Simon Pittaway

@simonpittaway.bsky.social

Working on macro, wealth and household balance sheets at the Resolution Foundation.

Finally, another potential explanation for the strength of US services is an uptick in business dynamism. Covid shook up the US economy in a big way, and there has been a long-lived uptick in labour reallocation and business formation – which hasn’t been matched in Britain.

April 8, 2025 at 9:49 AM

Finally, another potential explanation for the strength of US services is an uptick in business dynamism. Covid shook up the US economy in a big way, and there has been a long-lived uptick in labour reallocation and business formation – which hasn’t been matched in Britain.

Look at the type of investment, tech adoption seems to play a major role. Either side of the pandemic, American businesses increased spending on software twice as quickly as their British counterparts. We see a similar pattern in related investments like ICT and R&D.

April 8, 2025 at 9:49 AM

Look at the type of investment, tech adoption seems to play a major role. Either side of the pandemic, American businesses increased spending on software twice as quickly as their British counterparts. We see a similar pattern in related investments like ICT and R&D.

This pattern of outperformance is consistent with a concentrated investment slowdown since the Brexit referendum. In key service sectors, investment has now fallen so low that it only just offsets deprecation – i.e. these sectors' capital stock in didn’t grow in 2023.

April 8, 2025 at 9:49 AM

This pattern of outperformance is consistent with a concentrated investment slowdown since the Brexit referendum. In key service sectors, investment has now fallen so low that it only just offsets deprecation – i.e. these sectors' capital stock in didn’t grow in 2023.

3️⃣ Tech-using sectors are key

America’s growing advantage in services isn’t confined to the tech (ICT) sector. Professional services account for 2x as much of the recent productivity divergence. In reality, the US has outperformed the UK in a range of key service sectors.

America’s growing advantage in services isn’t confined to the tech (ICT) sector. Professional services account for 2x as much of the recent productivity divergence. In reality, the US has outperformed the UK in a range of key service sectors.

April 8, 2025 at 9:49 AM

3️⃣ Tech-using sectors are key

America’s growing advantage in services isn’t confined to the tech (ICT) sector. Professional services account for 2x as much of the recent productivity divergence. In reality, the US has outperformed the UK in a range of key service sectors.

America’s growing advantage in services isn’t confined to the tech (ICT) sector. Professional services account for 2x as much of the recent productivity divergence. In reality, the US has outperformed the UK in a range of key service sectors.

But, surprisingly, the US’s growing productivity advantage has been concentrated in less energy-intensive service sectors.

This isn’t to say energy prices don’t matter, but other factors have been more important in explaining sectoral productivity growth in recent years.

This isn’t to say energy prices don’t matter, but other factors have been more important in explaining sectoral productivity growth in recent years.

April 8, 2025 at 9:49 AM

But, surprisingly, the US’s growing productivity advantage has been concentrated in less energy-intensive service sectors.

This isn’t to say energy prices don’t matter, but other factors have been more important in explaining sectoral productivity growth in recent years.

This isn’t to say energy prices don’t matter, but other factors have been more important in explaining sectoral productivity growth in recent years.

2️⃣ Energy prices??

The UK has seen a massive spike in energy prices since 2019. Industrial gas prices rose by 158% between 2019 and 2023, compared to a 21% rise in the US. And because we’re so gas-dependent for electricity generation, electricity prices rose sharply too.

The UK has seen a massive spike in energy prices since 2019. Industrial gas prices rose by 158% between 2019 and 2023, compared to a 21% rise in the US. And because we’re so gas-dependent for electricity generation, electricity prices rose sharply too.

April 8, 2025 at 9:49 AM

2️⃣ Energy prices??

The UK has seen a massive spike in energy prices since 2019. Industrial gas prices rose by 158% between 2019 and 2023, compared to a 21% rise in the US. And because we’re so gas-dependent for electricity generation, electricity prices rose sharply too.

