Giuseppe Cavaliere

@cavalieregiu.bsky.social

Professor of #Econometrics @Unibo & @UniofExeter. Co-Editor of @JEconometrics. Dadx2, ECMAx4. Tireless traveler.

** 𝐓𝐢𝐦𝐞 𝐒𝐞𝐫𝐢𝐞𝐬 𝐌𝐨𝐝𝐞𝐥𝐬 𝐟𝐨𝐫 𝐃𝐮𝐫𝐚𝐭𝐢𝐨𝐧 𝐃𝐚𝐭𝐚 **

Happy to share that our joint paper with Thomas Mikosch, Anders Rahbek, and Frederik Vilandt on statistical inference (and unit roots) in ACD models is forthcoming in the 𝗝𝗼𝘂𝗿𝗻𝗮𝗹 𝗼𝗳 𝘁𝗵𝗲 𝗥𝗼𝘆𝗮𝗹 𝗦𝘁𝗮𝘁𝗶𝘀𝘁𝗶𝗰𝗮𝗹 𝗦𝗼𝗰𝗶𝗲𝘁𝘆: 𝗦𝗲𝗿𝗶𝗲𝘀 𝗕!

ideas.repec.org/p/arx/papers...

Happy to share that our joint paper with Thomas Mikosch, Anders Rahbek, and Frederik Vilandt on statistical inference (and unit roots) in ACD models is forthcoming in the 𝗝𝗼𝘂𝗿𝗻𝗮𝗹 𝗼𝗳 𝘁𝗵𝗲 𝗥𝗼𝘆𝗮𝗹 𝗦𝘁𝗮𝘁𝗶𝘀𝘁𝗶𝗰𝗮𝗹 𝗦𝗼𝗰𝗶𝗲𝘁𝘆: 𝗦𝗲𝗿𝗶𝗲𝘀 𝗕!

ideas.repec.org/p/arx/papers...

February 13, 2026 at 9:52 AM

** 𝐓𝐢𝐦𝐞 𝐒𝐞𝐫𝐢𝐞𝐬 𝐌𝐨𝐝𝐞𝐥𝐬 𝐟𝐨𝐫 𝐃𝐮𝐫𝐚𝐭𝐢𝐨𝐧 𝐃𝐚𝐭𝐚 **

Happy to share that our joint paper with Thomas Mikosch, Anders Rahbek, and Frederik Vilandt on statistical inference (and unit roots) in ACD models is forthcoming in the 𝗝𝗼𝘂𝗿𝗻𝗮𝗹 𝗼𝗳 𝘁𝗵𝗲 𝗥𝗼𝘆𝗮𝗹 𝗦𝘁𝗮𝘁𝗶𝘀𝘁𝗶𝗰𝗮𝗹 𝗦𝗼𝗰𝗶𝗲𝘁𝘆: 𝗦𝗲𝗿𝗶𝗲𝘀 𝗕!

ideas.repec.org/p/arx/papers...

Happy to share that our joint paper with Thomas Mikosch, Anders Rahbek, and Frederik Vilandt on statistical inference (and unit roots) in ACD models is forthcoming in the 𝗝𝗼𝘂𝗿𝗻𝗮𝗹 𝗼𝗳 𝘁𝗵𝗲 𝗥𝗼𝘆𝗮𝗹 𝗦𝘁𝗮𝘁𝗶𝘀𝘁𝗶𝗰𝗮𝗹 𝗦𝗼𝗰𝗶𝗲𝘁𝘆: 𝗦𝗲𝗿𝗶𝗲𝘀 𝗕!

ideas.repec.org/p/arx/papers...

*** 𝐡𝐞𝐭𝐞𝐫𝐨𝐠𝐞𝐧𝐞𝐨𝐮𝐬 𝐭𝐫𝐞𝐚𝐭𝐦𝐞𝐧𝐭 𝐞𝐟𝐟𝐞𝐜𝐭𝐬 𝐚𝐧𝐝 𝐑𝐃𝐃 ***

Interested in 𝐑𝐞𝐠𝐫𝐞𝐬𝐬𝐢𝐨𝐧 𝐃𝐢𝐬𝐜𝐨𝐧𝐭𝐢𝐧𝐮𝐢𝐭𝐲 𝐃𝐞𝐬𝐢𝐠𝐧𝐬 and treatment effect heterogeneity?

