Steve Markus

@stevem1.bsky.social

Chesterfield UK based Investor, like small caps and general industrials. Fundies based on the whole, like to buy and hold. Background in management consulting and software/database tech across the development and implementation lifecycle.

Gleeson #GLE.L AGM TU, unexciting but steady, expects FY26 results to be in line with expectations but mindful of Autumn Budget, seeing some progress with reservation rates up on the same period YoY. One significant land sale still waiting for a technical solution

November 14, 2025 at 7:26 AM

Gleeson #GLE.L AGM TU, unexciting but steady, expects FY26 results to be in line with expectations but mindful of Autumn Budget, seeing some progress with reservation rates up on the same period YoY. One significant land sale still waiting for a technical solution

Melrose #MRO.L Q3 TU reads well, in line with full year expectations and Engines revenue up 28% with record backlogs, Structures up 5% helped by defence demand. A long way from GKN days.

November 14, 2025 at 7:20 AM

Melrose #MRO.L Q3 TU reads well, in line with full year expectations and Engines revenue up 28% with record backlogs, Structures up 5% helped by defence demand. A long way from GKN days.

Aviva #AV.L Q3 TU, on track to achieve 2026 targets a year early, Amanda Blanc 'the outlook for Aviva has never been better'. Upgrading savings from Direct Line acquisition, setting new 3 year targets. Reads very well.

November 13, 2025 at 7:41 AM

Aviva #AV.L Q3 TU, on track to achieve 2026 targets a year early, Amanda Blanc 'the outlook for Aviva has never been better'. Upgrading savings from Direct Line acquisition, setting new 3 year targets. Reads very well.

Convatec #CTEC.L 10 month TU, full yr 2025 in line, expecting 2026 to be another year of double-digit adjusted EPS growth. Some ongoing regulatory difficulties for product Innovamatrix, but not holding back growth. New CEO and CFO following unfortunate death thru illness of previous CEO Karim Bitar.

November 13, 2025 at 7:27 AM

Convatec #CTEC.L 10 month TU, full yr 2025 in line, expecting 2026 to be another year of double-digit adjusted EPS growth. Some ongoing regulatory difficulties for product Innovamatrix, but not holding back growth. New CEO and CFO following unfortunate death thru illness of previous CEO Karim Bitar.

Keller #KLR.L Q3 TU, confirming in line for full yr, Asia-Pacific performance 'robust', everywhere else seems fairly solid. Approaching net cash position by end of year. Record level order book, geographic diversity give visibility and resilience. Happy as a long term holder.

November 13, 2025 at 7:14 AM

Keller #KLR.L Q3 TU, confirming in line for full yr, Asia-Pacific performance 'robust', everywhere else seems fairly solid. Approaching net cash position by end of year. Record level order book, geographic diversity give visibility and resilience. Happy as a long term holder.

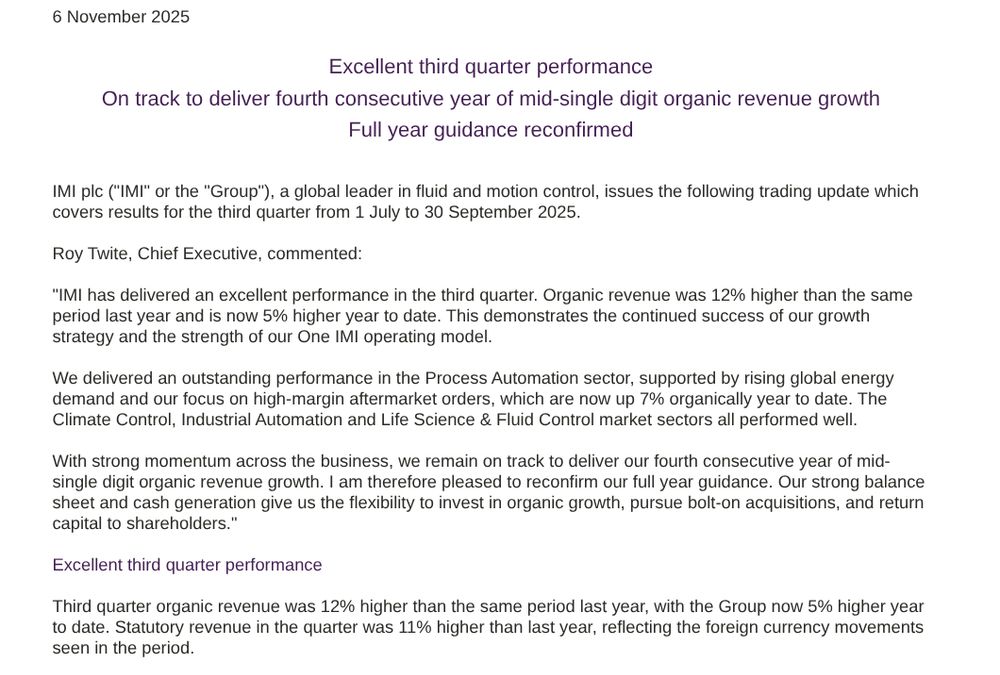

#IMI.L Q3 TU, plenty of repetitions of excellent, reads well. On track for full year expectations of mid single-digit growth and adj eps between 129 and 135p. Process Automation doing particularly well with revenue up 14%YTD and 26% in Q3.

