David Woodruff

@dmwoodruff.bsky.social

Associate Professor of Comparative Politics, LSE. CPE, central banks, monetary history, intellectual history of social science, Karl Polanyi, Soviet economic history, complaining about neoliberalism, etc. He/him.

Bloomberg taking a shot across the bow of @zackpolanski.bsky.social — but should we listen to an economist (and Times columnist btw) whose main concern regarding Reform is its fiscal policy? www.bloomberg.com/news/article...

November 25, 2025 at 6:10 AM

Bloomberg taking a shot across the bow of @zackpolanski.bsky.social — but should we listen to an economist (and Times columnist btw) whose main concern regarding Reform is its fiscal policy? www.bloomberg.com/news/article...

Despite planning to continue paying the banks 3 x more in interest on reserves than they pay in corporate and related taxes, Reeves is reduced to begging the banks for PR help to sell her budget. on.ft.com/4iDbqqB

November 24, 2025 at 10:39 PM

Despite planning to continue paying the banks 3 x more in interest on reserves than they pay in corporate and related taxes, Reeves is reduced to begging the banks for PR help to sell her budget. on.ft.com/4iDbqqB

This gives context to this proposal, which would significantly improve progressively.

November 12, 2025 at 3:34 PM

This gives context to this proposal, which would significantly improve progressively.

TIL that employee contributions to UK national insurance are ludicrously regressive: rate goes down from 8% to 2% on income > £50,270. And it's getting even worse: threshold is infrequently updated & would be nearly £10000 higher if adjusted for post-Covid inflation.

November 12, 2025 at 3:09 PM

TIL that employee contributions to UK national insurance are ludicrously regressive: rate goes down from 8% to 2% on income > £50,270. And it's getting even worse: threshold is infrequently updated & would be nearly £10000 higher if adjusted for post-Covid inflation.

Over the last 11 financial years, the UK Treasury has spent more on paying interest to the banking sector on their reserves than it has taken in from them in corporate and sector-specific taxes. In 2024-25, it paid over 3 times as much for interest on reserves as it received from taxes on banks.

November 12, 2025 at 9:30 AM

Over the last 11 financial years, the UK Treasury has spent more on paying interest to the banking sector on their reserves than it has taken in from them in corporate and sector-specific taxes. In 2024-25, it paid over 3 times as much for interest on reserves as it received from taxes on banks.

An outstanding policy analysis, but should be made more general: *any* business that has a return on equity < 10% automatically gets a tax adjustment so it reaches that level. Also, the magic of the market requires businesses have absolute freedom on salaries and bonuses.

November 4, 2025 at 1:07 PM

An outstanding policy analysis, but should be made more general: *any* business that has a return on equity < 10% automatically gets a tax adjustment so it reaches that level. Also, the magic of the market requires businesses have absolute freedom on salaries and bonuses.

Some Threadneedle-ologists say BoE will hold rates this week and wait to see how budget looks. To act on this reasoning would contradict long-stated, albeit entirely arbitrary, policy, which implies implausibly assuming government makes no change.

November 3, 2025 at 10:13 AM

Some Threadneedle-ologists say BoE will hold rates this week and wait to see how budget looks. To act on this reasoning would contradict long-stated, albeit entirely arbitrary, policy, which implies implausibly assuming government makes no change.

In case you don’t speak central banker, here’s BoE chief economist Huw Pill saying QT should be a club to force austerity on govt. Nary a reference to a BoE mandate in the speech! www.bankofengland.co.uk/speech/2025/...

September 23, 2025 at 12:51 PM

In case you don’t speak central banker, here’s BoE chief economist Huw Pill saying QT should be a club to force austerity on govt. Nary a reference to a BoE mandate in the speech! www.bankofengland.co.uk/speech/2025/...

The official line from the BoE on this is that the pace at which their portfolio would shrink if all gilts were held to maturity would be too slow. What counts as fast enough has never been specified. So far about 2/3s of QT has been from maturing gilts.

September 19, 2025 at 11:11 PM

The official line from the BoE on this is that the pace at which their portfolio would shrink if all gilts were held to maturity would be too slow. What counts as fast enough has never been specified. So far about 2/3s of QT has been from maturing gilts.