The UK has seen a massive spike in energy prices since 2019. Industrial gas prices rose by 158% between 2019 and 2023, compared to a 21% rise in the US. And because we’re so gas-dependent for electricity generation, electricity prices rose sharply too.

The mining and quarrying sector (of which oil and gas is the main part) accounts for 1/6th of the post-pandemic productivity divergence between Britain and America, despite being less than 2% of GDP in both countries.

April 8, 2025 at 9:49 AM

The mining and quarrying sector (of which oil and gas is the main part) accounts for 1/6th of the post-pandemic productivity divergence between Britain and America, despite being less than 2% of GDP in both countries.

1️⃣ Oil and gas

Production keeps booming in America while dwindling in Britain. Hours are sticky though: workers in UK mining and sector clocked the same number of hours in 2019 as they did in 2005, despite extraction falling ~50%. Less output + same hours = falling productivity.

Production keeps booming in America while dwindling in Britain. Hours are sticky though: workers in UK mining and sector clocked the same number of hours in 2019 as they did in 2005, despite extraction falling ~50%. Less output + same hours = falling productivity.

April 8, 2025 at 9:49 AM

1️⃣ Oil and gas

Production keeps booming in America while dwindling in Britain. Hours are sticky though: workers in UK mining and sector clocked the same number of hours in 2019 as they did in 2005, despite extraction falling ~50%. Less output + same hours = falling productivity.

Production keeps booming in America while dwindling in Britain. Hours are sticky though: workers in UK mining and sector clocked the same number of hours in 2019 as they did in 2005, despite extraction falling ~50%. Less output + same hours = falling productivity.

Britain isn’t alone in its recent struggles. In the G7, Canada, France and Italy have all seen productivity fall since Q4 2019. But (up until now at least) America has been in a league of its own.

In the paper, I set out three things to know about the recent US-UK divergence in productivity.

In the paper, I set out three things to know about the recent US-UK divergence in productivity.

April 8, 2025 at 9:49 AM

Britain isn’t alone in its recent struggles. In the G7, Canada, France and Italy have all seen productivity fall since Q4 2019. But (up until now at least) America has been in a league of its own.

In the paper, I set out three things to know about the recent US-UK divergence in productivity.

In the paper, I set out three things to know about the recent US-UK divergence in productivity.

What we've seen is growth slowing across most of the UK economy. A notable slowdown has been in Info & comms, the main source of productivity growth in the 2010s. It’s still contributing more than any other sector to aggregate productivity growth, but only half as much as before.

April 8, 2025 at 9:49 AM

What we've seen is growth slowing across most of the UK economy. A notable slowdown has been in Info & comms, the main source of productivity growth in the 2010s. It’s still contributing more than any other sector to aggregate productivity growth, but only half as much as before.

This partly reflects measurement difficulties, as labour productivity in healthcare doesn’t capture quality improvements. But even if we used NHS England’s quality-adjusted measure of acute care productivity, overall UK productivity would have grown just 0.3% from 2019 to 2024.

April 8, 2025 at 9:49 AM

This partly reflects measurement difficulties, as labour productivity in healthcare doesn’t capture quality improvements. But even if we used NHS England’s quality-adjusted measure of acute care productivity, overall UK productivity would have grown just 0.3% from 2019 to 2024.

What’s behind this? I find that the health sector has been the biggest drag on aggregate productivity since 2019. It’s our third biggest sector by gross-value added, and only the tiny sectors of mining and utilities have seen bigger sectoral productivity hits.

April 8, 2025 at 9:49 AM

What’s behind this? I find that the health sector has been the biggest drag on aggregate productivity since 2019. It’s our third biggest sector by gross-value added, and only the tiny sectors of mining and utilities have seen bigger sectoral productivity hits.

More reliable data sources point to a stronger post-pandemic recovery in employment than the LFS, and a lower level of productivity as a result. Our preferred estimate – based on HMRC’s payroll and tax data – suggests productivity fell by a cumulative 0.5% between 2019 and 2023.