November 6, 2025 at 7:13 AM

#IMI.L Q3 TU, plenty of repetitions of excellent, reads well. On track for full year expectations of mid single-digit growth and adj eps between 129 and 135p. Process Automation doing particularly well with revenue up 14%YTD and 26% in Q3.

Headlam #HEAD.L TU, surprisingly getting rid of CEO Payne has not helped and revenue in the recent quarter is 5% down YoY, so results for the year will be below expectations - the already downgraded ones from Sept interims. Restructure, cost reduction, asset sales plan. Board confident blah blah...

November 5, 2025 at 7:13 AM

Headlam #HEAD.L TU, surprisingly getting rid of CEO Payne has not helped and revenue in the recent quarter is 5% down YoY, so results for the year will be below expectations - the already downgraded ones from Sept interims. Restructure, cost reduction, asset sales plan. Board confident blah blah...

Solid State #SOLI.L H1 TU, healthy with revenue and adj PBT in excess of £85M and £4.75M. Seen some of their lumpy revenue come through, margins improved. H2 looking positive with order book £87.3M of which over 60% expected in H2, underpins FY excptns. Progress in shift to higher value activities,

November 4, 2025 at 7:26 AM

Solid State #SOLI.L H1 TU, healthy with revenue and adj PBT in excess of £85M and £4.75M. Seen some of their lumpy revenue come through, margins improved. H2 looking positive with order book £87.3M of which over 60% expected in H2, underpins FY excptns. Progress in shift to higher value activities,

Zotefoams #ZTF.L Q3 TU, performance in line with expectations and (caveated) full year revenue and adjusted PBT to be in line, to deliver mid single-digit growth for year as a whole. Plenty of strategic progress including interesting appointment of ex-Nike manager.

November 4, 2025 at 7:19 AM

Zotefoams #ZTF.L Q3 TU, performance in line with expectations and (caveated) full year revenue and adjusted PBT to be in line, to deliver mid single-digit growth for year as a whole. Plenty of strategic progress including interesting appointment of ex-Nike manager.

Brief Q3 TU from Spectris #SXS.L which is another holding being acquired, looks to be recovering with sales increasing YoY, up 11% on a reported bases and 4% at constant currency. Full year adjusted operating profit in line with expectations. Shame they are leaving the market.

October 30, 2025 at 7:22 AM

Brief Q3 TU from Spectris #SXS.L which is another holding being acquired, looks to be recovering with sales increasing YoY, up 11% on a reported bases and 4% at constant currency. Full year adjusted operating profit in line with expectations. Shame they are leaving the market.

TT Electronics #TTG.L have a takeover offer worth 155p, cash of 100p and shares in the acquirer worth 55p, from Swiss listed Cicor. Unanimous support from the TTG Board, maybe this will get further than the Volex attempt. No holding in TTG.

October 30, 2025 at 7:09 AM

TT Electronics #TTG.L have a takeover offer worth 155p, cash of 100p and shares in the acquirer worth 55p, from Swiss listed Cicor. Unanimous support from the TTG Board, maybe this will get further than the Volex attempt. No holding in TTG.

