Ernie Tedeschi

@ernietedeschi.bsky.social

Personal Account. Director of Economics, The Budget Lab at Yale University. Former Chief Economist, White House Council of Economic Advisers.

I'm open to the possibility that AI is having a nonzero effect on the labor market. But the varied mix of firms announcing layoffs strikes me as more consistent with the main driver here being a correction from over-hiring in the wake of the pandemic. www.wsj.com/economy/jobs...

October 29, 2025 at 3:18 PM

I'm open to the possibility that AI is having a nonzero effect on the labor market. But the varied mix of firms announcing layoffs strikes me as more consistent with the main driver here being a correction from over-hiring in the wake of the pandemic. www.wsj.com/economy/jobs...

There's still a lot of counter evidence. The NY Fed's Survey of Consumer Expectations shows similar spending growth at the bottom, middle, & top. Meanwhile, the bottom's share of aggregate wages has actually risen over the past 2 years. www.newyorkfed.org/m...

8/9

8/9

October 15, 2025 at 12:13 PM

There's still a lot of counter evidence. The NY Fed's Survey of Consumer Expectations shows similar spending growth at the bottom, middle, & top. Meanwhile, the bottom's share of aggregate wages has actually risen over the past 2 years. www.newyorkfed.org/m...

8/9

8/9

Moreover, I find that the rise in the unemployment rate over the last 2 years has been most acute for jobs most *& least* exposed to AI. So even if AI is *a* story, it's clearly not the *only* story, & we should be open to the possibility that the story is just broad weakness

6/9

6/9

October 15, 2025 at 12:13 PM

Moreover, I find that the rise in the unemployment rate over the last 2 years has been most acute for jobs most *& least* exposed to AI. So even if AI is *a* story, it's clearly not the *only* story, & we should be open to the possibility that the story is just broad weakness

6/9

6/9

But the evidence is not uniform. E.g. my colleague @marthagimbel.bsky.social & coauthors find that the recent change in the occupational mix is comparable to past technological shocks like the internet & the rise of personal computers.

budgetlab.yale.edu/r...

5/9

budgetlab.yale.edu/r...

5/9

October 15, 2025 at 12:13 PM

But the evidence is not uniform. E.g. my colleague @marthagimbel.bsky.social & coauthors find that the recent change in the occupational mix is comparable to past technological shocks like the internet & the rise of personal computers.

budgetlab.yale.edu/r...

5/9

budgetlab.yale.edu/r...

5/9

If you just looked at the gross effects of software, information equipment, & data centers on GDP, you'd conclude they added 1.3 points to 2025 H1's 1.6% SAAR growth!

Net out imports though, & the contribution falls to ~0.5pp. Still big! But just enough to offset tariffs.

3/9

Net out imports though, & the contribution falls to ~0.5pp. Still big! But just enough to offset tariffs.

3/9

October 15, 2025 at 12:13 PM

If you just looked at the gross effects of software, information equipment, & data centers on GDP, you'd conclude they added 1.3 points to 2025 H1's 1.6% SAAR growth!

Net out imports though, & the contribution falls to ~0.5pp. Still big! But just enough to offset tariffs.

3/9

Net out imports though, & the contribution falls to ~0.5pp. Still big! But just enough to offset tariffs.

3/9

One can think of our "existing fiscal distribution" as basically being the equivalent of assuming proportional spending cuts & tax hikes in the future to pay for a policy. The result is that a policy's aggregate benefit falls & its distributional impact looks quite different.

5/7

5/7

October 14, 2025 at 1:55 PM

One can think of our "existing fiscal distribution" as basically being the equivalent of assuming proportional spending cuts & tax hikes in the future to pay for a policy. The result is that a policy's aggregate benefit falls & its distributional impact looks quite different.

5/7

5/7

FISCAL EFFECTS: New 2025 tariffs raise $2.5 trillion over 2026-35 conventionally-scored and $2.0 trillion dynamically-scored.

9/10

9/10

September 27, 2025 at 12:05 AM

FISCAL EFFECTS: New 2025 tariffs raise $2.5 trillion over 2026-35 conventionally-scored and $2.0 trillion dynamically-scored.

9/10

9/10

COMMODITY PRICE EFFECTS: Consumers face particularly high increases in leather and clothing in the short-run: prices increase 36% for leather products (shoes and hand bags), 34% for apparel, and 21% for textiles.