April 8, 2025 at 9:49 AM

More reliable data sources point to a stronger post-pandemic recovery in employment than the LFS, and a lower level of productivity as a result. Our preferred estimate – based on HMRC’s payroll and tax data – suggests productivity fell by a cumulative 0.5% between 2019 and 2023.

Worryingly, things have got worse in the 2020s. Headline data says productivity grew by 1.8% in total between 2019 and 2024, about two-thirds of the UK’s already meagre 2010s growth rate.

But this is based on unreliable LFS data and probably *understates* the scale of the problem.

But this is based on unreliable LFS data and probably *understates* the scale of the problem.

April 8, 2025 at 9:49 AM

Worryingly, things have got worse in the 2020s. Headline data says productivity grew by 1.8% in total between 2019 and 2024, about two-thirds of the UK’s already meagre 2010s growth rate.

But this is based on unreliable LFS data and probably *understates* the scale of the problem.

But this is based on unreliable LFS data and probably *understates* the scale of the problem.

Productivity growth matters a lot. It is the main driver of higher wages across countries or over time. But in 2010s Britain, productivity (measured as GDP per hour) grew by just 0.6% per year - the lowest in the G7 bar Italy.

April 8, 2025 at 9:49 AM

Productivity growth matters a lot. It is the main driver of higher wages across countries or over time. But in 2010s Britain, productivity (measured as GDP per hour) grew by just 0.6% per year - the lowest in the G7 bar Italy.

New research out from me today: why has Britain experienced so little productivity growth in recent years? And why (at least up until now) has the US has performed so much better?

Spoiler: it’s not just tech companies and energy prices 🧵

Spoiler: it’s not just tech companies and energy prices 🧵

April 8, 2025 at 9:49 AM

New research out from me today: why has Britain experienced so little productivity growth in recent years? And why (at least up until now) has the US has performed so much better?

Spoiler: it’s not just tech companies and energy prices 🧵

Spoiler: it’s not just tech companies and energy prices 🧵

The weaker outlook could cause a fiscal headache for the Chancellor. The OBR had predicted growth of 0.7% in H2 2024, versus the 0.1% we got. Unless the OBR uprates its already optimistic view of future growth, this is likely to mean less tax revenue than previously forecast.

February 13, 2025 at 9:58 AM

The weaker outlook could cause a fiscal headache for the Chancellor. The OBR had predicted growth of 0.7% in H2 2024, versus the 0.1% we got. Unless the OBR uprates its already optimistic view of future growth, this is likely to mean less tax revenue than previously forecast.