Check out this new framework by Sebastian Calonico, Matias Cattaneo, Max Farrell, Filippo Palomba & Rocio Titiunik, as well as its companion software paper.

Interested in 𝐑𝐞𝐠𝐫𝐞𝐬𝐬𝐢𝐨𝐧 𝐃𝐢𝐬𝐜𝐨𝐧𝐭𝐢𝐧𝐮𝐢𝐭𝐲 𝐃𝐞𝐬𝐢𝐠𝐧𝐬 and treatment effect heterogeneity?

Check out this new framework by Sebastian Calonico, Matias Cattaneo, Max Farrell, Filippo Palomba & Rocio Titiunik, as well as its companion software paper.

August 3, 2025 at 9:36 PM

*** 𝐡𝐞𝐭𝐞𝐫𝐨𝐠𝐞𝐧𝐞𝐨𝐮𝐬 𝐭𝐫𝐞𝐚𝐭𝐦𝐞𝐧𝐭 𝐞𝐟𝐟𝐞𝐜𝐭𝐬 𝐚𝐧𝐝 𝐑𝐃𝐃 ***

Interested in 𝐑𝐞𝐠𝐫𝐞𝐬𝐬𝐢𝐨𝐧 𝐃𝐢𝐬𝐜𝐨𝐧𝐭𝐢𝐧𝐮𝐢𝐭𝐲 𝐃𝐞𝐬𝐢𝐠𝐧𝐬 and treatment effect heterogeneity?

Check out this new framework by Sebastian Calonico, Matias Cattaneo, Max Farrell, Filippo Palomba & Rocio Titiunik, as well as its companion software paper.

Interested in 𝐑𝐞𝐠𝐫𝐞𝐬𝐬𝐢𝐨𝐧 𝐃𝐢𝐬𝐜𝐨𝐧𝐭𝐢𝐧𝐮𝐢𝐭𝐲 𝐃𝐞𝐬𝐢𝐠𝐧𝐬 and treatment effect heterogeneity?

Check out this new framework by Sebastian Calonico, Matias Cattaneo, Max Farrell, Filippo Palomba & Rocio Titiunik, as well as its companion software paper.

