Eduardo Amaral

@edugca.bsky.social

Ph.D. in Economics @PUCRioEconomia || monetary || so much to explore outside || views are only mine || tweets mostly in 🇧🇷🇵🇹

https://sites.google.com/site/edugca/

https://sites.google.com/site/edugca/

Intrigued? If you're an economist, macro-finance expert, or just fascinated by monetary puzzles, you may want to read the full paper.

It has just been published in the BIS Working Paper series.

Read it here: bis.org/publ/work1288.…

It has just been published in the BIS Working Paper series.

Read it here: bis.org/publ/work1288.…

https://bis.org/publ/work1288.…

September 24, 2025 at 2:01 AM

Intrigued? If you're an economist, macro-finance expert, or just fascinated by monetary puzzles, you may want to read the full paper.

It has just been published in the BIS Working Paper series.

Read it here: bis.org/publ/work1288.…

It has just been published in the BIS Working Paper series.

Read it here: bis.org/publ/work1288.…

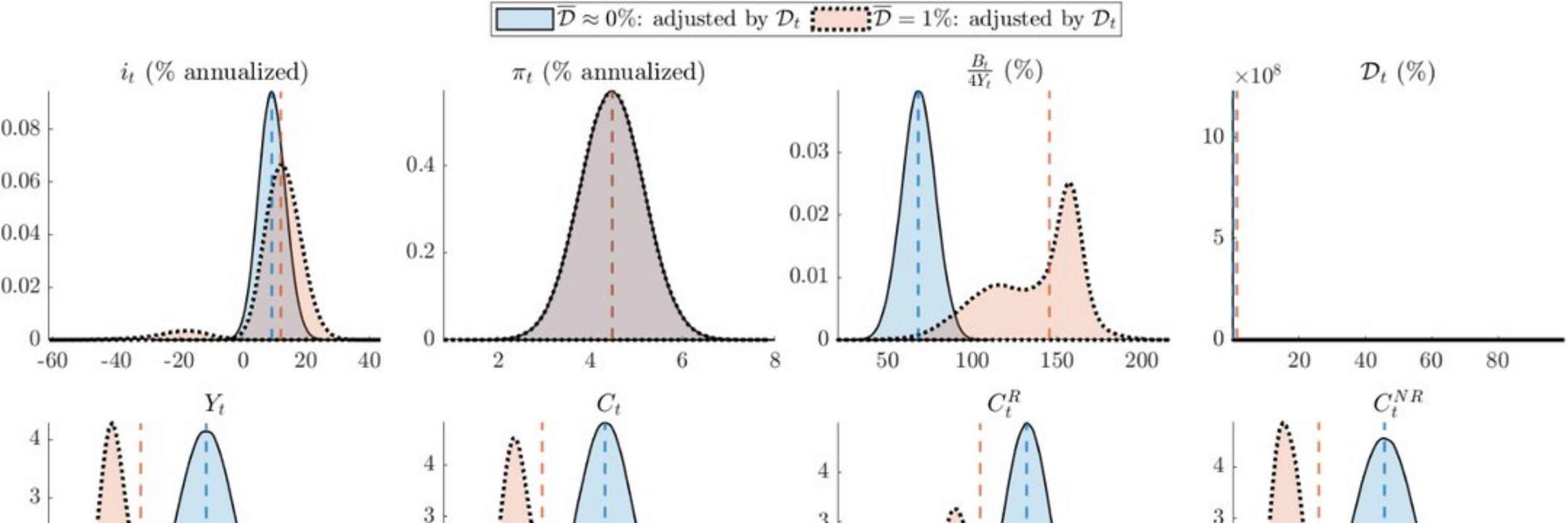

This identification problem isn't just theoretical. It has real implications for how central banks should design policy, particularly in scenarios where investment is highly vulnerable — like after financial crises, pandemics, or major trade disruptions. (9/10) #CentralBanking #FinancialMarkets

September 24, 2025 at 2:01 AM

This identification problem isn't just theoretical. It has real implications for how central banks should design policy, particularly in scenarios where investment is highly vulnerable — like after financial crises, pandemics, or major trade disruptions. (9/10) #CentralBanking #FinancialMarkets

My paper proposes a new measure of the monetary policy stance that avoids this pitfall. It works by filtering the impact of the monetary shock as if capital was fixed.

From 1965 to 2023, this new measure also enhanced inflation forecasting in the United States. 📈 (8/10)

From 1965 to 2023, this new measure also enhanced inflation forecasting in the United States. 📈 (8/10)

September 24, 2025 at 2:01 AM

My paper proposes a new measure of the monetary policy stance that avoids this pitfall. It works by filtering the impact of the monetary shock as if capital was fixed.

From 1965 to 2023, this new measure also enhanced inflation forecasting in the United States. 📈 (8/10)

From 1965 to 2023, this new measure also enhanced inflation forecasting in the United States. 📈 (8/10)

The identification puzzle creates a big problem: the classic "real interest rate gap" (r - r*) used to gauge the monetary policy stance moves in the WRONG direction.

