Luca Fornaro

@lucafornaro.bsky.social

Martin Wolf and I have studied this amplification effect in a recent paper, and show that it may lead to a state of fiscal stagnation, characterized by a self-sustained vicious cycle of high debt, high fiscal distortions and low productivity growth. Italy may be an example of it.

November 11, 2025 at 2:38 PM

Martin Wolf and I have studied this amplification effect in a recent paper, and show that it may lead to a state of fiscal stagnation, characterized by a self-sustained vicious cycle of high debt, high fiscal distortions and low productivity growth. Italy may be an example of it.

Moreover, there may be an amplification effect at play. Imagine that a government cuts public investments to increase its surplus and stabilize its debt (pretty much what happened during the euro area sovereign debt crisis).

November 11, 2025 at 2:38 PM

Moreover, there may be an amplification effect at play. Imagine that a government cuts public investments to increase its surplus and stabilize its debt (pretty much what happened during the euro area sovereign debt crisis).

There is also evidence suggesting that taxes on investment in intangibles tend to slow down innovation and productivity growth.

While this evidence is preliminary, it thus does look like fiscal policy affects productivity growth.

While this evidence is preliminary, it thus does look like fiscal policy affects productivity growth.

November 11, 2025 at 2:38 PM

There is also evidence suggesting that taxes on investment in intangibles tend to slow down innovation and productivity growth.

While this evidence is preliminary, it thus does look like fiscal policy affects productivity growth.

While this evidence is preliminary, it thus does look like fiscal policy affects productivity growth.

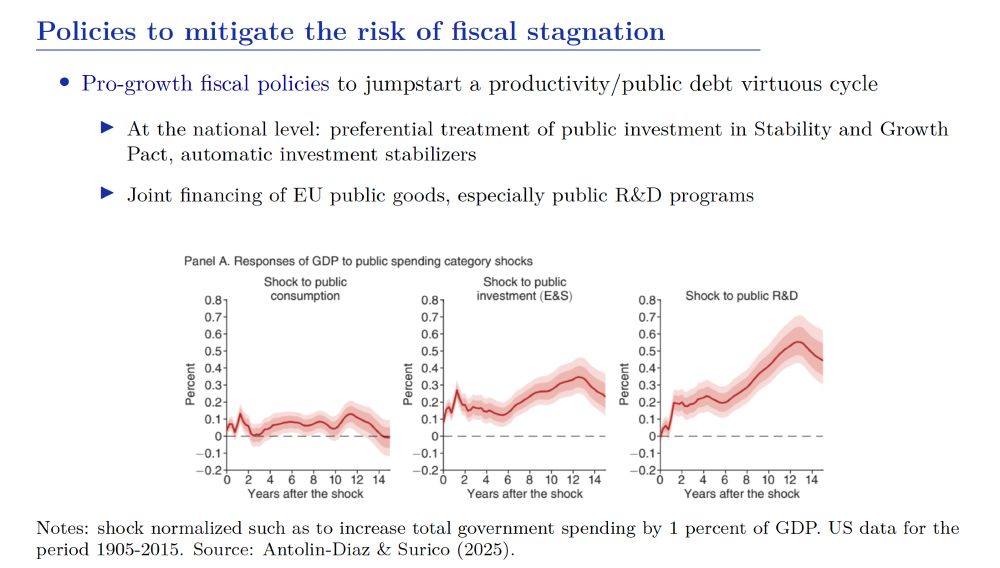

On the empirical side, recent research suggests that public investments matter for productivity. In particular, these two brilliant papers show that higher spending in public R&D crowd in private investment and lead to higher productivity growth in the medium run.

November 11, 2025 at 2:38 PM

On the empirical side, recent research suggests that public investments matter for productivity. In particular, these two brilliant papers show that higher spending in public R&D crowd in private investment and lead to higher productivity growth in the medium run.

Are public debts in the European Union sustainable? This recent article is a great introduction to this topic, I learned a lot by reading it.

One thing that struck me is that debt sustainability analyses typically abstract from the impact of fiscal policy on productivity growth.

One thing that struck me is that debt sustainability analyses typically abstract from the impact of fiscal policy on productivity growth.

