Dan Herbst

@danherbst.bsky.social

Econ Prof at University of Arizona. Interested in labor, public, & household finance. Also a fan of dogs & motorcycles. www.danjherbst.com

15/ For more, check out...

The @oppinsights.bsky.social WP: opportunityinsights.org/paper/credi...

Our non-technical summary: opportunityinsights.org/wp-content/...

And watch Nathan present LIVE TODAY at 10:45AM ET in the @NBER.org SI Household Finance session!

www.youtube.com/@NBERvideos...

The @oppinsights.bsky.social WP: opportunityinsights.org/paper/credi...

Our non-technical summary: opportunityinsights.org/wp-content/...

And watch Nathan present LIVE TODAY at 10:45AM ET in the @NBER.org SI Household Finance session!

www.youtube.com/@NBERvideos...

NBER

The National Bureau of Economic Research (NBER) is a private, nonprofit, nonpartisan organization that facilitates cutting-edge investigation and analysis of major economic issues. It disseminates research findings to academics, public and private-sector decisionmakers, and the public by posting more than 1,200 working papers, and convening more than 120 scholarly conferences, each year.

Headquartered in Cambridge, MA, the NBER is a network of more than 1,700 economists who hold primary appointments at North American colleges and universities. These researchers are leaders in the field: 47 current or former NBER affiliates and board members have been awarded the Nobel Prize in Economics, and 13 have chaired the President’s Council of Economic Advisers.

The NBER is committed to making its content accessible to all. Address any concerns or requests for assistance to webaccessibility@nber.org. To request a video you are featured in be taken down, reach out to webmaster@nber.org.

www.youtube.com

July 17, 2025 at 1:17 PM

15/ For more, check out...

The @oppinsights.bsky.social WP: opportunityinsights.org/paper/credi...

Our non-technical summary: opportunityinsights.org/wp-content/...

And watch Nathan present LIVE TODAY at 10:45AM ET in the @NBER.org SI Household Finance session!

www.youtube.com/@NBERvideos...

The @oppinsights.bsky.social WP: opportunityinsights.org/paper/credi...

Our non-technical summary: opportunityinsights.org/wp-content/...

And watch Nathan present LIVE TODAY at 10:45AM ET in the @NBER.org SI Household Finance session!

www.youtube.com/@NBERvideos...

14/ In sum, our paper documents large differences in credit access by race, class, and hometown. These differences appear driven not by algorithmic bias or resource constraints but by early-life repayment that's rooted in childhood environments.

July 17, 2025 at 1:17 PM

14/ In sum, our paper documents large differences in credit access by race, class, and hometown. These differences appear driven not by algorithmic bias or resource constraints but by early-life repayment that's rooted in childhood environments.

13/ Why do childhood environments matter so much? Survey evidence points to several mechanisms, including differences in social capital, financial literacy, and informal credit networks. Future research might explore how early credit experiences are shaped through these channels.

July 17, 2025 at 1:17 PM

13/ Why do childhood environments matter so much? Survey evidence points to several mechanisms, including differences in social capital, financial literacy, and informal credit networks. Future research might explore how early credit experiences are shaped through these channels.