If r falls after a hike, the gap suggests policy is easing when the central bank is actually tightening! (5

7/10) #rStar

If r falls after a hike, the gap suggests policy is easing when the central bank is actually tightening! (5

7/10) #rStar

September 24, 2025 at 2:01 AM

The identification puzzle creates a big problem: the classic "real interest rate gap" (r - r*) used to gauge the monetary policy stance moves in the WRONG direction.

If r falls after a hike, the gap suggests policy is easing when the central bank is actually tightening! (5

7/10) #rStar

If r falls after a hike, the gap suggests policy is easing when the central bank is actually tightening! (5

7/10) #rStar

The first case appears in textbooks (eg Woodford & Galí). The second case was revealed by Peter Rupert and Roman Ŝustek (2019). In my paper, in addition of explaining why it happens, I check its empirical relevance and suggest ways or circumventing it. Moreover, I propose a solution. (6/10)

September 24, 2025 at 2:01 AM

The first case appears in textbooks (eg Woodford & Galí). The second case was revealed by Peter Rupert and Roman Ŝustek (2019). In my paper, in addition of explaining why it happens, I check its empirical relevance and suggest ways or circumventing it. Moreover, I propose a solution. (6/10)

I find that the explanation for this phenomenon lies on the expected policy-reaction function of the central bank. Whenever the endogenous component of the policy rule outweighs the contractionary exogenous shock, we have that ↓ i. If it outweighs by more than Eπ ⇒ ↓r. (5/10)

September 24, 2025 at 2:01 AM

I find that the explanation for this phenomenon lies on the expected policy-reaction function of the central bank. Whenever the endogenous component of the policy rule outweighs the contractionary exogenous shock, we have that ↓ i. If it outweighs by more than Eπ ⇒ ↓r. (5/10)

The new transmission looks like this:

↑i ⇒ ↑r ⇒ ↓↓ Investment (if it is very sensitive) ⇒ ↓↓y ⇒ ↓↓π ⇒ ↓ i ⇒ ↓r

The initial hike is overwhelmed by the fall in π expectations, reversing interest rates. The real rate ends up lower, even as inflation falls! (4/10)

↑i ⇒ ↑r ⇒ ↓↓ Investment (if it is very sensitive) ⇒ ↓↓y ⇒ ↓↓π ⇒ ↓ i ⇒ ↓r

The initial hike is overwhelmed by the fall in π expectations, reversing interest rates. The real rate ends up lower, even as inflation falls! (4/10)

September 24, 2025 at 2:01 AM

The new transmission looks like this:

↑i ⇒ ↑r ⇒ ↓↓ Investment (if it is very sensitive) ⇒ ↓↓y ⇒ ↓↓π ⇒ ↓ i ⇒ ↓r

The initial hike is overwhelmed by the fall in π expectations, reversing interest rates. The real rate ends up lower, even as inflation falls! (4/10)

↑i ⇒ ↑r ⇒ ↓↓ Investment (if it is very sensitive) ⇒ ↓↓y ⇒ ↓↓π ⇒ ↓ i ⇒ ↓r

The initial hike is overwhelmed by the fall in π expectations, reversing interest rates. The real rate ends up lower, even as inflation falls! (4/10)

But what happens when we take this standard model and introduce capital and investment? Things can get weird.

In extreme scenarios, a policy rate hike can cause such a sharp drop in demand & inflation expectations that interest rates collapse. (3/10)

In extreme scenarios, a policy rate hike can cause such a sharp drop in demand & inflation expectations that interest rates collapse. (3/10)

September 24, 2025 at 2:01 AM

But what happens when we take this standard model and introduce capital and investment? Things can get weird.

In extreme scenarios, a policy rate hike can cause such a sharp drop in demand & inflation expectations that interest rates collapse. (3/10)

In extreme scenarios, a policy rate hike can cause such a sharp drop in demand & inflation expectations that interest rates collapse. (3/10)

The standard story of monetary policy is straightforward:

The Fed hikes rates (↑i) → real rates rise (↑r, if prices are sticky) → consumption falls (↓c) → output falls (↓y) → inflation falls (↓π).

It all works through higher real borrowing costs. (2/10)

The Fed hikes rates (↑i) → real rates rise (↑r, if prices are sticky) → consumption falls (↓c) → output falls (↓y) → inflation falls (↓π).

It all works through higher real borrowing costs. (2/10)

September 24, 2025 at 2:01 AM

The standard story of monetary policy is straightforward:

The Fed hikes rates (↑i) → real rates rise (↑r, if prices are sticky) → consumption falls (↓c) → output falls (↓y) → inflation falls (↓π).

It all works through higher real borrowing costs. (2/10)

The Fed hikes rates (↑i) → real rates rise (↑r, if prices are sticky) → consumption falls (↓c) → output falls (↓y) → inflation falls (↓π).

It all works through higher real borrowing costs. (2/10)

Eles mencionam o paper dele como um método de solução aproximada usando Dynare. A proposta me parece ser tornar-se mais user-friendly e com acesso a outros métodos mais precisos de solução.

September 26, 2024 at 5:05 PM

Eles mencionam o paper dele como um método de solução aproximada usando Dynare. A proposta me parece ser tornar-se mais user-friendly e com acesso a outros métodos mais precisos de solução.