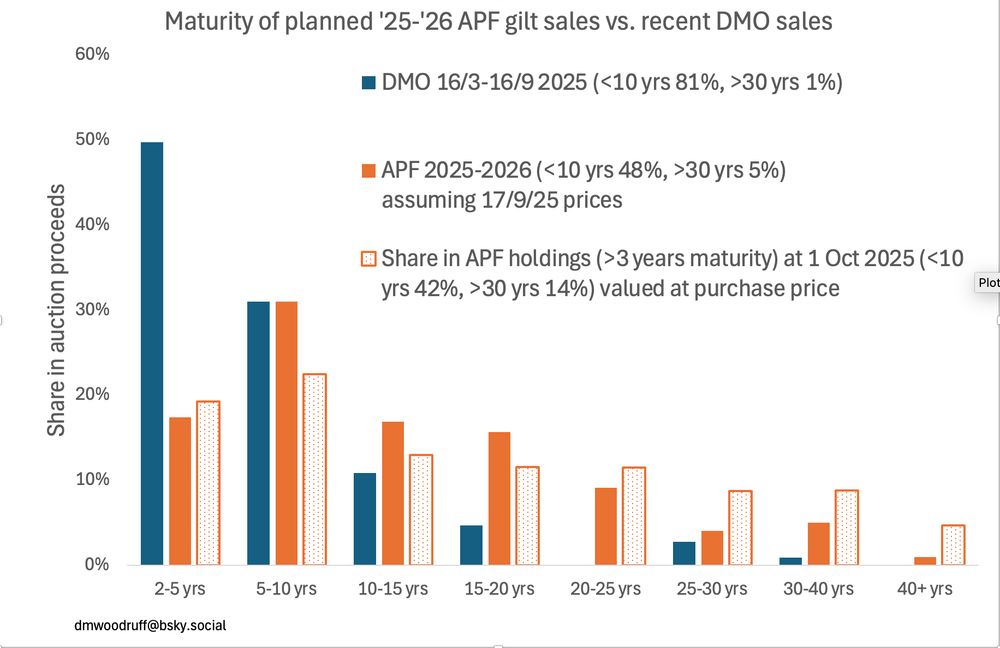

A more detailed breakdown by maturity.

September 18, 2025 at 3:04 PM

A more detailed breakdown by maturity.

The BoE responded to market concerns on APF sales of long-dated gilts by shifting to shorter-dated ones. Still will not be following Treasury/DMO issue policy, which is much more geared to short-dated gilts. Note that APF doesn't sell any gilts with <3 years to maturity.

September 18, 2025 at 2:59 PM

The BoE responded to market concerns on APF sales of long-dated gilts by shifting to shorter-dated ones. Still will not be following Treasury/DMO issue policy, which is much more geared to short-dated gilts. Note that APF doesn't sell any gilts with <3 years to maturity.

Good piece from Alphaville on likely scale of next year's QT. Threadneedle-ologists starting to remind me of Kremlinologists. Here's some figures on the fiscal effects of possible QT size decisions, assuming current gilt prices.

www.ft.com/content/96e6...

www.ft.com/content/96e6...

September 15, 2025 at 4:08 PM

Good piece from Alphaville on likely scale of next year's QT. Threadneedle-ologists starting to remind me of Kremlinologists. Here's some figures on the fiscal effects of possible QT size decisions, assuming current gilt prices.

www.ft.com/content/96e6...

www.ft.com/content/96e6...

How would changing the pace of QT affect the fiscal rules? The table compares 3 scenarios: an unchanged pace, a pace adjusted to reduce active sales to last year's level, or a shift to passive-only QT for the coming year. Maintaining the current pace would save £880 mln/year in interest costs.

September 15, 2025 at 3:30 PM

How would changing the pace of QT affect the fiscal rules? The table compares 3 scenarios: an unchanged pace, a pace adjusted to reduce active sales to last year's level, or a shift to passive-only QT for the coming year. Maintaining the current pace would save £880 mln/year in interest costs.