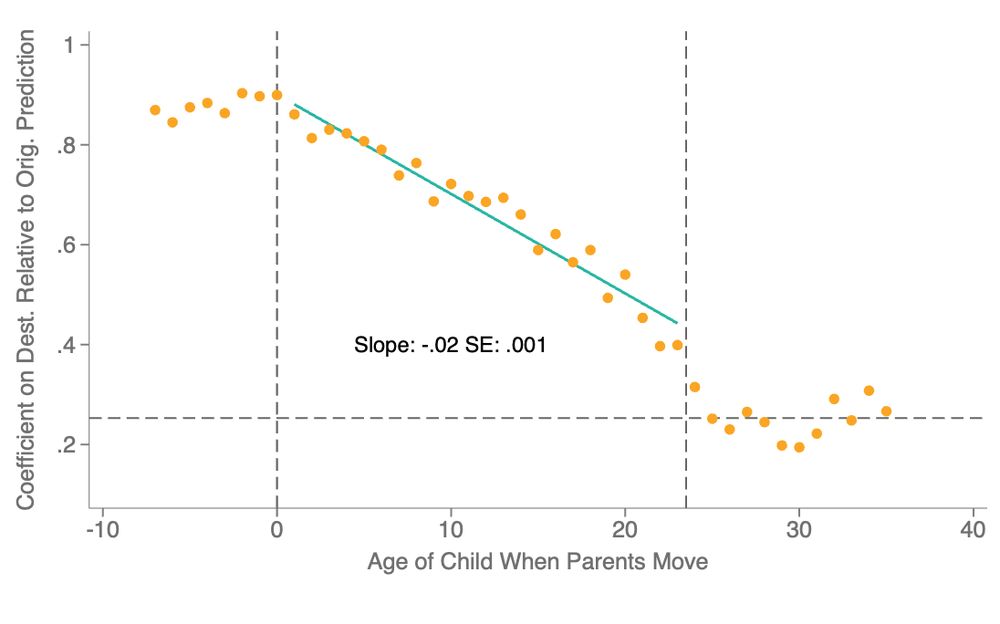

12/ We also find causal evidence place-based effects on repayment: using a mover's design, we find that childhood exposure to places with better repayment behaviors leads to lower delinquency rates in adulthood, even conditional on adult income.

July 17, 2025 at 1:17 PM

12/ We also find causal evidence place-based effects on repayment: using a mover's design, we find that childhood exposure to places with better repayment behaviors leads to lower delinquency rates in adulthood, even conditional on adult income.

11/ Instead, we find that childhood factors play a role--the credit scores of your parents and childhood neighbors predict your later-life repayment, even conditional on income, wealth, and education.

July 17, 2025 at 1:17 PM

11/ Instead, we find that childhood factors play a role--the credit scores of your parents and childhood neighbors predict your later-life repayment, even conditional on income, wealth, and education.

10/ Do differences in financial resources explain repayment gaps by race, class, and hometown? Not by much. Repayment gaps persist among individuals with the same income, wealth, marital status, job stability, and employer.

July 17, 2025 at 1:17 PM

10/ Do differences in financial resources explain repayment gaps by race, class, and hometown? Not by much. Repayment gaps persist among individuals with the same income, wealth, marital status, job stability, and employer.

9/ Since credit scores predict future delinquency, the key to removing either type of bias and expanding credit access is to understand why some groups fall delinquent more often than others, especially in early adulthood.

July 17, 2025 at 1:17 PM

9/ Since credit scores predict future delinquency, the key to removing either type of bias and expanding credit access is to understand why some groups fall delinquent more often than others, especially in early adulthood.

8/ But when it comes to *balance* bias, the answer is yes: among those who end up avoiding delinquency, Black individuals and those from low-income backgrounds received lower initial scores than other groups.

July 17, 2025 at 1:17 PM

8/ But when it comes to *balance* bias, the answer is yes: among those who end up avoiding delinquency, Black individuals and those from low-income backgrounds received lower initial scores than other groups.

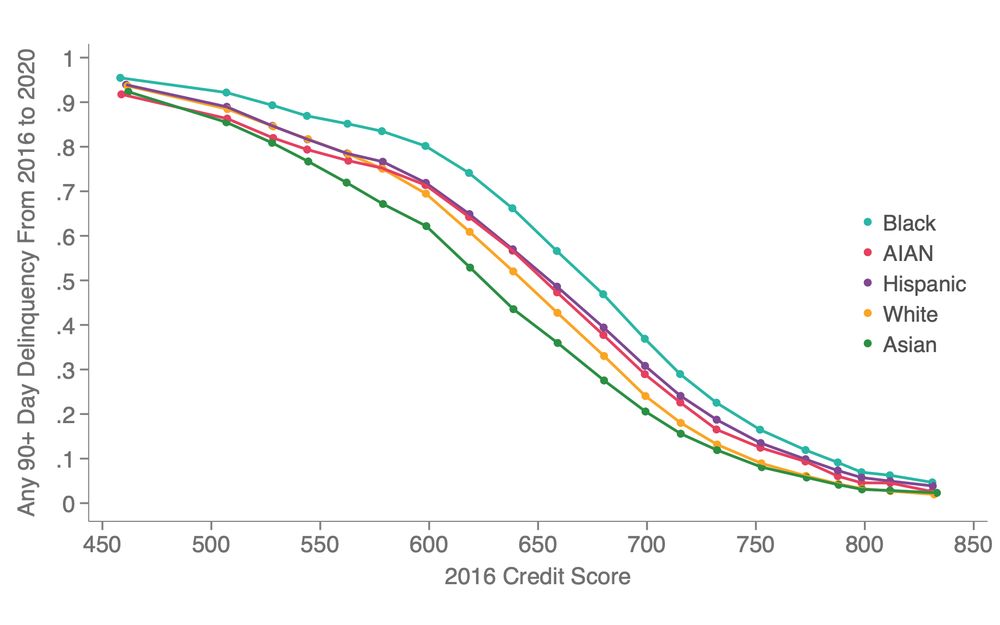

7/ When it comes to *calibration* bias, the answer is no: Among those with a given credit score, Black individuals or those from low-income backgrounds actually fall delinquent at higher rates than other groups. In other words, the credit-score gap understates the repayment gap.

