Adrianna McIntyre

@adrianna.bsky.social

Assistant Professor of Health Policy and Politics at @hsph.harvard.edu

I study how administrative burdens impede health insurance coverage, strategies to reduce these barriers, and the politics of health reform

she/her/Michigander

I study how administrative burdens impede health insurance coverage, strategies to reduce these barriers, and the politics of health reform

she/her/Michigander

awww. gave Nellie some extra bedtime pats in honor of George

November 11, 2025 at 4:45 AM

awww. gave Nellie some extra bedtime pats in honor of George

omg!

fortunately Nellie is like half the size of George (between 37 and 40lbs, depending on how much coaxing has been going on)

fortunately Nellie is like half the size of George (between 37 and 40lbs, depending on how much coaxing has been going on)

November 11, 2025 at 4:25 AM

omg!

fortunately Nellie is like half the size of George (between 37 and 40lbs, depending on how much coaxing has been going on)

fortunately Nellie is like half the size of George (between 37 and 40lbs, depending on how much coaxing has been going on)

(second half after the landing? totally fine. other stairs? also fine!)

November 11, 2025 at 2:07 AM

(second half after the landing? totally fine. other stairs? also fine!)

I love this paper because it shattered my priors: I assumed HDHPs were materially bad for low-income folks with limited liquidity, but also that they probably "worked" to some extent for people who are wealthy and savvy (people who see HSAs as retirement savings vehicles).

I was wrong!

/fin

I was wrong!

/fin

As the ~discourse~ seems to bend interminably towards Republicans trying to figure out how they can (further) HDHP-ify ACA coverage, it's worth revisiting what is probably our best (most rigorous) study on the effect of deductibles in health insurance.

academic.oup.com/qje/article-...

academic.oup.com/qje/article-...

November 10, 2025 at 10:27 PM

I love this paper because it shattered my priors: I assumed HDHPs were materially bad for low-income folks with limited liquidity, but also that they probably "worked" to some extent for people who are wealthy and savvy (people who see HSAs as retirement savings vehicles).

I was wrong!

/fin

I was wrong!

/fin

In this best-case scenario for HDHPs, the authors "find no evidence of consumers learning to price shop after two years in high-deductible coverage" and that "consumers did not shift to cheaper providers, in either of the two years we observe post-switch"

November 10, 2025 at 10:22 PM

In this best-case scenario for HDHPs, the authors "find no evidence of consumers learning to price shop after two years in high-deductible coverage" and that "consumers did not shift to cheaper providers, in either of the two years we observe post-switch"

The authors also find that "a meaningful portion of all spending reductions came from well-off consumers who were predictably sick" — again, despite (1) HSAs being pre-funded to a level sufficient to cover the deductible in the first year and (2) most employees still being under the deductible level

November 10, 2025 at 10:16 PM

The authors also find that "a meaningful portion of all spending reductions came from well-off consumers who were predictably sick" — again, despite (1) HSAs being pre-funded to a level sufficient to cover the deductible in the first year and (2) most employees still being under the deductible level

The authors find that the entirety of reduced spending — because HDHPs *do* reduce spending — came entirely from people seeking less care.

They weren't adept at distinguishing "high" and "low" value care; they scaled back all forms of care.

They weren't adept at distinguishing "high" and "low" value care; they scaled back all forms of care.

November 10, 2025 at 10:11 PM

The authors find that the entirety of reduced spending — because HDHPs *do* reduce spending — came entirely from people seeking less care.

They weren't adept at distinguishing "high" and "low" value care; they scaled back all forms of care.

They weren't adept at distinguishing "high" and "low" value care; they scaled back all forms of care.

In other words, the deck is as stacked in favor of HDHPs achieving their proposed ends — prudent price shopping, encouraging lower-cost drugs and procedures over higher-cost alternatives, elevation of necessary and appropriate care over "low-value" or "wasteful" care — as they could be.

And yet.

And yet.

November 10, 2025 at 10:06 PM

In other words, the deck is as stacked in favor of HDHPs achieving their proposed ends — prudent price shopping, encouraging lower-cost drugs and procedures over higher-cost alternatives, elevation of necessary and appropriate care over "low-value" or "wasteful" care — as they could be.

And yet.

And yet.

And this employees are "almost exclusively college educated and technologically savvy"

The authors describe this as "close to a best-case scenario for the ability of consumers to (i) use technology in support of health care decisions and (ii) understand complex aspects of insurance contract"

The authors describe this as "close to a best-case scenario for the ability of consumers to (i) use technology in support of health care decisions and (ii) understand complex aspects of insurance contract"

November 10, 2025 at 10:02 PM

And this employees are "almost exclusively college educated and technologically savvy"

The authors describe this as "close to a best-case scenario for the ability of consumers to (i) use technology in support of health care decisions and (ii) understand complex aspects of insurance contract"

The authors describe this as "close to a best-case scenario for the ability of consumers to (i) use technology in support of health care decisions and (ii) understand complex aspects of insurance contract"