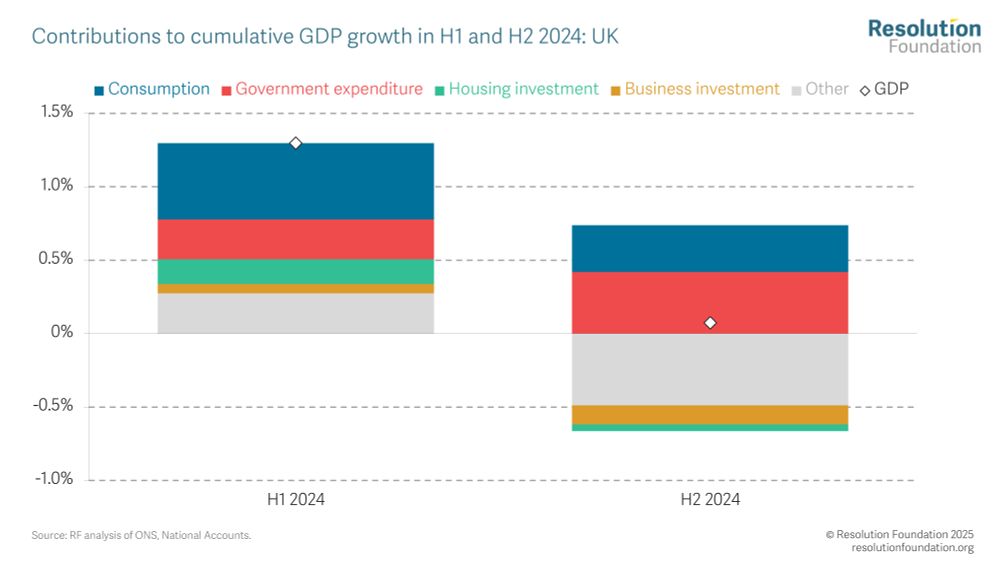

Indeed, a slowdown in households’ spending was one of the drivers of last year’s slowdown. But, as suggested by the key role of business-facing services above, it was far from the whole story (and the big ‘other’ bar for H2 suggests the picture could change in later releases).

February 13, 2025 at 9:58 AM

Indeed, a slowdown in households’ spending was one of the drivers of last year’s slowdown. But, as suggested by the key role of business-facing services above, it was far from the whole story (and the big ‘other’ bar for H2 suggests the picture could change in later releases).

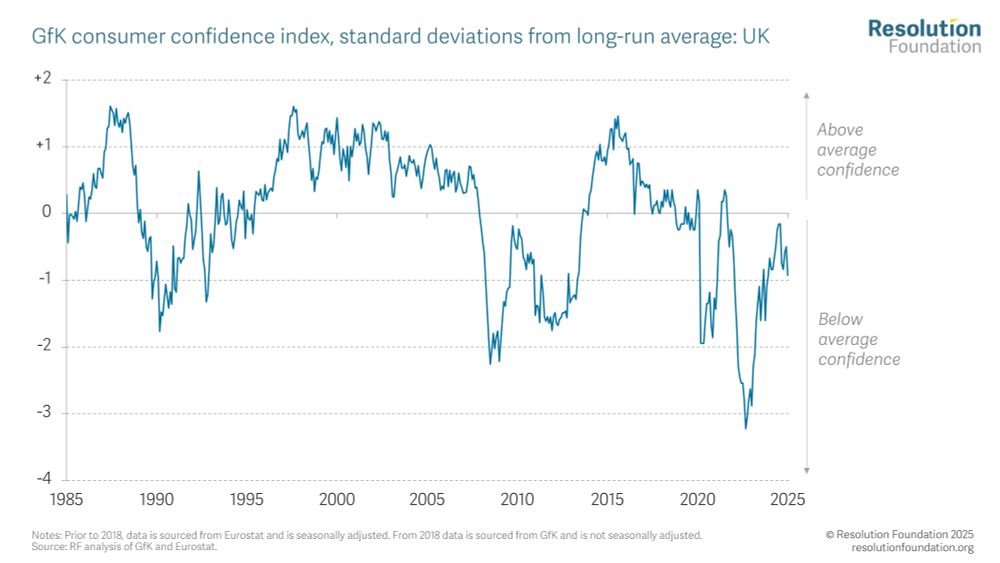

There were clear signs that consumer confidence weakened last year, with the GfK consumer confidence index remaining well below its long-run average and retail sales tailing off towards year-end.

February 13, 2025 at 9:58 AM

There were clear signs that consumer confidence weakened last year, with the GfK consumer confidence index remaining well below its long-run average and retail sales tailing off towards year-end.