July 17, 2025 at 1:17 PM

7/ When it comes to *calibration* bias, the answer is no: Among those with a given credit score, Black individuals or those from low-income backgrounds actually fall delinquent at higher rates than other groups. In other words, the credit-score gap understates the repayment gap.

6/ Are credit scores simply biased against Black individuals or those from low-income backgrounds? The answer depends on how you define "bias."

July 17, 2025 at 1:17 PM

6/ Are credit scores simply biased against Black individuals or those from low-income backgrounds? The answer depends on how you define "bias."

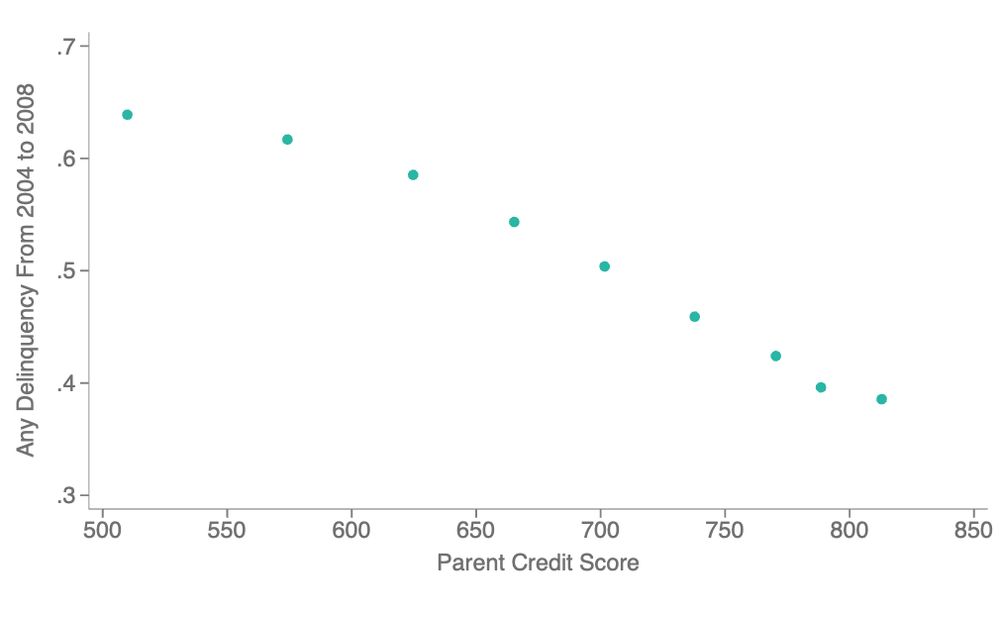

5/ These differences emerge at early ages and reflect real constraints on borrowing: groups with lower scores also have smaller credit balances, higher credit card utilization, and rely more on high-cost alternative financial products like payday loans.

July 17, 2025 at 1:17 PM

5/ These differences emerge at early ages and reflect real constraints on borrowing: groups with lower scores also have smaller credit balances, higher credit card utilization, and rely more on high-cost alternative financial products like payday loans.