Reposted by Giuseppe Cavaliere

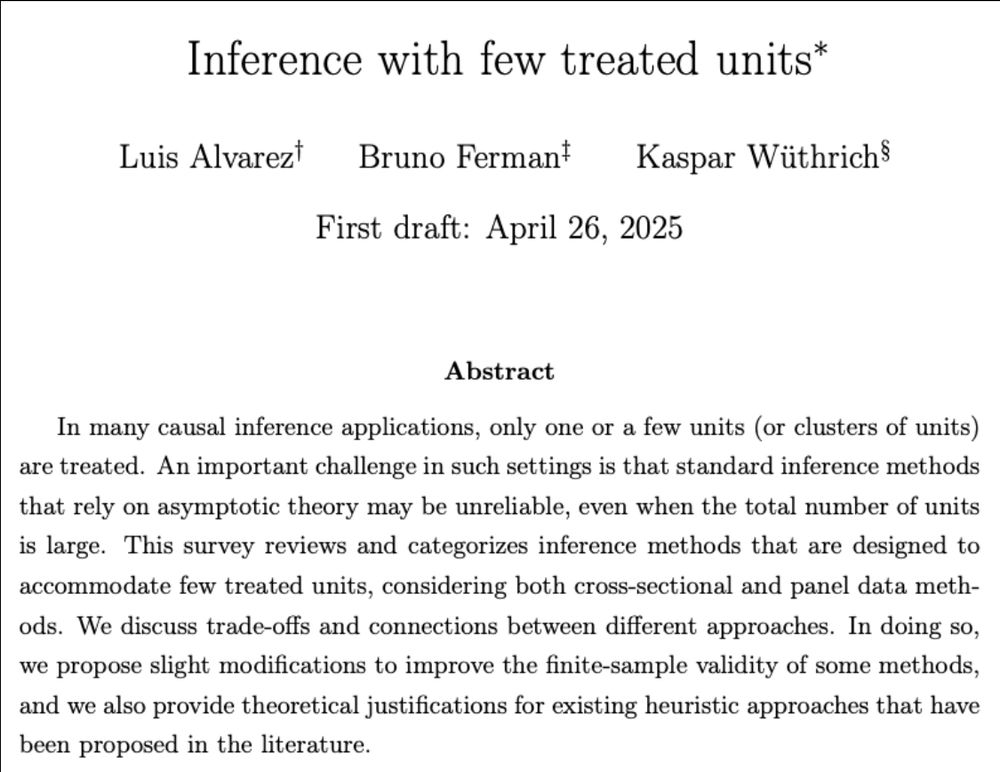

🧵New survey paper: "Inference with Few Treated Units"

Luis Alvarez, Bruno Ferman and Kaspar Wüthrich

Tired of referees saying your standard errors are wrong?

This survey will help you understand if you really have a problem — and, if so, how to fix it!

Luis Alvarez, Bruno Ferman and Kaspar Wüthrich

Tired of referees saying your standard errors are wrong?

This survey will help you understand if you really have a problem — and, if so, how to fix it!

April 29, 2025 at 2:18 PM

🧵New survey paper: "Inference with Few Treated Units"

Luis Alvarez, Bruno Ferman and Kaspar Wüthrich

Tired of referees saying your standard errors are wrong?

This survey will help you understand if you really have a problem — and, if so, how to fix it!

Luis Alvarez, Bruno Ferman and Kaspar Wüthrich

Tired of referees saying your standard errors are wrong?

This survey will help you understand if you really have a problem — and, if so, how to fix it!

A very interesting interview to one of the greatest statisticians of recent times - Marc Hallin. Highly recommended!

Link: onlinelibrary.wiley.com/doi/full/10....

Link: onlinelibrary.wiley.com/doi/full/10....

April 22, 2025 at 12:33 AM

A very interesting interview to one of the greatest statisticians of recent times - Marc Hallin. Highly recommended!

Link: onlinelibrary.wiley.com/doi/full/10....

Link: onlinelibrary.wiley.com/doi/full/10....

Very happy to see time series in Econometrica 😃

Does the randomness of the number of events affect the asymptotic theory for time series duration models? Our new theory shows that, contrary to prior beliefs, asymptotics can be non-standard in terms of convergence rates and asymptotic distribution. buff.ly/3Ewns53

