Emil Verner

@emilverner.bsky.social

Financial economist at MIT Sloan working on finance, macro, international, economic history, and other fun stuff

emilverner.com

emilverner.com

Here is an interesting figure from Demirguc-Kunt et al on the adoption of deposit insurance over time across countries. US was much earlier than other countries in adopting federal deposit insurance (and some US state banking systems experimented earlier). DI is relatively recent in most countries.

December 13, 2024 at 3:46 AM

Here is an interesting figure from Demirguc-Kunt et al on the adoption of deposit insurance over time across countries. US was much earlier than other countries in adopting federal deposit insurance (and some US state banking systems experimented earlier). DI is relatively recent in most countries.

The basic message of Failing Banks, though, is that runs on solvent banks seem to be a quite rare cause of failure before DI. This was also the view at the time at the Fed/OCC. For example, the OCC bank examiners rarely cite runs as the cause of failure (even though failures many involved runs)

December 13, 2024 at 3:38 AM

The basic message of Failing Banks, though, is that runs on solvent banks seem to be a quite rare cause of failure before DI. This was also the view at the time at the Fed/OCC. For example, the OCC bank examiners rarely cite runs as the cause of failure (even though failures many involved runs)

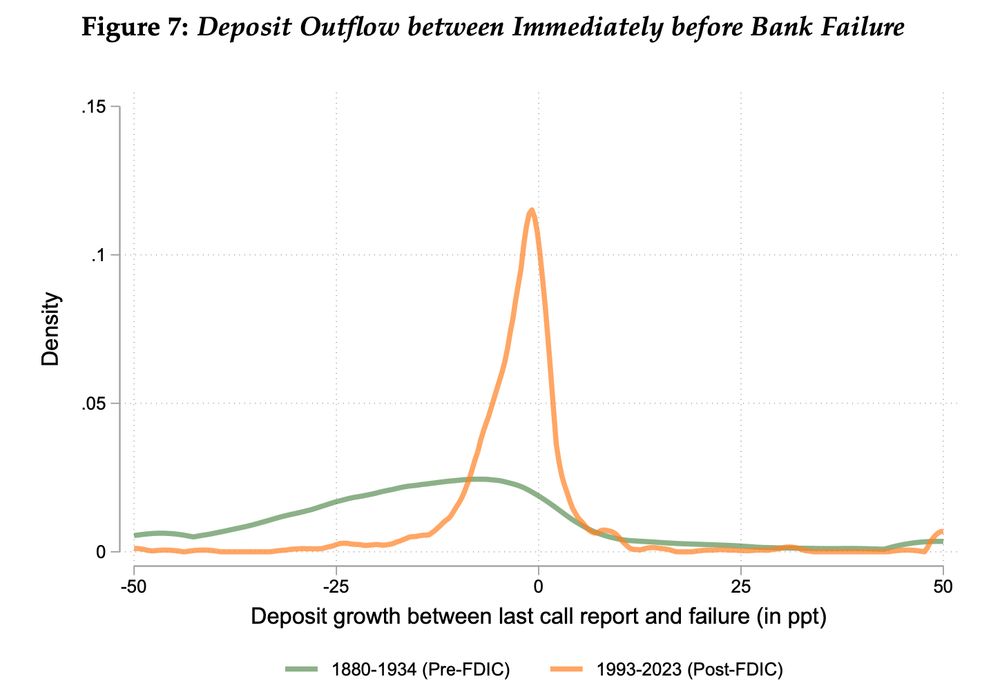

To be clear, that's not exaaaaactly what we find or claim. See figure below. But certainly our paper suggests that preventing run-induced failures of solvent banks is not an important benefit of deposit insurance (there are likely other benefits... and some costs...)

December 13, 2024 at 1:23 AM

To be clear, that's not exaaaaactly what we find or claim. See figure below. But certainly our paper suggests that preventing run-induced failures of solvent banks is not an important benefit of deposit insurance (there are likely other benefits... and some costs...)

I am less sanguine than the article above about providing unlimited deposit insurance. Insured deposits tend to flow into failing banks (see blue line below). With full insurance, there is even more onus on supervisors to close failing banks and prevent moral hazard.

November 27, 2024 at 8:58 PM

I am less sanguine than the article above about providing unlimited deposit insurance. Insured deposits tend to flow into failing banks (see blue line below). With full insurance, there is even more onus on supervisors to close failing banks and prevent moral hazard.

This is closer to depositor loss rates for historical (pre-FDIC failures), which were initially around 60 cents on the $, but fell to 30-35 cents on the $ in receivership

November 27, 2024 at 7:59 PM

This is closer to depositor loss rates for historical (pre-FDIC failures), which were initially around 60 cents on the $, but fell to 30-35 cents on the $ in receivership