November 11, 2025 at 2:38 PM

Are public debts in the European Union sustainable? This recent article is a great introduction to this topic, I learned a lot by reading it.

One thing that struck me is that debt sustainability analyses typically abstract from the impact of fiscal policy on productivity growth.

One thing that struck me is that debt sustainability analyses typically abstract from the impact of fiscal policy on productivity growth.

Finally, what if a country puts a tariff on innovation inputs, perhaps by taxing researchers moving from abroad? This policy may fail spectacularly, by triggering an outflows of innovation goods, which over time will erode the country's technological rents.

October 30, 2025 at 10:40 AM

Finally, what if a country puts a tariff on innovation inputs, perhaps by taxing researchers moving from abroad? This policy may fail spectacularly, by triggering an outflows of innovation goods, which over time will erode the country's technological rents.

Moreover, if the rest of the world chooses to retaliate, the result will be a full-blown trade war. In this scenario, tariffs have no impact on the distribution of technological rents across countries, but they cause big efficiency and output losses.

October 30, 2025 at 10:40 AM

Moreover, if the rest of the world chooses to retaliate, the result will be a full-blown trade war. In this scenario, tariffs have no impact on the distribution of technological rents across countries, but they cause big efficiency and output losses.

But this strategy has several drawbacks. First, reducing imports of foreign high-tech goods generates productivity and output losses. Second, even if import tariffs may increase national welfare, this comes at the expense of even larger welfare losses in the rest of the world.

October 30, 2025 at 10:40 AM

But this strategy has several drawbacks. First, reducing imports of foreign high-tech goods generates productivity and output losses. Second, even if import tariffs may increase national welfare, this comes at the expense of even larger welfare losses in the rest of the world.

Tariffs on imports of high-tech goods may be used to steal technological rents from the rest of the world. Intuitively, tariffs reduce the profitability of foreign high-tech firms, causing a flow of innovation inputs and technological rents to the country imposing the tariffs.

October 30, 2025 at 10:40 AM

Tariffs on imports of high-tech goods may be used to steal technological rents from the rest of the world. Intuitively, tariffs reduce the profitability of foreign high-tech firms, causing a flow of innovation inputs and technological rents to the country imposing the tariffs.

From a national perspective, importing innovation inputs yields technological rents, because of the positive knowledge spillovers that they create. So countries have an incentive to compete for technological hegemony, i.e. to become net importers of innovation inputs.

October 30, 2025 at 10:40 AM

From a national perspective, importing innovation inputs yields technological rents, because of the positive knowledge spillovers that they create. So countries have an incentive to compete for technological hegemony, i.e. to become net importers of innovation inputs.

To innovate, high-tech firms need specialized 'innovation inputs', such as researchers and venture capital. Building a strong high-tech cluster requires importing innovation inputs from abroad. Think of foreign researchers working for Big Tech firms in the Silicon Valley.

October 30, 2025 at 10:40 AM

To innovate, high-tech firms need specialized 'innovation inputs', such as researchers and venture capital. Building a strong high-tech cluster requires importing innovation inputs from abroad. Think of foreign researchers working for Big Tech firms in the Silicon Valley.

We start from the observation that high-tech clusters generate technological rents for the countries hosting them. Not only high-tech firms are highly profitable, but their innovation activities trigger positive knowledge spillovers to other domestic firms.

October 30, 2025 at 10:40 AM

We start from the observation that high-tech clusters generate technological rents for the countries hosting them. Not only high-tech firms are highly profitable, but their innovation activities trigger positive knowledge spillovers to other domestic firms.

We provide a framework connecting trade policies to innovation and technological hegemony. Our model focuses on high-tech firms that invest heavily in R&D and other intangibles. Nowadays, these firms play a key role in international trade.

October 30, 2025 at 10:40 AM

We provide a framework connecting trade policies to innovation and technological hegemony. Our model focuses on high-tech firms that invest heavily in R&D and other intangibles. Nowadays, these firms play a key role in international trade.

How will tariffs affect innovation in the US and abroad? Shall the EU use tariffs to protect its high-tech industries? Should the rise in Chinese exports of high-tech goods worry the rest of the world?

We tackle these issues in a new paper on Tariffs and Technological Hegemony.