March 9, 2025 at 8:30 AM

Very happy to see time series in Econometrica 😃

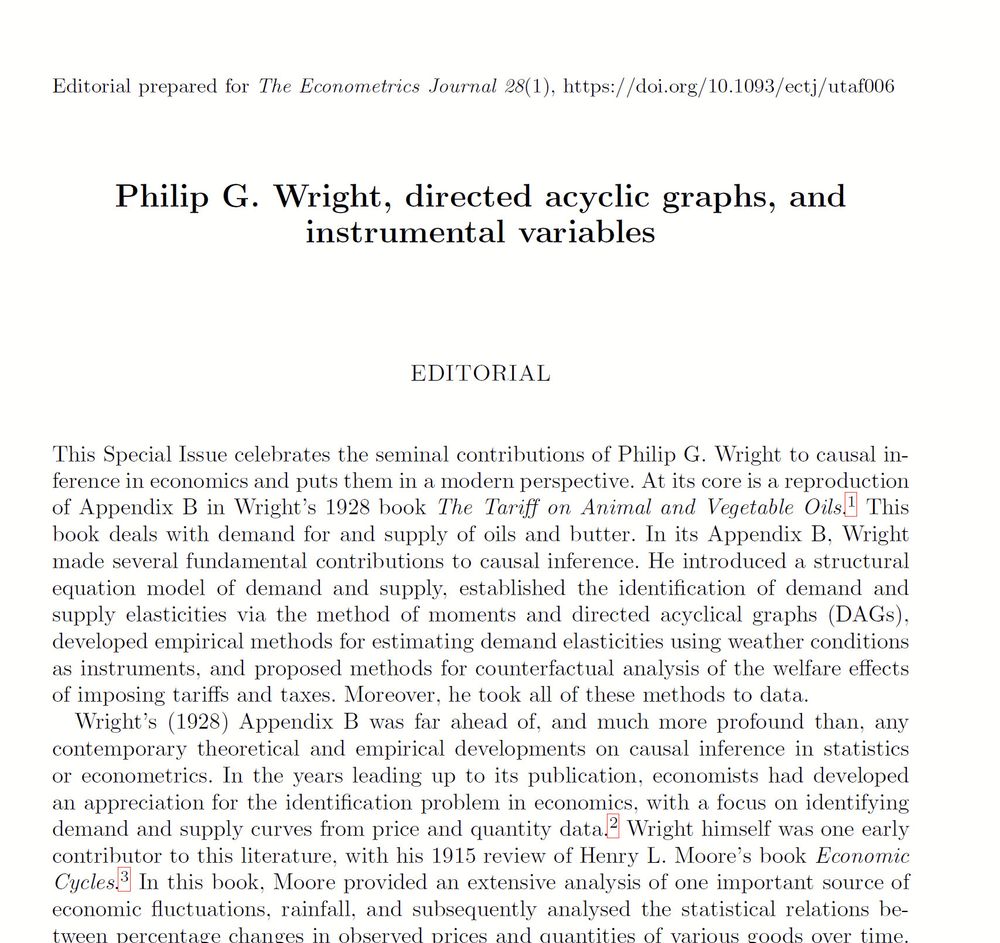

A very cool Econometrics Journal editorial by @jaapabbring.bsky.social, @victorchernozhukov.bsky.social & Fernandez-Val on Wright's 1928 contribution to causal inference and IV.

Very interesting stuff!

Link: arxiv.org/abs/2501.16395

Very interesting stuff!

Link: arxiv.org/abs/2501.16395

January 29, 2025 at 1:16 PM

A very cool Econometrics Journal editorial by @jaapabbring.bsky.social, @victorchernozhukov.bsky.social & Fernandez-Val on Wright's 1928 contribution to causal inference and IV.

Very interesting stuff!

Link: arxiv.org/abs/2501.16395

Very interesting stuff!

Link: arxiv.org/abs/2501.16395

Cavaliere-Mikosch-Rahbek-Vilandt on autoregressive conditional durations forthcoming in *Econometrica* !

www.econometricsociety.org/publications...

www.econometricsociety.org/publications...

January 20, 2025 at 11:16 AM

Cavaliere-Mikosch-Rahbek-Vilandt on autoregressive conditional durations forthcoming in *Econometrica* !

www.econometricsociety.org/publications...

www.econometricsociety.org/publications...

I've just been appointed for another term as Associate Editor of the @JEconometrics.

Proud to contribute to the premier journal for econometricians and to be part of its amazing editorial board!

#econometrics

Proud to contribute to the premier journal for econometricians and to be part of its amazing editorial board!

#econometrics

December 16, 2023 at 12:24 AM

I've just been appointed for another term as Associate Editor of the @JEconometrics.

Proud to contribute to the premier journal for econometricians and to be part of its amazing editorial board!

#econometrics

Proud to contribute to the premier journal for econometricians and to be part of its amazing editorial board!