This white van ad illuminates a UK fiscal rule accounting issue important for understanding significance of looming BoE QT decision. If buyers are offered a discount for paying deposit and interest, they can choose lower payments&higher indebtedness or a cheaper boiler. Savvy+liquid buyer… 1/3

September 2, 2025 at 2:05 PM

This white van ad illuminates a UK fiscal rule accounting issue important for understanding significance of looming BoE QT decision. If buyers are offered a discount for paying deposit and interest, they can choose lower payments&higher indebtedness or a cheaper boiler. Savvy+liquid buyer… 1/3

This white van ad illuminates a UK fiscal rule accounting issue important for understanding significance of looming BoE QT decision. If buyers are offered a discount for paying deposit and interest, they can choose lower payments&higher indebtedness or a cheaper boiler. Savvy+liquid buyer… 1/3

September 2, 2025 at 1:59 PM

This white van ad illuminates a UK fiscal rule accounting issue important for understanding significance of looming BoE QT decision. If buyers are offered a discount for paying deposit and interest, they can choose lower payments&higher indebtedness or a cheaper boiler. Savvy+liquid buyer… 1/3

Did you know that the Bank of England promised to give the Debt Management Office a voice in determining the terms of quantitative tightening? Here's Governor Mervyn King before the Treasury Committee in March 2009. Thread offers minimal and radical ways to implement this promise.

August 25, 2025 at 4:20 PM

Did you know that the Bank of England promised to give the Debt Management Office a voice in determining the terms of quantitative tightening? Here's Governor Mervyn King before the Treasury Committee in March 2009. Thread offers minimal and radical ways to implement this promise.

In Norwich UK. Read it years ago in the US but it made me happy to see it.

August 2, 2025 at 2:11 PM

In Norwich UK. Read it years ago in the US but it made me happy to see it.

Pigou wept. Must-read piece on AI infrastructure.

ig.ft.com/ai-data-cent...

ig.ft.com/ai-data-cent...

July 31, 2025 at 10:25 AM

Pigou wept. Must-read piece on AI infrastructure.

ig.ft.com/ai-data-cent...

ig.ft.com/ai-data-cent...

Lending based on readily fungible collateral has serious negative externalities and should not be a presumptive right. Thank you for coming to my TED talk.

July 27, 2025 at 11:22 AM

Lending based on readily fungible collateral has serious negative externalities and should not be a presumptive right. Thank you for coming to my TED talk.

Lohmann’s ‘audience cost’ theory of central bank independence has held up for almost six months since the inauguration, which is pretty good for this crazed era.

July 16, 2025 at 4:55 PM

Lohmann’s ‘audience cost’ theory of central bank independence has held up for almost six months since the inauguration, which is pretty good for this crazed era.

A key passage from Lohmann. Source in next post. 2/3

April 22, 2025 at 12:30 PM

A key passage from Lohmann. Source in next post. 2/3

Calls for some Schumpeter. Nobody plays bridge anymore but substitute fantasy football, etc.

April 4, 2025 at 6:58 AM

Calls for some Schumpeter. Nobody plays bridge anymore but substitute fantasy football, etc.

Harvard trying to bargain is pointless. The Trumpists want to see it in the wood chipper. See Vance’s favorite political philosopher (Yarvin) below. Throwing its considerable resources into legal battle and collective action on behalf of universities and science is Harvard’s only practical option.

April 1, 2025 at 2:09 AM

Harvard trying to bargain is pointless. The Trumpists want to see it in the wood chipper. See Vance’s favorite political philosopher (Yarvin) below. Throwing its considerable resources into legal battle and collective action on behalf of universities and science is Harvard’s only practical option.

Labour wants to be the mirror image of their mythological version of Truss 2022—ie Brown in 1998 doing ‘prudence with a purpose’. All will be good once it appeases the bond market gods Truss flouted. But there might have been some external factors at work for Brown…

March 22, 2025 at 2:36 PM

Labour wants to be the mirror image of their mythological version of Truss 2022—ie Brown in 1998 doing ‘prudence with a purpose’. All will be good once it appeases the bond market gods Truss flouted. But there might have been some external factors at work for Brown…