We tackle these issues in a new paper on Tariffs and Technological Hegemony.

October 30, 2025 at 10:40 AM

How will tariffs affect innovation in the US and abroad? Shall the EU use tariffs to protect its high-tech industries? Should the rise in Chinese exports of high-tech goods worry the rest of the world?

We tackle these issues in a new paper on Tariffs and Technological Hegemony.

We tackle these issues in a new paper on Tariffs and Technological Hegemony.

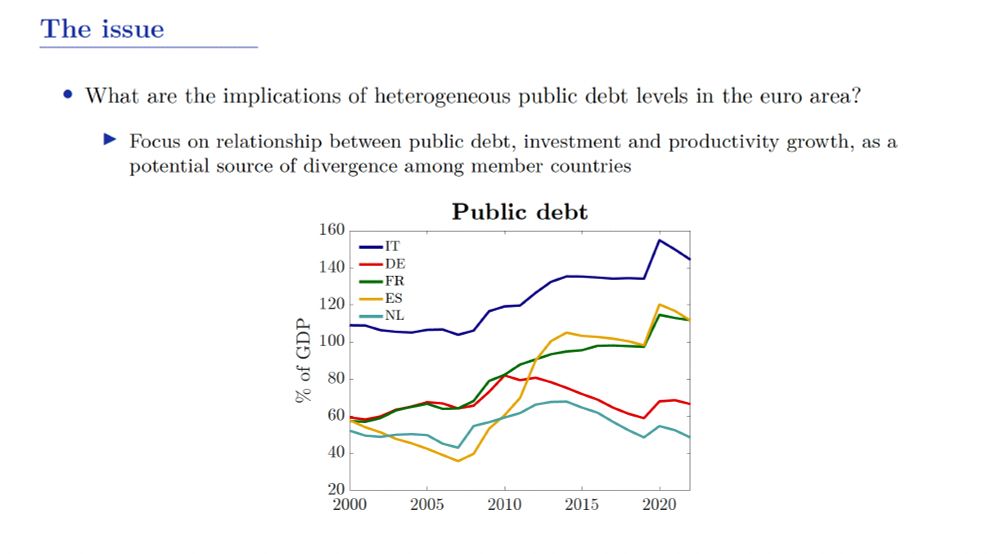

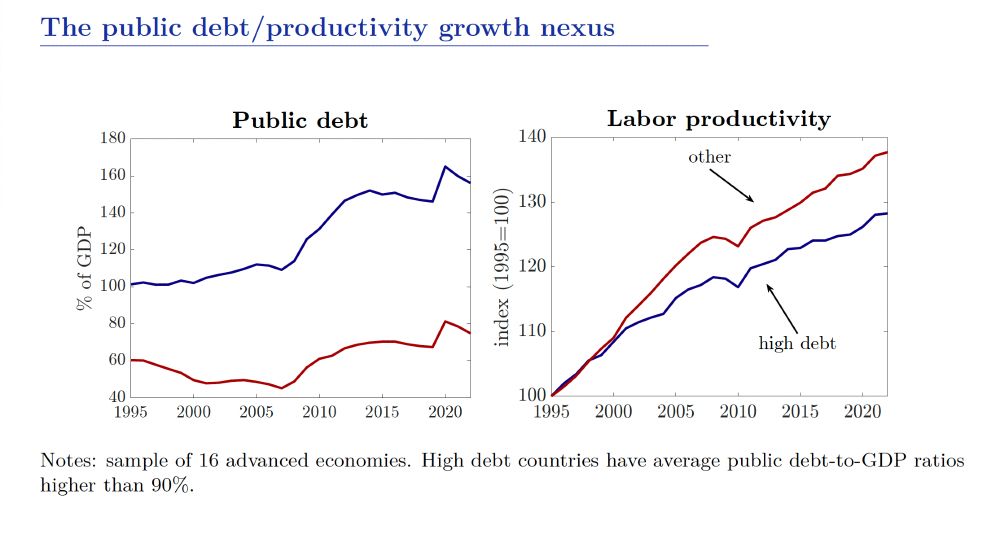

Some thoughts on the interactions between public debt, public investments and productivity growth in the euro area. Key risk is that the union ends up being split between a fiscally sound/high growth block and a fiscally stagnant one.

www.ecb.europa.eu/pub/pdf/sint...

www.ecb.europa.eu/pub/pdf/sint...