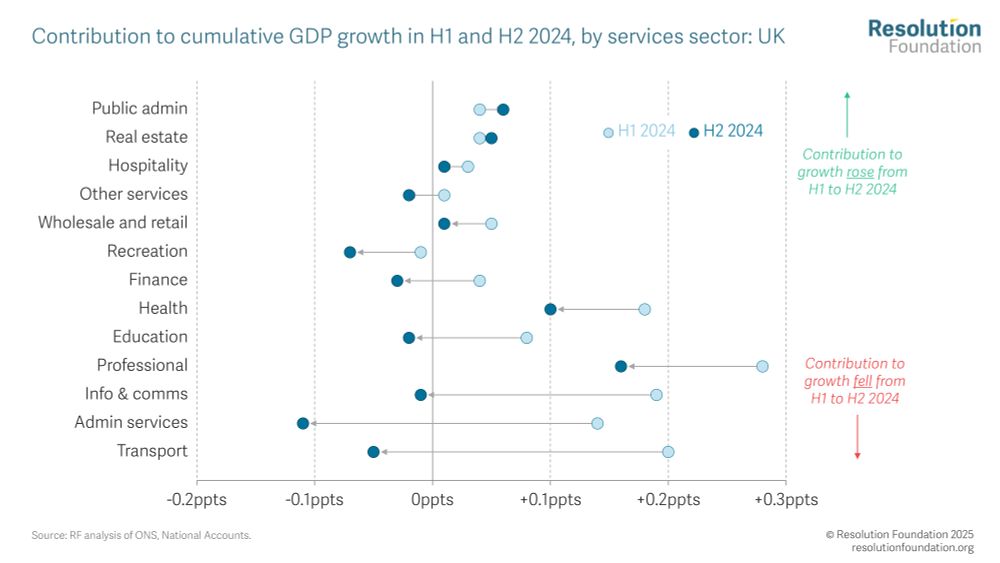

Within services, most subsectors slowed. But the most consequential slowdowns were in info & comms, admin services and transport. These three sectors were big drivers of growth in Q1, but their contributions turned negative in H2.

February 13, 2025 at 9:58 AM

Within services, most subsectors slowed. But the most consequential slowdowns were in info & comms, admin services and transport. These three sectors were big drivers of growth in Q1, but their contributions turned negative in H2.

Digging into the UK data, what drove the growth slowdown in 2024?

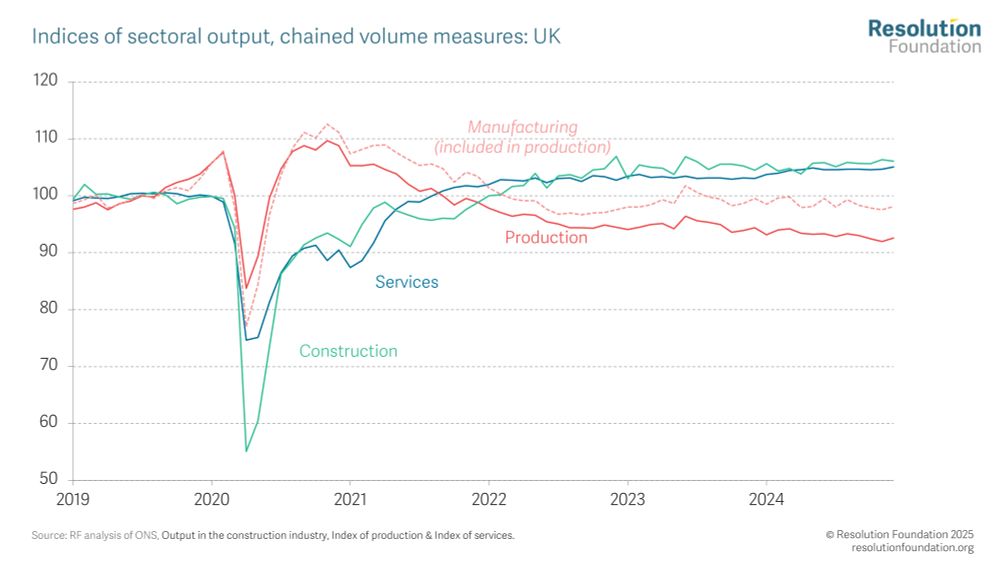

Most of the slowdown came from services, which contributed 1.3ppts to total growth in H1 and just 0.1ppts in H2. But note that the *level* of activity remains weakest in the production sector.

Most of the slowdown came from services, which contributed 1.3ppts to total growth in H1 and just 0.1ppts in H2. But note that the *level* of activity remains weakest in the production sector.

February 13, 2025 at 9:58 AM

Digging into the UK data, what drove the growth slowdown in 2024?

Most of the slowdown came from services, which contributed 1.3ppts to total growth in H1 and just 0.1ppts in H2. But note that the *level* of activity remains weakest in the production sector.