8/10

8/10

September 27, 2025 at 12:04 AM

COMMODITY PRICE EFFECTS: Consumers face particularly high increases in leather and clothing in the short-run: prices increase 36% for leather products (shoes and hand bags), 34% for apparel, and 21% for textiles.

8/10

8/10

DISTRIBUTIONAL EFFECTS: Tariffs are a regressive tax, especially in the short-run. The average annual cost to households in the first and top income deciles from all 2025 tariffs are $1,350 and $5,350 respectively in 2025$. The median cost is $2,000 per household.

7/10

7/10

September 27, 2025 at 12:04 AM

DISTRIBUTIONAL EFFECTS: Tariffs are a regressive tax, especially in the short-run. The average annual cost to households in the first and top income deciles from all 2025 tariffs are $1,350 and $5,350 respectively in 2025$. The median cost is $2,000 per household.

7/10

7/10

GLOBAL EFFECTS: In the long-run, China real GDP is -0.3% smaller, about 3/4 of the effect to the US. The economies of Mexico, Canada, the EU, and the UK are all larger.

6/10

6/10

September 27, 2025 at 12:04 AM

GLOBAL EFFECTS: In the long-run, China real GDP is -0.3% smaller, about 3/4 of the effect to the US. The economies of Mexico, Canada, the EU, and the UK are all larger.

6/10

6/10

SECTORAL EFFECTS: In the long-run, tariffs present a trade-off. Total US manufacturing output expands by 2.7%, but advanced manufacturing shrinks by 4.2%. Moreover, the manufacturing gains are more than crowded out by other sectors: eg construction output contracts by 3.7%.

5/10

5/10

September 27, 2025 at 12:04 AM

SECTORAL EFFECTS: In the long-run, tariffs present a trade-off. Total US manufacturing output expands by 2.7%, but advanced manufacturing shrinks by 4.2%. Moreover, the manufacturing gains are more than crowded out by other sectors: eg construction output contracts by 3.7%.

5/10

5/10

ECONOMIC/LABOR MARKET EFFECTS: US real GDP growth is -0.5pp lower over 2025 & -0.4pp lower over 2026. The level of US real GDP is persistently -0.4% smaller in the long-run. By the end of 2025, the unemployment rate is +0.3pp higher & employment is -490K lower.

4/10

4/10

September 27, 2025 at 12:04 AM

ECONOMIC/LABOR MARKET EFFECTS: US real GDP growth is -0.5pp lower over 2025 & -0.4pp lower over 2026. The level of US real GDP is persistently -0.4% smaller in the long-run. By the end of 2025, the unemployment rate is +0.3pp higher & employment is -490K lower.

4/10

4/10

TARIFF RATE: The September 25 announcement raises the average effective tariff rate by 0.5pp to 17.9% pre-substitution (as of Oct 1), the highest since 1934. After consumers & businesses shift their spending mix, the post-substitution rate is 16.7%, highest since 1936.

2/10

2/10

September 27, 2025 at 12:04 AM

TARIFF RATE: The September 25 announcement raises the average effective tariff rate by 0.5pp to 17.9% pre-substitution (as of Oct 1), the highest since 1934. After consumers & businesses shift their spending mix, the post-substitution rate is 16.7%, highest since 1936.

2/10

2/10

New @budgetlab.bsky.social tariff update out tonight, incorporating the heavy truck, furniture, and pharmaceutical tariffs announced by President Trump yesterday. Details are still sparse; we will update in the future as more specifics about the policy are published.

In brief...

1/10

In brief...

1/10

September 27, 2025 at 12:04 AM

New @budgetlab.bsky.social tariff update out tonight, incorporating the heavy truck, furniture, and pharmaceutical tariffs announced by President Trump yesterday. Details are still sparse; we will update in the future as more specifics about the policy are published.

In brief...

1/10

In brief...

1/10

The preliminary benchmark revision of -911K amounts to -0.6% to March 2025 payroll employment. Combined with 2-month revisions, recent total revisions are big but hardly unprecedented, & smoothed over the business cycle the payroll survey has gotten more accurate over time.

