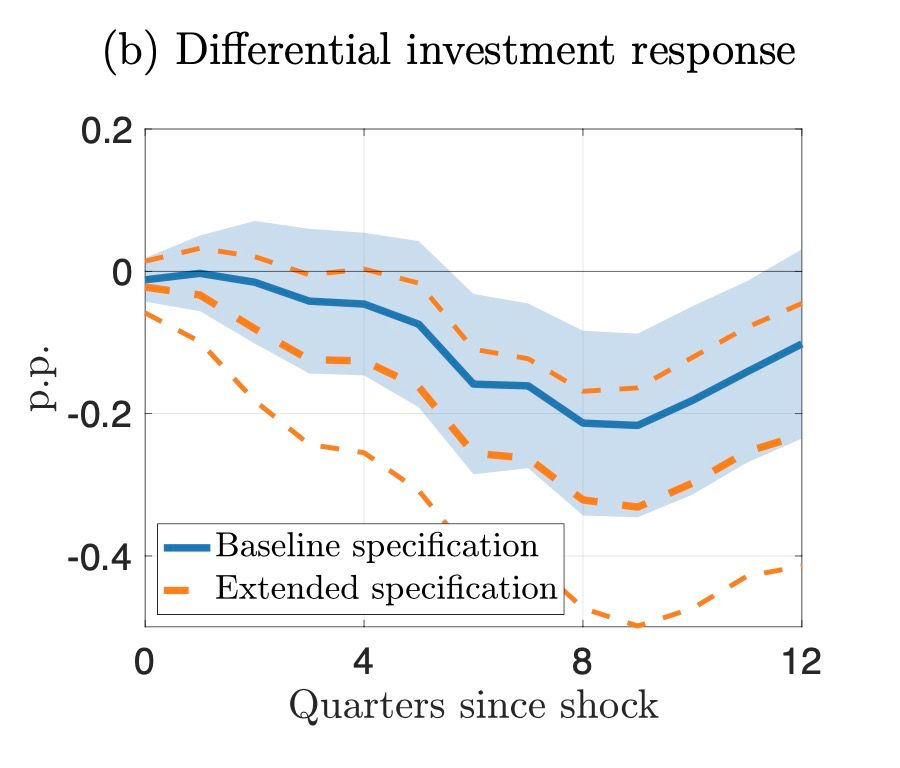

The model replicates the empirical observation that after a contractionary monetary policy shock, firms with shorter remaining debt maturity react more strongly, meaning that they reduce investment by more and that they see larger increases in credit spreads.

December 9, 2024 at 9:43 PM

The model replicates the empirical observation that after a contractionary monetary policy shock, firms with shorter remaining debt maturity react more strongly, meaning that they reduce investment by more and that they see larger increases in credit spreads.

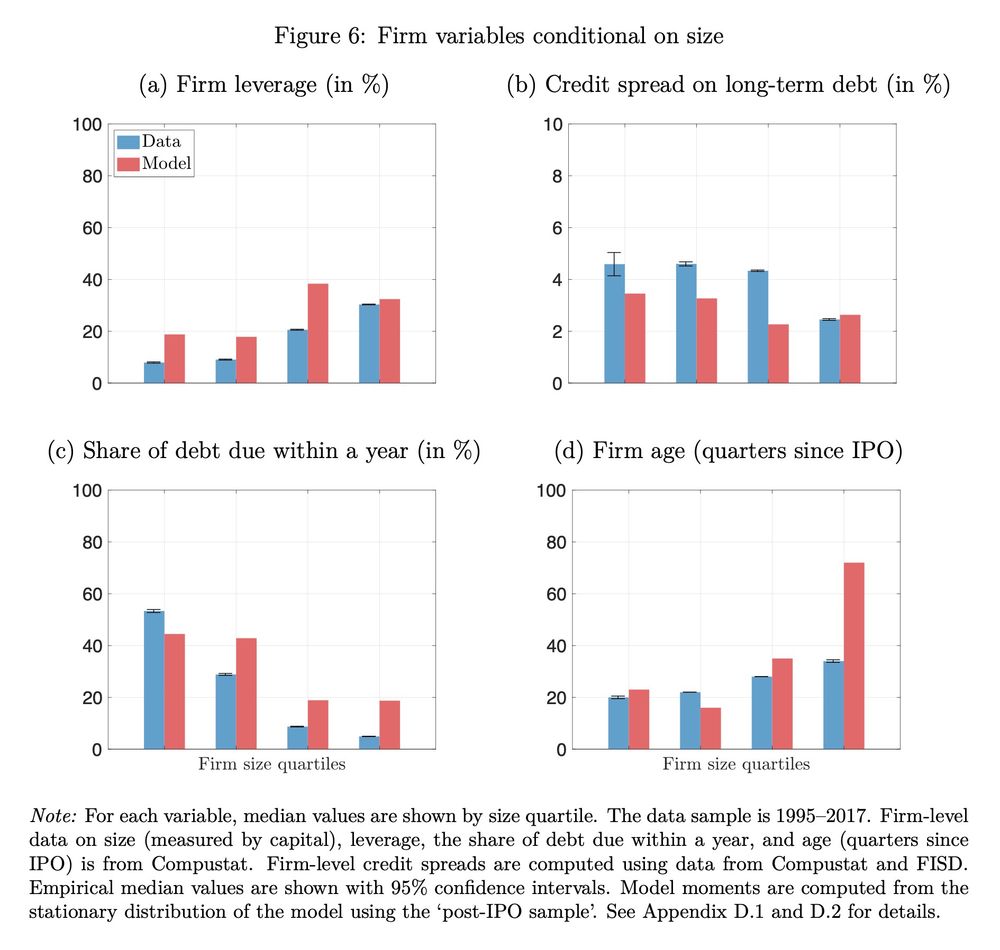

We construct a general equilibrium model with heterogeneous firms, long-term debt, and costly default. Firms raise capital, consisting of equity, long-term debt, and short-term debt. Safer firms endogenously have higher leverage, lower credit spreads, and more long-maturity debt.

December 9, 2024 at 9:43 PM

We construct a general equilibrium model with heterogeneous firms, long-term debt, and costly default. Firms raise capital, consisting of equity, long-term debt, and short-term debt. Safer firms endogenously have higher leverage, lower credit spreads, and more long-maturity debt.

This heterogeneity across firms is important if we want to understand which firms are most affected by monetary policy. It is also a crucial for assessing the macroeconomic effects of rate changes, which depends on the distribution of firms across remaining maturities.

December 9, 2024 at 9:43 PM

This heterogeneity across firms is important if we want to understand which firms are most affected by monetary policy. It is also a crucial for assessing the macroeconomic effects of rate changes, which depends on the distribution of firms across remaining maturities.

We combine balance sheet & bond-level data to construct a measure of the share of a firm's debt which matures at any given point in time. Using panel local projections, we show that investment & credit spreads react more strongly to MP when firms have higher maturing bond shares.

December 9, 2024 at 9:43 PM

We combine balance sheet & bond-level data to construct a measure of the share of a firm's debt which matures at any given point in time. Using panel local projections, we show that investment & credit spreads react more strongly to MP when firms have higher maturing bond shares.