Most of the slowdown came from services, which contributed 1.3ppts to total growth in H1 and just 0.1ppts in H2. But note that the *level* of activity remains weakest in the production sector.

The UK isn’t alone in its recent struggles – Canada and Germany have seen GDP per capita fall by slightly more over the past five years. But if the UK had managed even the average recovery of other G7 economies, annual GDP per capita would be £450 higher today.

February 13, 2025 at 9:58 AM

The UK isn’t alone in its recent struggles – Canada and Germany have seen GDP per capita fall by slightly more over the past five years. But if the UK had managed even the average recovery of other G7 economies, annual GDP per capita would be £450 higher today.

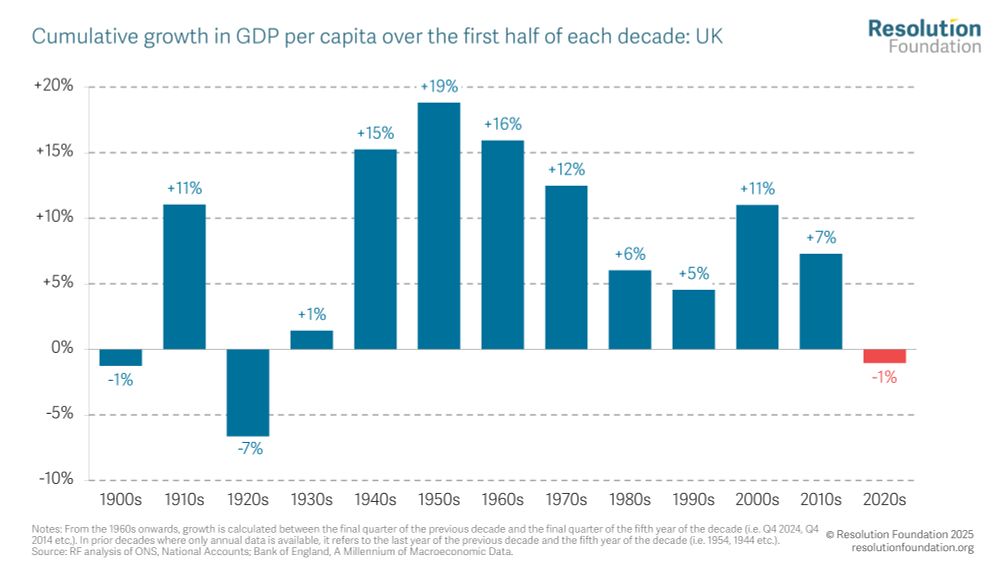

Our shocking record of per capita growth means that we’re now halfway through the 2020s and GDP per capita is lower than when the decade started. By my calculations, that hasn’t happened in any decade since the 1920s!

February 13, 2025 at 9:58 AM

Our shocking record of per capita growth means that we’re now halfway through the 2020s and GDP per capita is lower than when the decade started. By my calculations, that hasn’t happened in any decade since the 1920s!