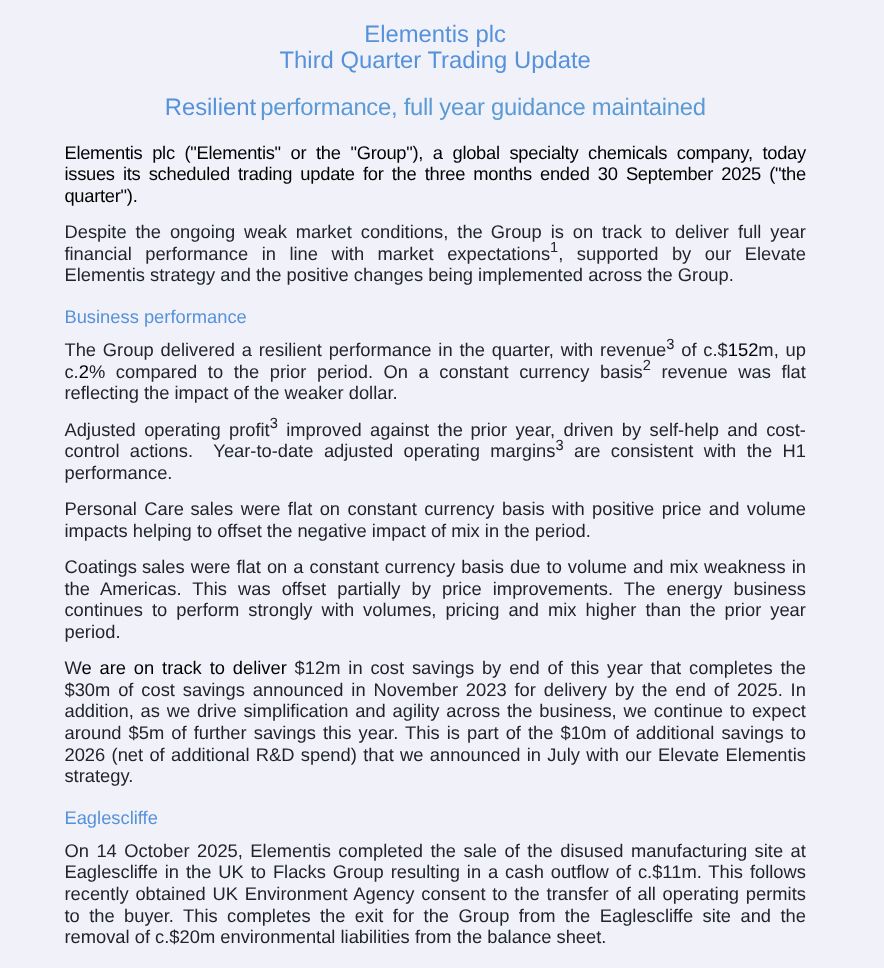

Elementis #ELM.L Q3 TU, on track for full yr performance in line with expectations, cost savings exceeding original target with further $5M expected this yr. Completed sale of Eaglescliffe site, altho they had to pay the purchaser $11M to take it! Was subject to an environmental 'incident' in 2023.

October 29, 2025 at 7:15 AM

Elementis #ELM.L Q3 TU, on track for full yr performance in line with expectations, cost savings exceeding original target with further $5M expected this yr. Completed sale of Eaglescliffe site, altho they had to pay the purchaser $11M to take it! Was subject to an environmental 'incident' in 2023.

Goodwin #GDWN.L issue a TU and break one of their normal rules by providing forward guidance - done because trading PBT for FY26 > £71M, 100% increase YoY with a 'high degree of confidence'. Plus... a special interim dividend of 532p. What a nice Monday morning surprise.

October 27, 2025 at 7:13 AM

Goodwin #GDWN.L issue a TU and break one of their normal rules by providing forward guidance - done because trading PBT for FY26 > £71M, 100% increase YoY with a 'high degree of confidence'. Plus... a special interim dividend of 532p. What a nice Monday morning surprise.

Alumasc #ALU.L AGM TU, cautious in tone especially for H1, Housebuilding still positive, Building Envelope/Water Mgmt revenue constrained by delays, despite healthy order books. Export good but lower YoY due to HK project last yr. Cautioun for H1, H2 weighting in 25/26, medium term very positive.

October 24, 2025 at 6:13 AM

Alumasc #ALU.L AGM TU, cautious in tone especially for H1, Housebuilding still positive, Building Envelope/Water Mgmt revenue constrained by delays, despite healthy order books. Export good but lower YoY due to HK project last yr. Cautioun for H1, H2 weighting in 25/26, medium term very positive.

Renishaw #RSW.L Q1 TU moderately encouraging, 2.8% revenue growth, America doing well, EMEA poor. New products introduced and a cost reduction program bringing £20M payroll savings. Steady start, markets presenting growth opportunities, expecting further steady revenue growth at this stage.

October 23, 2025 at 6:23 AM

Renishaw #RSW.L Q1 TU moderately encouraging, 2.8% revenue growth, America doing well, EMEA poor. New products introduced and a cost reduction program bringing £20M payroll savings. Steady start, markets presenting growth opportunities, expecting further steady revenue growth at this stage.

Macfarlane #MACF.L warning full yr adj operating profit to be 20-25% below expectations. Due to a combination of a fatal incident at one of Pitreavie sites causing temporary suspension of activity, and slower than expected market recovery in Distribution. Manufacturing still performing well.

October 22, 2025 at 6:09 AM

Macfarlane #MACF.L warning full yr adj operating profit to be 20-25% below expectations. Due to a combination of a fatal incident at one of Pitreavie sites causing temporary suspension of activity, and slower than expected market recovery in Distribution. Manufacturing still performing well.