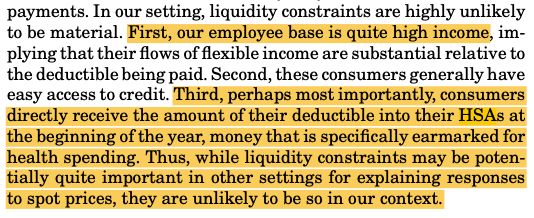

Before getting to the findings, two key facts about the study context:

1. Employees were high-income; fewer than 10% had incomes under $100K and more than a quarter had incomes over $150K (this is employee income, not household)

2. HSAs were *pre-funded* to the deductible level

1. Employees were high-income; fewer than 10% had incomes under $100K and more than a quarter had incomes over $150K (this is employee income, not household)

2. HSAs were *pre-funded* to the deductible level

November 10, 2025 at 9:57 PM

Before getting to the findings, two key facts about the study context:

1. Employees were high-income; fewer than 10% had incomes under $100K and more than a quarter had incomes over $150K (this is employee income, not household)

2. HSAs were *pre-funded* to the deductible level

1. Employees were high-income; fewer than 10% had incomes under $100K and more than a quarter had incomes over $150K (this is employee income, not household)

2. HSAs were *pre-funded* to the deductible level

HSAs are similar, in that evidence finds they're fairly abysmal health policy — deductibles scare people off care *even w/HSAs pre-funded to the deductible level* — but they're *phenomenal* retirement savings vehicles for those healthy & wealthy enough to foot OOP (or, catastrophically, MOOP) costs

November 10, 2025 at 9:46 PM

HSAs are similar, in that evidence finds they're fairly abysmal health policy — deductibles scare people off care *even w/HSAs pre-funded to the deductible level* — but they're *phenomenal* retirement savings vehicles for those healthy & wealthy enough to foot OOP (or, catastrophically, MOOP) costs

Reposted by Adrianna McIntyre

Sorry, correction, HRA actually stands for health reimbursement *arrangement*

Health policy acronyms come for us all.

Health policy acronyms come for us all.

November 10, 2025 at 9:31 PM

Sorry, correction, HRA actually stands for health reimbursement *arrangement*

Health policy acronyms come for us all.

Health policy acronyms come for us all.

We're at "concepts of concepts" at best

November 10, 2025 at 9:23 PM

We're at "concepts of concepts" at best

And a third possibility is that they actually mean some sort of new individual health reimbursement account (HRA), not HSAs.

My point is, if Republicans don't actually know what acronym they're planning to use, maybe news outlets shouldn't be credulous about Republicans having a "plan."

My point is, if Republicans don't actually know what acronym they're planning to use, maybe news outlets shouldn't be credulous about Republicans having a "plan."

This is neither here nor there, but the distinction between a FSA and a HSA is actually pretty monumental — FSAs are use-it-or-lose-it, HSAs are not — and I don't think we actually know which one Trump(/Rick Scott/Bill Cassidy) is talking about in his new concepts of a plan

November 10, 2025 at 9:22 PM

And a third possibility is that they actually mean some sort of new individual health reimbursement account (HRA), not HSAs.

My point is, if Republicans don't actually know what acronym they're planning to use, maybe news outlets shouldn't be credulous about Republicans having a "plan."

My point is, if Republicans don't actually know what acronym they're planning to use, maybe news outlets shouldn't be credulous about Republicans having a "plan."

I talk about these as sepatate "front door" (problems at application that keep eligible people from enrolling) and "side door" (problems at renewal that lead to avoidable coverage loss and churn) problems.

They're related, but because the policies/frictions differ, they require tailored solutions.

They're related, but because the policies/frictions differ, they require tailored solutions.

n.b. The statutory text is substantially less flexible on the timeframe for work activity at application; to meet the at-application requirement, prospective enrollees need to have at least been working in the prior month (and states can require up to three months of consecutive work).

November 10, 2025 at 4:34 PM

I talk about these as sepatate "front door" (problems at application that keep eligible people from enrolling) and "side door" (problems at renewal that lead to avoidable coverage loss and churn) problems.

They're related, but because the policies/frictions differ, they require tailored solutions.

They're related, but because the policies/frictions differ, they require tailored solutions.

n.b. The statutory text is substantially less flexible on the timeframe for work activity at application; to meet the at-application requirement, prospective enrollees need to have at least been working in the prior month (and states can require up to three months of consecutive work).

November 10, 2025 at 4:31 PM

n.b. The statutory text is substantially less flexible on the timeframe for work activity at application; to meet the at-application requirement, prospective enrollees need to have at least been working in the prior month (and states can require up to three months of consecutive work).

States will have an easier time automating this if they're comfortable using the most flexible interpretation of this requirement and using data that is 4-5 months old, rather than insisting on "prior month" data, simply because state wage databases take time to make data available.

November 10, 2025 at 4:29 PM

States will have an easier time automating this if they're comfortable using the most flexible interpretation of this requirement and using data that is 4-5 months old, rather than insisting on "prior month" data, simply because state wage databases take time to make data available.