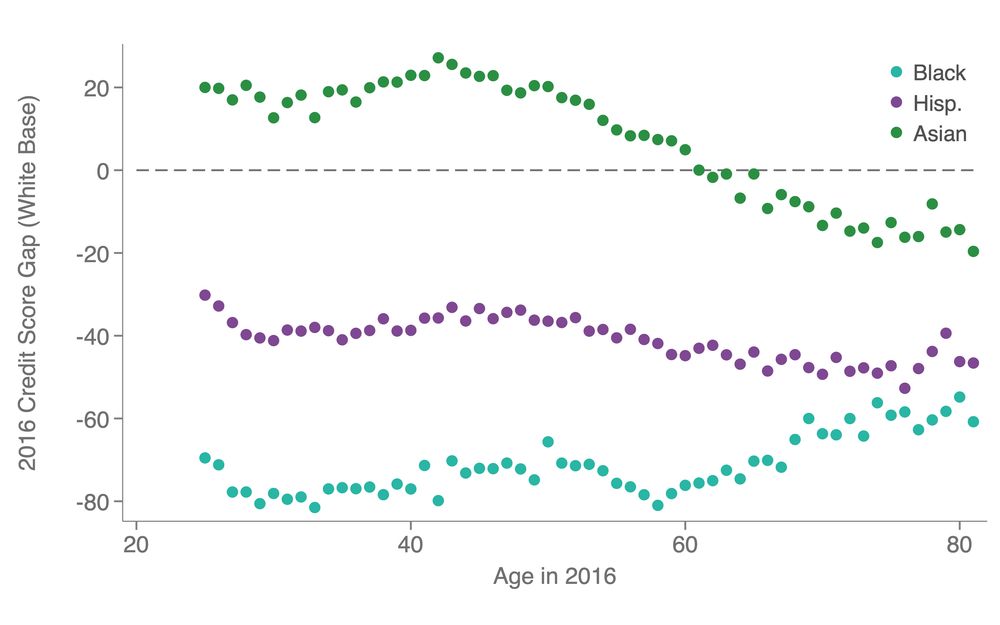

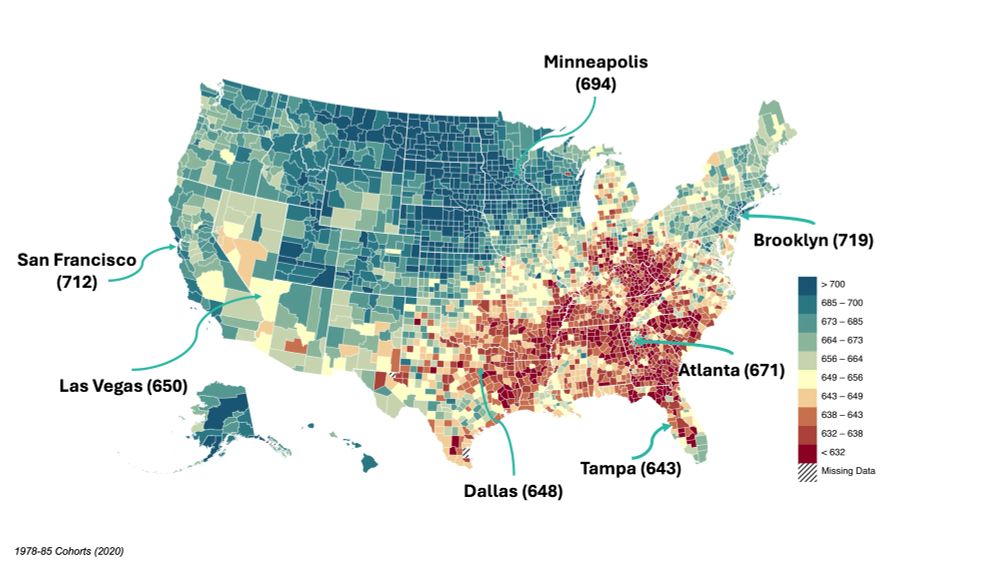

4/ We also see large differences by hometown. For example, by the time they're adults, low-income White children from Brooklyn, NY have 90-point higher average credit scores than low-income White children from Indianapolis.

July 17, 2025 at 1:17 PM

4/ We also see large differences by hometown. For example, by the time they're adults, low-income White children from Brooklyn, NY have 90-point higher average credit scores than low-income White children from Indianapolis.