September 23, 2025 at 8:45 AM

Some thoughts on the interactions between public debt, public investments and productivity growth in the euro area. Key risk is that the union ends up being split between a fiscally sound/high growth block and a fiscally stagnant one.

www.ecb.europa.eu/pub/pdf/sint...

www.ecb.europa.eu/pub/pdf/sint...

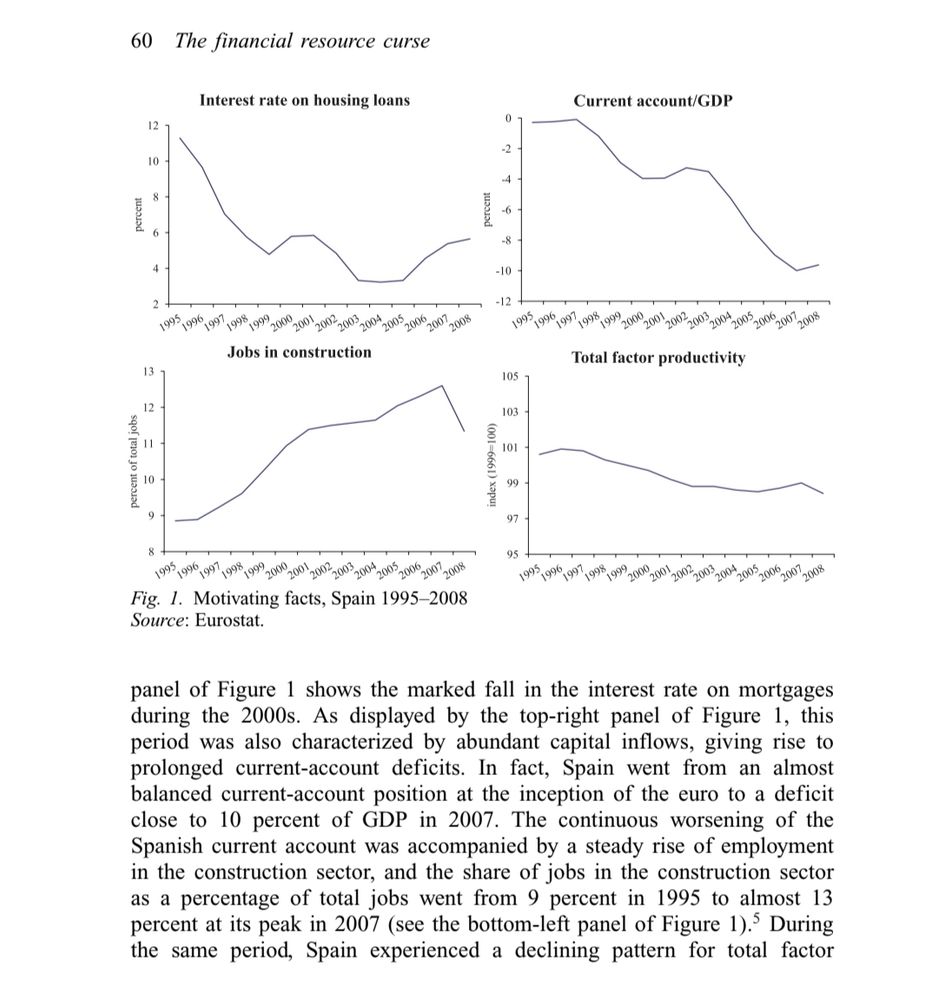

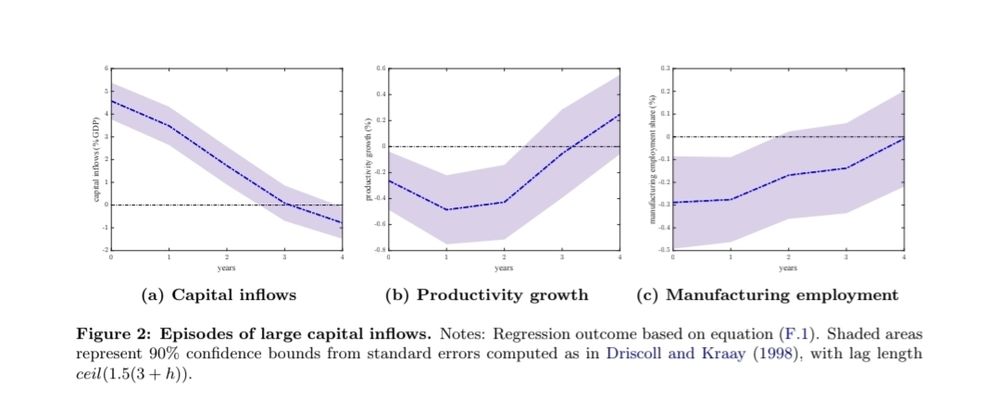

Spain during the 2000s is a good example of these dynamics, but productivity growth slowdowns during large surges in trade deficits are quite common.

July 31, 2025 at 4:35 AM

Spain during the 2000s is a good example of these dynamics, but productivity growth slowdowns during large surges in trade deficits are quite common.

Deeply honored to have participated in a panel at the

@ecb.europa.eu Forum in Sintra. My remarks focused on the risk that high legacy debt may push part of the euro area into fiscal stagnation, and how a pro-growth approach to fiscal policy can mitigate this risk.

@ecb.europa.eu Forum in Sintra. My remarks focused on the risk that high legacy debt may push part of the euro area into fiscal stagnation, and how a pro-growth approach to fiscal policy can mitigate this risk.

July 3, 2025 at 10:52 AM

Deeply honored to have participated in a panel at the

@ecb.europa.eu Forum in Sintra. My remarks focused on the risk that high legacy debt may push part of the euro area into fiscal stagnation, and how a pro-growth approach to fiscal policy can mitigate this risk.

@ecb.europa.eu Forum in Sintra. My remarks focused on the risk that high legacy debt may push part of the euro area into fiscal stagnation, and how a pro-growth approach to fiscal policy can mitigate this risk.

