Mark Zandi

@markzandi.bsky.social

Chief Economist of Moody’s Analytics. Host of the Inside Economics podcast. Co-founder of Economy.com. Views expressed here are my own.

Reposted by Mark Zandi

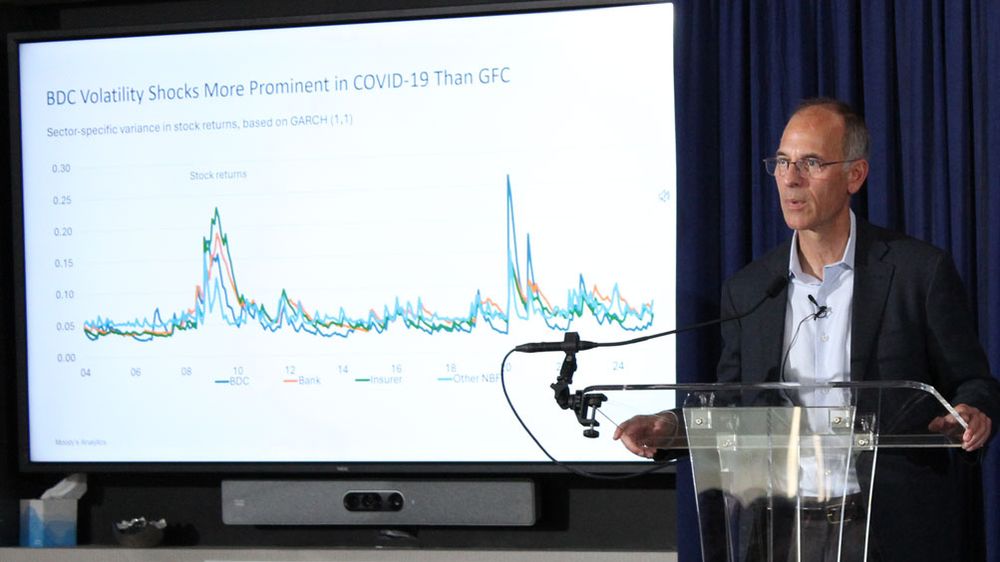

"The shape of the financial system has shifted from where it was in the Great Financial Crisis, from a bank-centric hub-and-spoke system with the banks in the middle and everyone else around the periphery to more of a web, with private credit more central in that web." - @markzandi.bsky.social

September 19, 2025 at 5:36 PM

"The shape of the financial system has shifted from where it was in the Great Financial Crisis, from a bank-centric hub-and-spoke system with the banks in the middle and everyone else around the periphery to more of a web, with private credit more central in that web." - @markzandi.bsky.social

Housing will thus soon be a full-blown headwind to broader economic growth, adding to the growing list of reasons to be worried about the economy’s prospects later this year and early next.

July 14, 2025 at 7:40 PM

Housing will thus soon be a full-blown headwind to broader economic growth, adding to the growing list of reasons to be worried about the economy’s prospects later this year and early next.

House price growth had held up well. But this, too, is changing, as prices have gone sideways and are set to fall. 7% is hammering demand, and there are more listings. Given their demographic and job situations, locked-in homeowners must move. They can only work around these needs for so long.

July 14, 2025 at 7:40 PM

House price growth had held up well. But this, too, is changing, as prices have gone sideways and are set to fall. 7% is hammering demand, and there are more listings. Given their demographic and job situations, locked-in homeowners must move. They can only work around these needs for so long.

Home sales are already uber depressed, but homebuilders providing rate buydowns had been propping sales up. They are giving up. It’s simply too expensive. A big tell is that many builders are delaying their land purchases from the land banks. New home sales, starts, and completions will soon fall.

July 14, 2025 at 7:40 PM

Home sales are already uber depressed, but homebuilders providing rate buydowns had been propping sales up. They are giving up. It’s simply too expensive. A big tell is that many builders are delaying their land purchases from the land banks. New home sales, starts, and completions will soon fall.

One caveat is that seasonally adjusting the UI data is hard given how claims got scrambled in the pandemic. So-called residual seasonality. Non-SA UI claims are not too much higher than in recent years. But if initial claims rise even a bit further in the coming weeks, it's time to buckle up.

June 12, 2025 at 7:40 PM

One caveat is that seasonally adjusting the UI data is hard given how claims got scrambled in the pandemic. So-called residual seasonality. Non-SA UI claims are not too much higher than in recent years. But if initial claims rise even a bit further in the coming weeks, it's time to buckle up.

It also means the economy’s real potential GDP growth – that pace of growth consistent with stable inflation – is much lower. It is currently closer to 1% than the 2% we have come to think of as typical. Think of what this means for everything from asset returns to our already dire fiscal outlook.

June 9, 2025 at 4:54 PM

It also means the economy’s real potential GDP growth – that pace of growth consistent with stable inflation – is much lower. It is currently closer to 1% than the 2% we have come to think of as typical. Think of what this means for everything from asset returns to our already dire fiscal outlook.

