Gabriel Mihalache

@gmihalache.bsky.social

Placeholder account. I'm on Twitter.

Just be grateful for the opportunity!

October 23, 2023 at 10:17 PM

Just be grateful for the opportunity!

What if monetary policy turns loose during default and abandons its inflation target? What is key for our mechanism is that default comes with high inflation, and not whether that's due to low productivity (baseline) or loose policy (alt).

October 18, 2023 at 6:48 PM

What if monetary policy turns loose during default and abandons its inflation target? What is key for our mechanism is that default comes with high inflation, and not whether that's due to low productivity (baseline) or loose policy (alt).

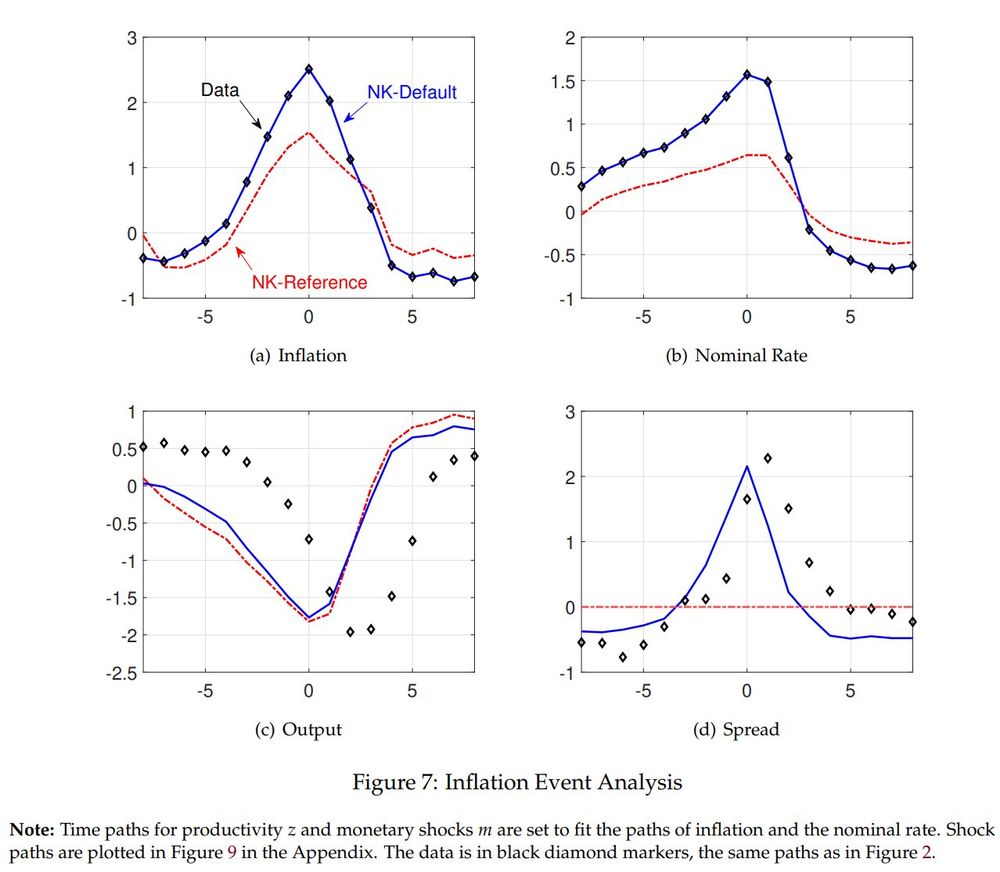

We identify temporary inflation events, times where inflation exceeds 2 sd-s above average. Our model helps make sense of these episodes. High inflation comes with high spreads, recessions, and tight monetary policy. About half of the inflation is attributable to default risk.

October 18, 2023 at 6:48 PM

We identify temporary inflation events, times where inflation exceeds 2 sd-s above average. Our model helps make sense of these episodes. High inflation comes with high spreads, recessions, and tight monetary policy. About half of the inflation is attributable to default risk.

We now use more data, in terms of countries and measures. We estimate interest rate rules and project spreads on their shocks, we use inflation expectations surveys to argue that higher default risk is associated with higher expected inflation, as in our mechanism.

October 18, 2023 at 6:48 PM

We now use more data, in terms of countries and measures. We estimate interest rate rules and project spreads on their shocks, we use inflation expectations surveys to argue that higher default risk is associated with higher expected inflation, as in our mechanism.

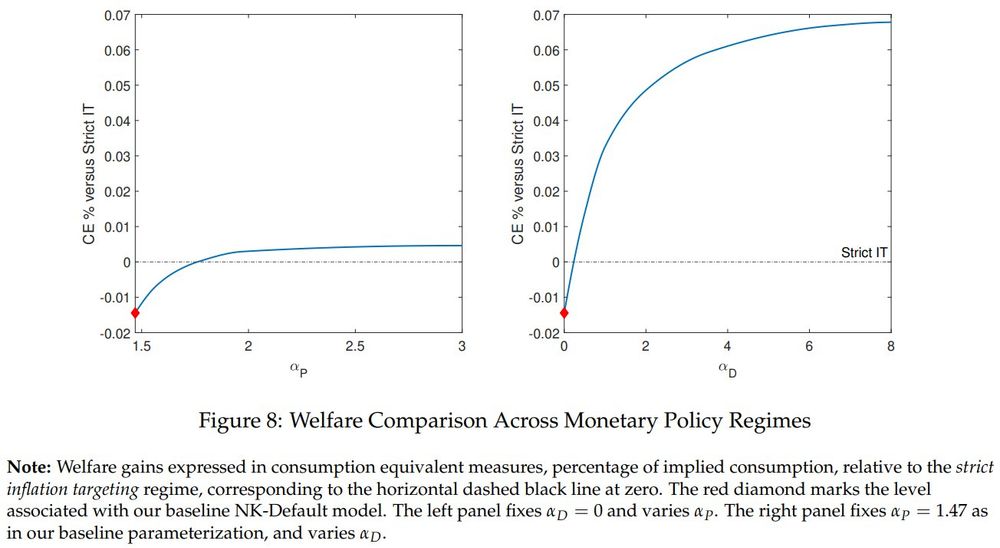

Monetary policy can deliver the flexible price allocation, but this is not desirable, not constrained efficiency. We design simple interest rate rules that deliver efficiency (in tractable model) and large welfare gains (in quant model) relative to strict inflation targeting.

October 18, 2023 at 6:48 PM

Monetary policy can deliver the flexible price allocation, but this is not desirable, not constrained efficiency. We design simple interest rate rules that deliver efficiency (in tractable model) and large welfare gains (in quant model) relative to strict inflation targeting.

The paper is built around two mechanisms, new to our setting with domestic pricing frictions and sovereign default risk: default amplification and monetary discipline. Default risk is inflationary, and domestic frictions disincentivize sovereign borrowing.

October 18, 2023 at 6:47 PM

The paper is built around two mechanisms, new to our setting with domestic pricing frictions and sovereign default risk: default amplification and monetary discipline. Default risk is inflationary, and domestic frictions disincentivize sovereign borrowing.

We're all sick in here with COVID and secondary infections so I thought I'd better monitor the situation on here, make sure nobody says anything dumb...

October 16, 2023 at 1:50 AM

We're all sick in here with COVID and secondary infections so I thought I'd better monitor the situation on here, make sure nobody says anything dumb...