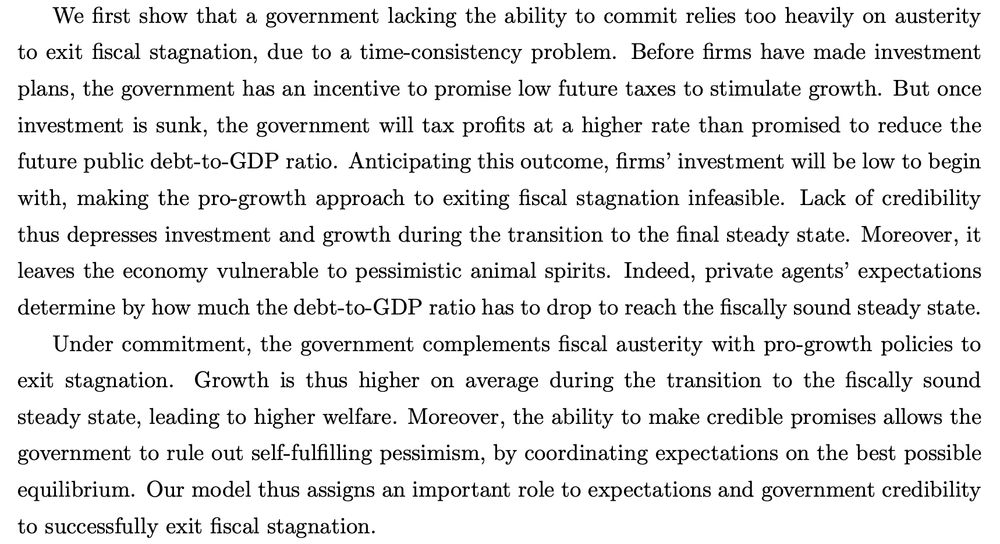

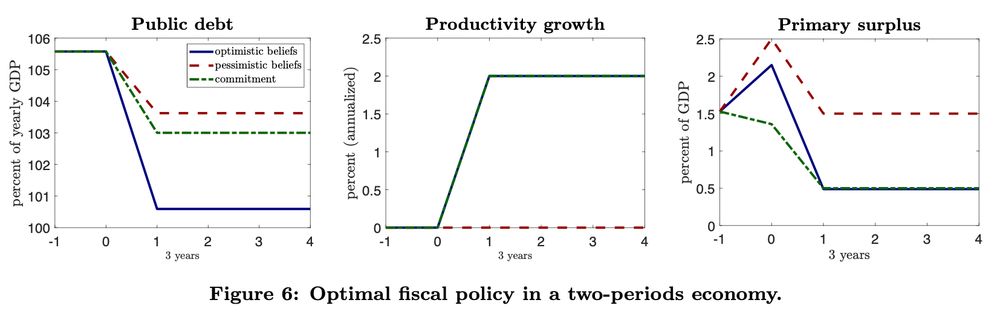

Pro-growth policies are more appealing. Credibly promising to lower fiscal distortions boosts investment and growth. High growth, in turn, reduces the debt-to-GDP ratio. But, due to a time-consistency problem, this strategy requires commitment on the side of the government.

April 21, 2025 at 4:48 AM

Pro-growth policies are more appealing. Credibly promising to lower fiscal distortions boosts investment and growth. High growth, in turn, reduces the debt-to-GDP ratio. But, due to a time-consistency problem, this strategy requires commitment on the side of the government.

Austerity, in theory, is simple. Increase the primary surplus today to lower public debt in the future. But austerity discourages investment and growth. So exiting stagnation through austerity is painful and takes a long time, especially if animal spirits are pessimistic.

April 21, 2025 at 4:48 AM

Austerity, in theory, is simple. Increase the primary surplus today to lower public debt in the future. But austerity discourages investment and growth. So exiting stagnation through austerity is painful and takes a long time, especially if animal spirits are pessimistic.

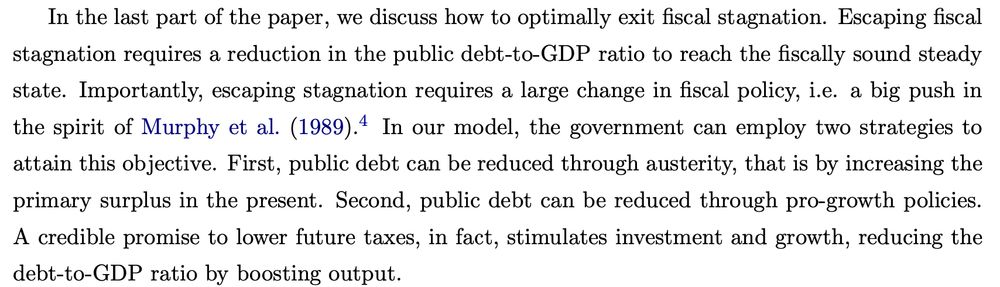

How to optimally escape fiscal stagnation? First, marginal policy changes won't do it. Exiting stagnation requires a big push, i.e. a large change in fiscal policy to reduce the public debt-to-GDP ratio. Two strategies to do so: fiscal austerity and pro-growth policies.

April 21, 2025 at 4:48 AM

How to optimally escape fiscal stagnation? First, marginal policy changes won't do it. Exiting stagnation requires a big push, i.e. a large change in fiscal policy to reduce the public debt-to-GDP ratio. Two strategies to do so: fiscal austerity and pro-growth policies.

A shift from fiscal soundness to stagnation can be interpreted as the result of self-defeating austerity. During the transition toward fiscal stagnation, in fact, high primary surpluses depress growth so much that the debt-to-GDP ratio may not decline, or even rise.

April 21, 2025 at 4:48 AM

A shift from fiscal soundness to stagnation can be interpreted as the result of self-defeating austerity. During the transition toward fiscal stagnation, in fact, high primary surpluses depress growth so much that the debt-to-GDP ratio may not decline, or even rise.