#econometrics

Excellent news today - our paper on bootstrap inference with asymptotically biased estimators, joint with Silvia Goncalves, Morten Nielsen & Edoardo Zanelli, has been accepted by the 𝑱𝒐𝒖𝒓𝒏𝒂𝒍 𝒐𝒇 𝒕𝒉𝒆 𝑨𝒎𝒆𝒓𝒊𝒄𝒂𝒏 𝑺𝒕𝒂𝒕𝒊𝒔𝒕𝒊𝒄𝒂𝒍 𝑨𝒔𝒔𝒐𝒄𝒊𝒂𝒕𝒊𝒐𝒏! ⭐⭐⭐

For the paper, see: arxiv.org/abs/2208.02028

November 11, 2023 at 6:18 PM

Excellent news today - our paper on bootstrap inference with asymptotically biased estimators, joint with Silvia Goncalves, Morten Nielsen & Edoardo Zanelli, has been accepted by the 𝑱𝒐𝒖𝒓𝒏𝒂𝒍 𝒐𝒇 𝒕𝒉𝒆 𝑨𝒎𝒆𝒓𝒊𝒄𝒂𝒏 𝑺𝒕𝒂𝒕𝒊𝒔𝒕𝒊𝒄𝒂𝒍 𝑨𝒔𝒔𝒐𝒄𝒊𝒂𝒕𝒊𝒐𝒏! ⭐⭐⭐

For the paper, see: arxiv.org/abs/2208.02028

Today my macroeconometrics lecture took place in the anatomy department of @Unibo. It gave me a friendly reminder that ‘In the long run we are all dead.’ 😅

November 9, 2023 at 8:16 PM

Today my macroeconometrics lecture took place in the anatomy department of @Unibo. It gave me a friendly reminder that ‘In the long run we are all dead.’ 😅

Hi #EconSky!

Looking for (teaching) resources on intermediate macroeconomics?

François Geerolf (UCLA) offers a rich set of lecture notes, slides, and handouts.

Topics include growth, business cycles, unemployment, inflation, and open-economy macro issues.

Check it out! fgeerolf.com/econ102/

Looking for (teaching) resources on intermediate macroeconomics?

François Geerolf (UCLA) offers a rich set of lecture notes, slides, and handouts.

Topics include growth, business cycles, unemployment, inflation, and open-economy macro issues.

Check it out! fgeerolf.com/econ102/

October 8, 2023 at 4:15 PM

Hi #EconSky!

Looking for (teaching) resources on intermediate macroeconomics?

François Geerolf (UCLA) offers a rich set of lecture notes, slides, and handouts.

Topics include growth, business cycles, unemployment, inflation, and open-economy macro issues.

Check it out! fgeerolf.com/econ102/

Looking for (teaching) resources on intermediate macroeconomics?

François Geerolf (UCLA) offers a rich set of lecture notes, slides, and handouts.

Topics include growth, business cycles, unemployment, inflation, and open-economy macro issues.

Check it out! fgeerolf.com/econ102/

Hi #EconSky!

Working with causal inference, perhaps using RDDs?

This paper reveals significant multiple testing issues in empirical analyses from top-five econ journals.

They highlight pitfalls and possible solution.

Cool #econometrics stuff to read - check it out!

arxiv.org/abs/2205.04345

Working with causal inference, perhaps using RDDs?

This paper reveals significant multiple testing issues in empirical analyses from top-five econ journals.

They highlight pitfalls and possible solution.

Cool #econometrics stuff to read - check it out!

arxiv.org/abs/2205.04345

October 8, 2023 at 11:00 AM

Hi #EconSky!

Working with causal inference, perhaps using RDDs?

This paper reveals significant multiple testing issues in empirical analyses from top-five econ journals.

They highlight pitfalls and possible solution.

Cool #econometrics stuff to read - check it out!

arxiv.org/abs/2205.04345

Working with causal inference, perhaps using RDDs?

This paper reveals significant multiple testing issues in empirical analyses from top-five econ journals.

They highlight pitfalls and possible solution.

Cool #econometrics stuff to read - check it out!

arxiv.org/abs/2205.04345

How many econometricians out here?

September 28, 2023 at 7:28 PM

How many econometricians out here?

Financial markets, like probability measures, converge weakly. 🫣

September 26, 2023 at 2:31 PM

Financial markets, like probability measures, converge weakly. 🫣

Life through the lens of #econometrics

September 21, 2023 at 8:35 AM

Life through the lens of #econometrics