September 9, 2025 at 2:01 PM

The preliminary benchmark revision of -911K amounts to -0.6% to March 2025 payroll employment. Combined with 2-month revisions, recent total revisions are big but hardly unprecedented, & smoothed over the business cycle the payroll survey has gotten more accurate over time.

3. The long-run hit to US real GDP levels is now only -0.1%, but there is still an outsized negative effect on advanced manufacturing (due to the remaining 232 tariffs).

4. The effective tariff rate would be 6.8%, still the highest since 1969.

11/12

4. The effective tariff rate would be 6.8%, still the highest since 1969.

11/12

September 4, 2025 at 7:16 PM

3. The long-run hit to US real GDP levels is now only -0.1%, but there is still an outsized negative effect on advanced manufacturing (due to the remaining 232 tariffs).

4. The effective tariff rate would be 6.8%, still the highest since 1969.

11/12

4. The effective tariff rate would be 6.8%, still the highest since 1969.

11/12

But what if the IEEPA tariffs were both 1) overturned, & 2) not replaced? We show a "No IEEPA" scenario assuming a SCOTUS decision in June 2026. A few highlights:

1. IEEPA tariffs make up ~70% of the 2025 tariffs to date.

2. Revenues shrink to $700B over 2026-2035.

10/12

1. IEEPA tariffs make up ~70% of the 2025 tariffs to date.

2. Revenues shrink to $700B over 2026-2035.

10/12

September 4, 2025 at 7:16 PM

But what if the IEEPA tariffs were both 1) overturned, & 2) not replaced? We show a "No IEEPA" scenario assuming a SCOTUS decision in June 2026. A few highlights:

1. IEEPA tariffs make up ~70% of the 2025 tariffs to date.

2. Revenues shrink to $700B over 2026-2035.

10/12

1. IEEPA tariffs make up ~70% of the 2025 tariffs to date.

2. Revenues shrink to $700B over 2026-2035.

10/12

All tariffs to date in 2025 raise $2.4 trillion over 2026-35, with $454 billion in negative dynamic revenue effects, bringing dynamic revenues to $2.0 trillion.

9/12

9/12

September 4, 2025 at 7:16 PM

All tariffs to date in 2025 raise $2.4 trillion over 2026-35, with $454 billion in negative dynamic revenue effects, bringing dynamic revenues to $2.0 trillion.

9/12

9/12

Canada cessation of most retaliation significantly eases the economic burden they bear relative to our prior estimates: long-run Canadian real GDP is now 0.1% higher. China’s economy is -0.3% smaller, nearly 3/4 as large as the hit to the US.

8/12

8/12

September 4, 2025 at 7:16 PM

Canada cessation of most retaliation significantly eases the economic burden they bear relative to our prior estimates: long-run Canadian real GDP is now 0.1% higher. China’s economy is -0.3% smaller, nearly 3/4 as large as the hit to the US.

8/12

8/12

In the long-run, tariffs present a trade-off. US manufacturing output expands by 2.7%, but these gains are more than crowded out by other sectors: construction output contracts by 3.8% and mining declines by 1.6%.

7/12

7/12

September 4, 2025 at 7:16 PM

In the long-run, tariffs present a trade-off. US manufacturing output expands by 2.7%, but these gains are more than crowded out by other sectors: construction output contracts by 3.8% and mining declines by 1.6%.

7/12

7/12

US real GDP growth over 2025 & 2026 is 0.5pp & 0.4pp lower respectively from all 2025 tariffs. In the long-run, the US economy is persistently 0.4% smaller, the equivalent of $120B annually in 2024$.

The unemployment rate rises 0.3pp by the end of 2025, & 0.7pp by end-2026.

6/12

The unemployment rate rises 0.3pp by the end of 2025, & 0.7pp by end-2026.

6/12

September 4, 2025 at 7:16 PM

US real GDP growth over 2025 & 2026 is 0.5pp & 0.4pp lower respectively from all 2025 tariffs. In the long-run, the US economy is persistently 0.4% smaller, the equivalent of $120B annually in 2024$.

The unemployment rate rises 0.3pp by the end of 2025, & 0.7pp by end-2026.

6/12

The unemployment rate rises 0.3pp by the end of 2025, & 0.7pp by end-2026.

6/12

The 2025 tariffs disproportionately affect clothing and textiles, with consumers facing 37% higher shoe prices and 35% higher apparel prices in the short-run. Shoes and apparel prices stay 13% higher in the long-run.