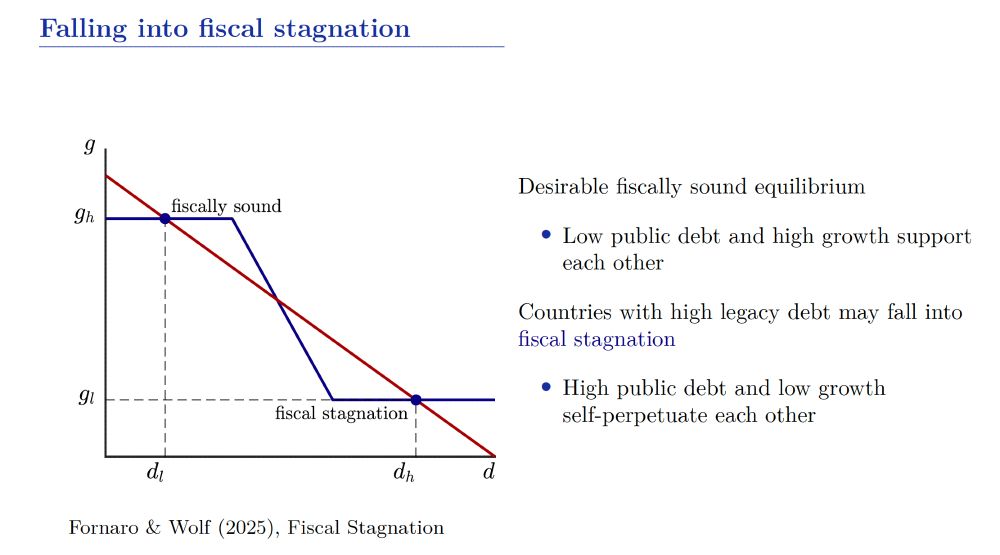

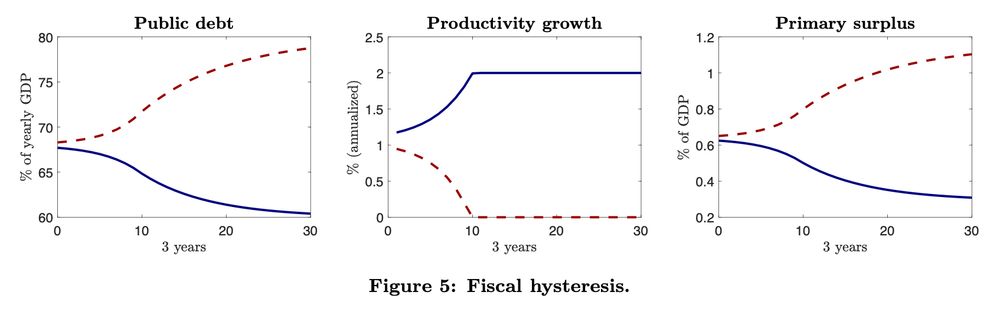

What makes the economy fall into fiscal stagnation? This may happen through hysteresis effects, i.e. a moderate negative fiscal shock may lead to a sharp deterioration of the long-run fiscal outlook. But pessimistic animal spirits can drive the economy into fiscal stagnation too.

April 21, 2025 at 4:48 AM

What makes the economy fall into fiscal stagnation? This may happen through hysteresis effects, i.e. a moderate negative fiscal shock may lead to a sharp deterioration of the long-run fiscal outlook. But pessimistic animal spirits can drive the economy into fiscal stagnation too.

Due to this feedback loop, the economy may enter a fiscal stagnation steady state, i.e. a self-perpetuating state of high fiscal distortions and weak growth. Technically, our model has multiple steady states. so a fiscally sound and a fiscal stagnation steady state may coexist.

April 21, 2025 at 4:48 AM

Due to this feedback loop, the economy may enter a fiscal stagnation steady state, i.e. a self-perpetuating state of high fiscal distortions and weak growth. Technically, our model has multiple steady states. so a fiscally sound and a fiscal stagnation steady state may coexist.

Our model suggests that this is a risk, because of a feedback loop between fiscal policy and growth. Large primary surpluses and high fiscal distortions depress investment and growth. But low growth calls for high primary surpluses to ensure the sustainability of public debt...

April 21, 2025 at 4:48 AM

Our model suggests that this is a risk, because of a feedback loop between fiscal policy and growth. Large primary surpluses and high fiscal distortions depress investment and growth. But low growth calls for high primary surpluses to ensure the sustainability of public debt...