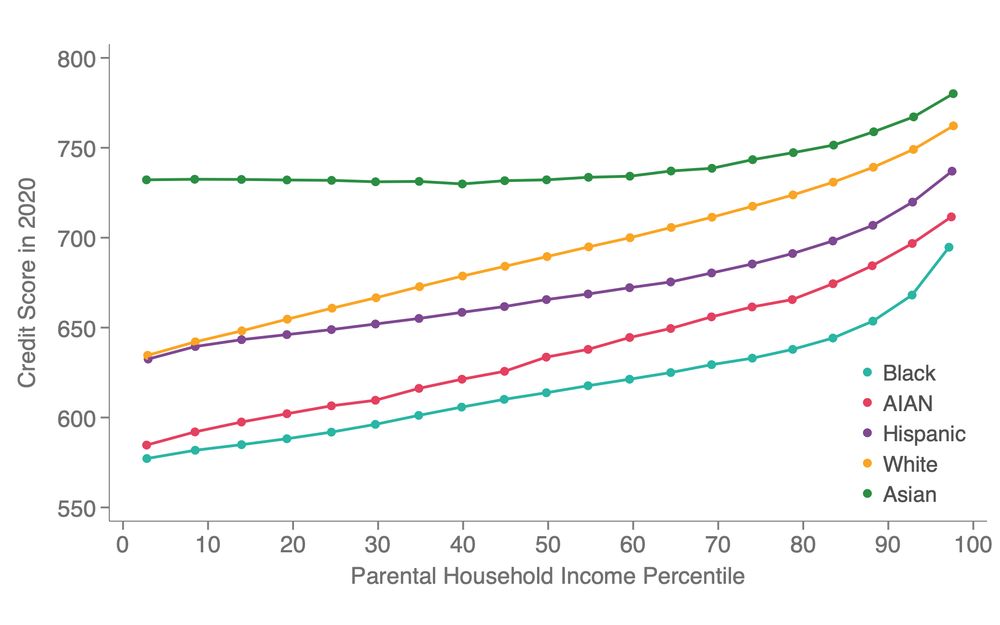

3/ Black individuals and those born to low-income parents have much lower credit scores than other groups. For example, Black individuals from the 90th pctile of parent income have similar average credit scores as White individuals from the 25th pctile.

July 17, 2025 at 1:17 PM

3/ Black individuals and those born to low-income parents have much lower credit scores than other groups. For example, Black individuals from the 90th pctile of parent income have similar average credit scores as White individuals from the 25th pctile.

2/ Whether buying a home, building wealth, or managing sudden expenses, affordable credit can be a powerful tool for upward mobility. But our data show how access to this tool is limited for many groups.

Consider credit scores—a metric lenders use to judge creditworthiness...

Consider credit scores—a metric lenders use to judge creditworthiness...

July 17, 2025 at 1:17 PM

2/ Whether buying a home, building wealth, or managing sudden expenses, affordable credit can be a powerful tool for upward mobility. But our data show how access to this tool is limited for many groups.

Consider credit scores—a metric lenders use to judge creditworthiness...

Consider credit scores—a metric lenders use to judge creditworthiness...

Thanks!

And thanks for the thoughtful feedback! The comments are much appreciated :)

And thanks for the thoughtful feedback! The comments are much appreciated :)

December 12, 2024 at 5:23 AM

Thanks!

And thanks for the thoughtful feedback! The comments are much appreciated :)

And thanks for the thoughtful feedback! The comments are much appreciated :)

Yeah it would add cost and complicate recruitment (which mentions the piece-rate option). At the time, I didn't think an hourly conrol group would be worth the trouble because I thought the highest wage offers would get close to complete take-up. In hindsight it might have been a good idea!

December 12, 2024 at 5:21 AM

Yeah it would add cost and complicate recruitment (which mentions the piece-rate option). At the time, I didn't think an hourly conrol group would be worth the trouble because I thought the highest wage offers would get close to complete take-up. In hindsight it might have been a good idea!

You're absolutely right--there are a variety of factors apart from moral hazard and adverse selection that influence payment schemes. I mention monitoring costs, but I should delve into behavioral mechanisms like Falk & Kosfeld as well. There's a lot of great work I'm building on here.

December 12, 2024 at 5:20 AM

You're absolutely right--there are a variety of factors apart from moral hazard and adverse selection that influence payment schemes. I mention monitoring costs, but I should delve into behavioral mechanisms like Falk & Kosfeld as well. There's a lot of great work I'm building on here.

I'd love to add other dimensions of variation, but unfortunately cost is a very real constraint right now. I'm definitely looking to things like this in the future if those constraints are lifted!

December 12, 2024 at 5:19 AM

I'd love to add other dimensions of variation, but unfortunately cost is a very real constraint right now. I'm definitely looking to things like this in the future if those constraints are lifted!

Yeah, I tried to make it as generalizable as possible—participants don't know they're in an experiment, data-entry required in many jobs, etc. But I can't claim my estimates would extrapolate different tasks or labor markets (in fairness, neither can most other studies of labor productivity.)

December 12, 2024 at 5:19 AM

Yeah, I tried to make it as generalizable as possible—participants don't know they're in an experiment, data-entry required in many jobs, etc. But I can't claim my estimates would extrapolate different tasks or labor markets (in fairness, neither can most other studies of labor productivity.)