The implications of a flagging labor force are disconcerting. It means serious disruptions to businesses that rely on immigrant labor, ranging from construction and agriculture to hospitality and retailing. It also means higher inflation, just when the higher tariffs are set to push up prices.

June 9, 2025 at 4:54 PM

The implications of a flagging labor force are disconcerting. It means serious disruptions to businesses that rely on immigrant labor, ranging from construction and agriculture to hospitality and retailing. It also means higher inflation, just when the higher tariffs are set to push up prices.

Given the new population controls, measuring labor force growth is tricky, but by my calculation, it’s at a standstill. Look to the severe restrictions on immigration. This time last year, the foreign-born labor force was growing 5%. It’s now declining. The native-born labor force remains moribund.

June 9, 2025 at 4:54 PM

Given the new population controls, measuring labor force growth is tricky, but by my calculation, it’s at a standstill. Look to the severe restrictions on immigration. This time last year, the foreign-born labor force was growing 5%. It’s now declining. The native-born labor force remains moribund.

None of this signals recession, but it does signal the job market and economy are increasingly fragile as the fallout from the global trade war intensifies.

June 6, 2025 at 1:49 PM

None of this signals recession, but it does signal the job market and economy are increasingly fragile as the fallout from the global trade war intensifies.

It isn’t great that the job gains are almost entirely in the healthcare and leisure and hospitality industries. At this pace of job growth, unemployment will continue to push higher, and this, despite weaker labor force participation.

June 6, 2025 at 1:49 PM

It isn’t great that the job gains are almost entirely in the healthcare and leisure and hospitality industries. At this pace of job growth, unemployment will continue to push higher, and this, despite weaker labor force participation.

My preferred path: Charter GSEs as gov’t corporations (like pre-1968 Fannie). Add an explicit federal guarantee for stability & lowest mortgage rates. This formalizes the status quo but requires legislation, which makes it a 0% shot.

June 2, 2025 at 2:48 PM

My preferred path: Charter GSEs as gov’t corporations (like pre-1968 Fannie). Add an explicit federal guarantee for stability & lowest mortgage rates. This formalizes the status quo but requires legislation, which makes it a 0% shot.

Scenario 4 - Release w/ Explicit Guarantee (5%): Requires Congress to pass legislation. With a federal guarantee, mortgage rates could fall ~25 bps, benefiting borrowers. But political gridlock makes this unlikely. While this offers stability, the need for legislation makes it a long shot.

June 2, 2025 at 2:48 PM

Scenario 4 - Release w/ Explicit Guarantee (5%): Requires Congress to pass legislation. With a federal guarantee, mortgage rates could fall ~25 bps, benefiting borrowers. But political gridlock makes this unlikely. While this offers stability, the need for legislation makes it a long shot.

Scenario 3 - Release w/o Guarantee (5%): GSEs lose gov’t backing entirely. Rates jump +60–90 bps as investors demand higher returns. The Fed would stop buying their securities, shrinking GSE market share. FHA/private lenders would expand, ironically increasing taxpayer risk through FHA loans.

June 2, 2025 at 2:48 PM

Scenario 3 - Release w/o Guarantee (5%): GSEs lose gov’t backing entirely. Rates jump +60–90 bps as investors demand higher returns. The Fed would stop buying their securities, shrinking GSE market share. FHA/private lenders would expand, ironically increasing taxpayer risk through FHA loans.

Scenario 2 - Release w/ Implicit Guarantee (35%): GSEs would operate like they did pre-2008, but with better capital buffers. Rates would rise +20–40 bps as investors doubt long-term stability. While it’s more likely than other reforms, financial crisis flashbacks make this politically sensitive.

June 2, 2025 at 2:48 PM

Scenario 2 - Release w/ Implicit Guarantee (35%): GSEs would operate like they did pre-2008, but with better capital buffers. Rates would rise +20–40 bps as investors doubt long-term stability. While it’s more likely than other reforms, financial crisis flashbacks make this politically sensitive.

Scenario 1 - Status Quo (50%): GSEs remain in conservatorship. Mortgage rates won’t change. The system works well as-is, with risks already shifted to private investors via credit risk transfers. No legislation is needed, and there’s little incentive to disrupt what’s already functioning smoothly.

June 2, 2025 at 2:48 PM

Scenario 1 - Status Quo (50%): GSEs remain in conservatorship. Mortgage rates won’t change. The system works well as-is, with risks already shifted to private investors via credit risk transfers. No legislation is needed, and there’s little incentive to disrupt what’s already functioning smoothly.

Typically, the soft data leads the hard data into economic downturns. This time is increasingly unlikely to be different.

May 11, 2025 at 4:41 PM

Typically, the soft data leads the hard data into economic downturns. This time is increasingly unlikely to be different.

And while businesses have held the line on layoffs, and thus payrolls continue to increase, that seems set to change, as businesses have already cut back workers’ hours, hiring, and job postings.

May 11, 2025 at 4:41 PM

And while businesses have held the line on layoffs, and thus payrolls continue to increase, that seems set to change, as businesses have already cut back workers’ hours, hiring, and job postings.