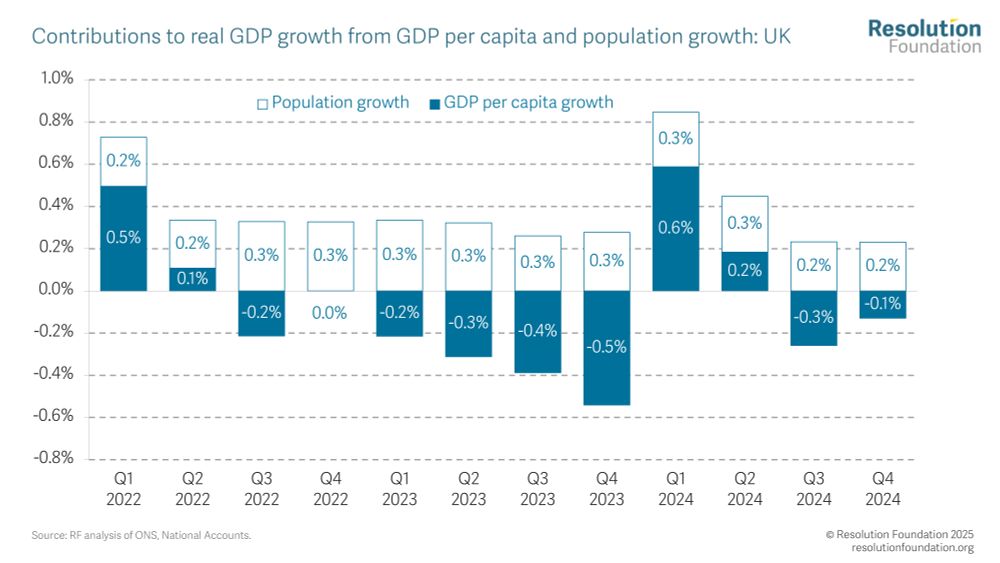

In contrast to modest headline growth, GDP per capita shrank once again.

Worryingly, we’ve now only seen four quarters of per capita growth in the past three years of data (going back to the start of 2022).

Worryingly, we’ve now only seen four quarters of per capita growth in the past three years of data (going back to the start of 2022).

February 13, 2025 at 9:58 AM

In contrast to modest headline growth, GDP per capita shrank once again.

Worryingly, we’ve now only seen four quarters of per capita growth in the past three years of data (going back to the start of 2022).

Worryingly, we’ve now only seen four quarters of per capita growth in the past three years of data (going back to the start of 2022).

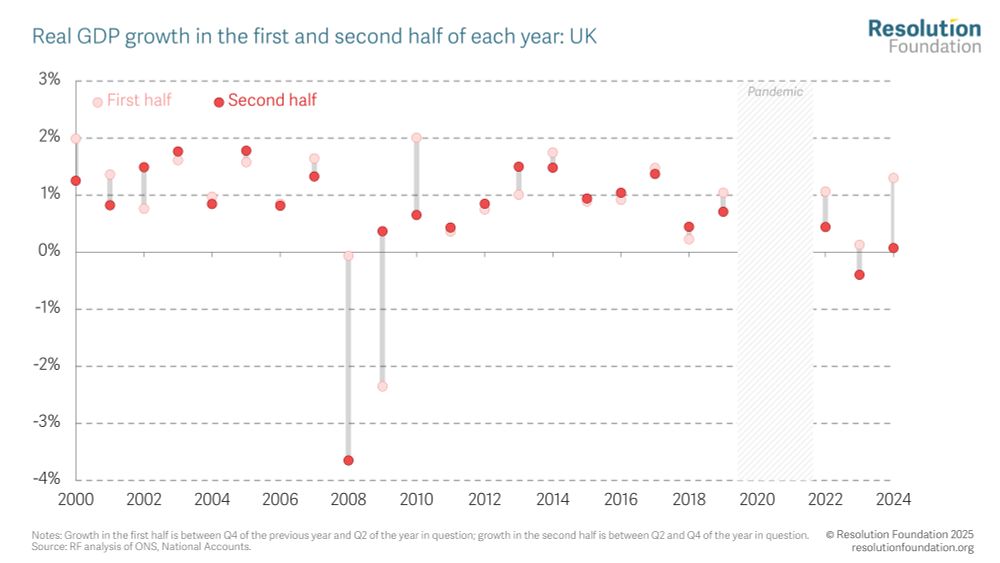

But, looking at 2024 as a whole, growth slowed dramatically over the course of the year. The UK economy grew 1.3% in the first half of 2024 and slowed to just 0.1% in the second half – the sharpest slowdown outside of the pandemic since 2010.

February 13, 2025 at 9:58 AM

But, looking at 2024 as a whole, growth slowed dramatically over the course of the year. The UK economy grew 1.3% in the first half of 2024 and slowed to just 0.1% in the second half – the sharpest slowdown outside of the pandemic since 2010.