Alex

@s3alfisc.bsky.social

Data Science, open source and economics. Currently working on fwildclusterboot and pyfixest.

https://github.com/s3alfisc

https://github.com/s3alfisc

Oh interesting, this does not look good. For me everything has been working well, I just upgraded to the newest fixest release via conda-forge a few weeks ago without any problems (as it happens, on windows!).

October 2, 2025 at 9:16 PM

Oh interesting, this does not look good. For me everything has been working well, I just upgraded to the newest fixest release via conda-forge a few weeks ago without any problems (as it happens, on windows!).

No global R or Python installation needed! And if you have these, no interference with your global installations.

Big fan. pixi.sh/latest/

Big fan. pixi.sh/latest/

October 2, 2025 at 8:47 PM

No global R or Python installation needed! And if you have these, no interference with your global installations.

Big fan. pixi.sh/latest/

Big fan. pixi.sh/latest/

Next step is to rewrite the vignette (more to the point & I need to make a better case for the methods usefulness in business contexts).

August 16, 2025 at 8:37 AM

Next step is to rewrite the vignette (more to the point & I need to make a better case for the methods usefulness in business contexts).

Also works with "negative" effects:

August 16, 2025 at 8:35 AM

Also works with "negative" effects:

In contrast to uv, it is cross-language and also allows to pin down non-python dependencies in the same env (R, Julia, etc). And it also has nice "pixi run command" options (you can even define tasks as in justfiles, which I personally use a lot). pixi.sh/latest/

August 15, 2025 at 9:38 PM

In contrast to uv, it is cross-language and also allows to pin down non-python dependencies in the same env (R, Julia, etc). And it also has nice "pixi run command" options (you can even define tasks as in justfiles, which I personally use a lot). pixi.sh/latest/

For pyfixest's development, we've been using pixi for a while, which I really enjoy. More or less it is the conda-forge (free & open source) equivalent to uv (it actually runs uv for PyPi dependency resolution). Really fast both for PyPi & conda-forge dependency resolution.

August 15, 2025 at 9:38 PM

For pyfixest's development, we've been using pixi for a while, which I really enjoy. More or less it is the conda-forge (free & open source) equivalent to uv (it actually runs uv for PyPi dependency resolution). Really fast both for PyPi & conda-forge dependency resolution.

This I will still have to explore (as matplotlib does not always auto-scale). Generally there are two options to handle this as of now - users can keep / drop covariates via a function arg, or simply combine many of them into a single "combined" covariate in the estimation process.

August 13, 2025 at 6:50 AM

This I will still have to explore (as matplotlib does not always auto-scale). Generally there are two options to handle this as of now - users can keep / drop covariates via a function arg, or simply combine many of them into a single "combined" covariate in the estimation process.

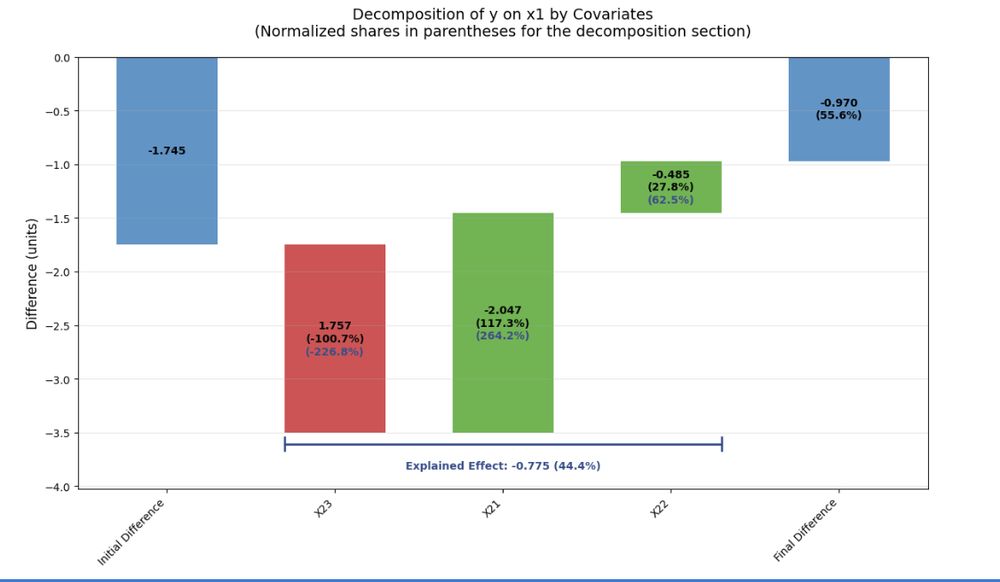

Yes, negative contributions should be handled and would be colored red and should add to the "initial difference" bar

August 13, 2025 at 6:48 AM

Yes, negative contributions should be handled and would be colored red and should add to the "initial difference" bar

My attempt - how to tell you I work in industry without telling you ;) what do you think?