5/12

5/12

September 4, 2025 at 7:15 PM

The 2025 tariffs disproportionately affect clothing and textiles, with consumers facing 37% higher shoe prices and 35% higher apparel prices in the short-run. Shoes and apparel prices stay 13% higher in the long-run.

5/12

5/12

Tariffs are a regressive tax, especially in the short-run. The short-run burden on 1st decile households (as a % of income) is >3x that of the top decile (-3.5% versus -1.0%). The average annual cost to the 1st & top decile are $1,300 & $5,200 respectively; median is $2,000.

4/12

4/12

September 4, 2025 at 7:15 PM

Tariffs are a regressive tax, especially in the short-run. The short-run burden on 1st decile households (as a % of income) is >3x that of the top decile (-3.5% versus -1.0%). The average annual cost to the 1st & top decile are $1,300 & $5,200 respectively; median is $2,000.

4/12

4/12

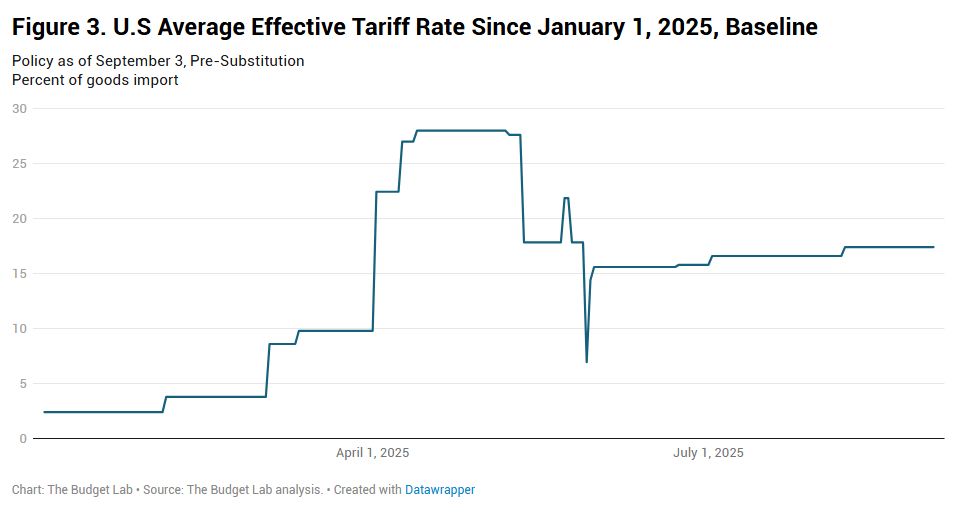

Under our all-tariff baseline, consumers face an effective tariff rate of 17.4%, a 15.0pp increase from 2024 & the highest since 1935. After shifts in spending in reaction to the tariffs, the effective tariff rate will be 16.4%, a 13.9pp increase & the highest since 1936

2/12

September 4, 2025 at 7:15 PM

Under our all-tariff baseline, consumers face an effective tariff rate of 17.4%, a 15.0pp increase from 2024 & the highest since 1935. After shifts in spending in reaction to the tariffs, the effective tariff rate will be 16.4%, a 13.9pp increase & the highest since 1936

2/12

New @budgetlab.bsky.social tariff analysis incorporating all tariffs through Sept 3. This is a major update. We:

• incorporate higher assumptions about Canada & Mexico tariff-free import shares;

• show 2 scenarios: all tariffs & no IEEPA tariffs after Jun 2026.

In brief...

1/12

• incorporate higher assumptions about Canada & Mexico tariff-free import shares;

• show 2 scenarios: all tariffs & no IEEPA tariffs after Jun 2026.

In brief...

1/12

September 4, 2025 at 7:15 PM

New @budgetlab.bsky.social tariff analysis incorporating all tariffs through Sept 3. This is a major update. We:

• incorporate higher assumptions about Canada & Mexico tariff-free import shares;

• show 2 scenarios: all tariffs & no IEEPA tariffs after Jun 2026.

In brief...

1/12

• incorporate higher assumptions about Canada & Mexico tariff-free import shares;

• show 2 scenarios: all tariffs & no IEEPA tariffs after Jun 2026.

In brief...

1/12