XP Power #XPP.L Q3 TU, in line with full yr expectations and Q3 apparently sees a material step-up in profitability, together with generally improving quarterly figures, apart from debt which is up slightly. Appeal against Comet court judgement was heard in September, judges to consider verdict.

October 21, 2025 at 6:37 AM

XP Power #XPP.L Q3 TU, in line with full yr expectations and Q3 apparently sees a material step-up in profitability, together with generally improving quarterly figures, apart from debt which is up slightly. Appeal against Comet court judgement was heard in September, judges to consider verdict.

SigmaRoc #SRC.L Q3 TU, strong Q3 'underpins confidence in full year expectations', underlying EBITDA margins up, full yr EPS to be not less than 9.5p. Generally positive, UK/Ireland doing well, Belgium and Germany showing some early positive signs. Synergy programmes also having a positive effect.

October 21, 2025 at 6:24 AM

SigmaRoc #SRC.L Q3 TU, strong Q3 'underpins confidence in full year expectations', underlying EBITDA margins up, full yr EPS to be not less than 9.5p. Generally positive, UK/Ireland doing well, Belgium and Germany showing some early positive signs. Synergy programmes also having a positive effect.

GB Group #GBG.L H1 TU reads OK, in line with revenue £135M, well positioned to achieve H2 growth in Americas business. Acquiring DataTools address and data validation in Australia and NZ, for £7.9M, immediately earnings accretive. Well positioned to 'achieve our revenue outlook for full year' inline

October 16, 2025 at 6:21 AM

GB Group #GBG.L H1 TU reads OK, in line with revenue £135M, well positioned to achieve H2 growth in Americas business. Acquiring DataTools address and data validation in Australia and NZ, for £7.9M, immediately earnings accretive. Well positioned to 'achieve our revenue outlook for full year' inline

Sanderson #SDG.L interims look reasonable, revenue down slightly with profitability flat. Some bright spots with licensing revenue up 6%, net cash £7.8M, brand sales up 5% in first 9 weeks of H2. Confident of meeting expectations for the full year. Slightly more positive than last few statements.

October 15, 2025 at 6:17 AM

Sanderson #SDG.L interims look reasonable, revenue down slightly with profitability flat. Some bright spots with licensing revenue up 6%, net cash £7.8M, brand sales up 5% in first 9 weeks of H2. Confident of meeting expectations for the full year. Slightly more positive than last few statements.

Robert Walters #RWA.L Q3 TU, Asia Pacific (largest sector in terms of net income) saw broad based imprvmnt, UK saw Specialist Recruitment grow by 6%, Europe still difficult. Seeing signs of sustained improvement in select markets but conditions fragile. Net cash £26.6M, to review divi in March 26.

October 14, 2025 at 6:32 AM

Robert Walters #RWA.L Q3 TU, Asia Pacific (largest sector in terms of net income) saw broad based imprvmnt, UK saw Specialist Recruitment grow by 6%, Europe still difficult. Seeing signs of sustained improvement in select markets but conditions fragile. Net cash £26.6M, to review divi in March 26.

Morgan Advanced Materials #MGAM.L Q3 TU sounds quite gloomy with 'we now expect full year sales to be 4% lower than the prior year' and adj operating profit margin of ~10%, implying a guiding down of expectations but not in any specific way. Meanwhile they are busy buying back shares.

October 14, 2025 at 6:24 AM

Morgan Advanced Materials #MGAM.L Q3 TU sounds quite gloomy with 'we now expect full year sales to be 4% lower than the prior year' and adj operating profit margin of ~10%, implying a guiding down of expectations but not in any specific way. Meanwhile they are busy buying back shares.

Hollywood #BOWL.L FY TU reads OK (apart from reporting adj EBITDA) with record revenue £250.8M, adj EBITDA in line with expectations, net cash of £15.2M, good growth in Canada 32.9% and 6.4% in the UK. Strong pipeline of new centres, confident in outlook for 2026 and beyond.

October 14, 2025 at 6:13 AM

Hollywood #BOWL.L FY TU reads OK (apart from reporting adj EBITDA) with record revenue £250.8M, adj EBITDA in line with expectations, net cash of £15.2M, good growth in Canada 32.9% and 6.4% in the UK. Strong pipeline of new centres, confident in outlook for 2026 and beyond.

Oxford Instruments #OXIG.L H1 TU, warning that full yr revenue and adj operating profit to be similar to last year, quite a big downgrade. Multiple reasons but difficult markets and currency headwinds, particularly on Imaging and Analysis business. Adv Technology remains strong.

October 13, 2025 at 6:26 AM

Oxford Instruments #OXIG.L H1 TU, warning that full yr revenue and adj operating profit to be similar to last year, quite a big downgrade. Multiple reasons but difficult markets and currency headwinds, particularly on Imaging and Analysis business. Adv Technology remains strong.