August 12, 2025 at 9:41 PM

My attempt - how to tell you I work in industry without telling you ;) what do you think?

For the ladder I'll make sure that all defaults can be easily changed.

July 31, 2025 at 6:48 PM

For the ladder I'll make sure that all defaults can be easily changed.

I agree - optimally I am looking for default labels that make it immediately clear to the econometricians what is being shown (this is the status quo) but that also allows non-technical stake holder to easily understand the substantive message.

July 31, 2025 at 6:48 PM

I agree - optimally I am looking for default labels that make it immediately clear to the econometricians what is being shown (this is the status quo) but that also allows non-technical stake holder to easily understand the substantive message.

Thanks - I actually control for x21 in the short regression ... will have to think about a good naming convention for this case.

July 31, 2025 at 6:44 PM

Thanks - I actually control for x21 in the short regression ... will have to think about a good naming convention for this case.

Yes this makes a lot of sense. Had also wondered if anyone had seen any great visualizations. Am sold that we should add a plot method. Thanks!

July 31, 2025 at 6:42 PM

Yes this makes a lot of sense. Had also wondered if anyone had seen any great visualizations. Am sold that we should add a plot method. Thanks!

cc @gelbach.bsky.social , and also @nickchk.com, whose blog post (nickchk.substack.com/p/decomposit...) convinced me of the value of decomp methods in industry - maybe you have some tips on effective communication?

July 30, 2025 at 8:38 PM

cc @gelbach.bsky.social , and also @nickchk.com, whose blog post (nickchk.substack.com/p/decomposit...) convinced me of the value of decomp methods in industry - maybe you have some tips on effective communication?

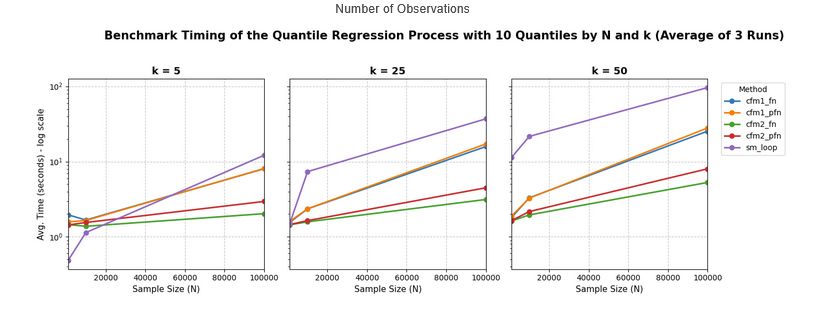

Re fast routines for the quantile regression process - we follow Chernozhukov et al (2019) and their algo's are quite an improvement over "naive" for loops over quantiles:

July 6, 2025 at 10:54 AM

Re fast routines for the quantile regression process - we follow Chernozhukov et al (2019) and their algo's are quite an improvement over "naive" for loops over quantiles:

This release has had 8 new contributors (none of which I think are around here) - thanks all for your help!

July 6, 2025 at 10:26 AM

This release has had 8 new contributors (none of which I think are around here) - thanks all for your help!

You can find the full changelog here: py-econometrics.github.io/pyfixest/cha...

July 6, 2025 at 10:26 AM

You can find the full changelog here: py-econometrics.github.io/pyfixest/cha...

Second, we have added support for 𝐪𝐮𝐚𝐧𝐭𝐢𝐥𝐞 𝐫𝐞𝐠𝐫𝐞𝐬𝐬𝐢𝐨𝐧 based on a Frisch-Newton Solver, including iid, heteroskedastic, and cluster robust standard errors, as well as fast routines for fitting the entire quantile regression process.

July 6, 2025 at 10:26 AM

Second, we have added support for 𝐪𝐮𝐚𝐧𝐭𝐢𝐥𝐞 𝐫𝐞𝐠𝐫𝐞𝐬𝐬𝐢𝐨𝐧 based on a Frisch-Newton Solver, including iid, heteroskedastic, and cluster robust standard errors, as well as fast routines for fitting the entire quantile regression process.