Joscha Wullweber

@jwullweber.bsky.social

Heisenberg-Professor of PolEcon, Transformation and Sustainability, Director of [tra:ce], Univ. Witten/Herdecke. Strong focus on IPE, global finance, central bank politics, money. Also active at mastodon.world/@JWullweber

Disclaimer: Many activities necessary for the green transition will never be bankable, and therefore will never be attractive for financial investors. As a result, the state should directly provide the necessary financing.

You can find our full policy report here: www.uni-wh.de/en/your-camp...

You can find our full policy report here: www.uni-wh.de/en/your-camp...

[tra:ce] Policy Report

Financing the green transition: Increasing bankability, phasing out carbon investments and funding ‘never bankable’ activities

www.uni-wh.de

July 11, 2025 at 1:10 PM

Disclaimer: Many activities necessary for the green transition will never be bankable, and therefore will never be attractive for financial investors. As a result, the state should directly provide the necessary financing.

You can find our full policy report here: www.uni-wh.de/en/your-camp...

You can find our full policy report here: www.uni-wh.de/en/your-camp...

The figure illustrates how financial policies should function: Green investments require derisking policies and better financing conditions to become bankable. For greenhouse gas-emitting investments, policies should increase risk and decrease returns in order to reduce their bankability.

July 11, 2025 at 1:10 PM

The figure illustrates how financial policies should function: Green investments require derisking policies and better financing conditions to become bankable. For greenhouse gas-emitting investments, policies should increase risk and decrease returns in order to reduce their bankability.

#5 @naguila.bsky.social @paulahaufe.bsky.social @riccardobaioni.bsky.social @janinaurban @simonschairer.bsky.social @floriankern @janfichtner.bsky.social

July 3, 2025 at 6:01 AM

#5 @naguila.bsky.social @paulahaufe.bsky.social @riccardobaioni.bsky.social @janinaurban @simonschairer.bsky.social @floriankern @janfichtner.bsky.social

#4 This taxonomy forms the basis for the projects’ policy recommendations that can increase the bankability of not-yet bankable firms and projects, decrease the bankability of high-GHG emitting ones, and expand financing for never bankable activities. @wbgu.bsky.social @ioew.bsky.social

July 3, 2025 at 6:01 AM

#4 This taxonomy forms the basis for the projects’ policy recommendations that can increase the bankability of not-yet bankable firms and projects, decrease the bankability of high-GHG emitting ones, and expand financing for never bankable activities. @wbgu.bsky.social @ioew.bsky.social

#3 In other words, many green firms and projects are considered as ‘non-bankable’. Based on our analysis, we propose a classification that considers two criteria: 1) Is the investment green or does it generate high GHG emissions? 2) Is it bankable, not yet bankable, or never bankable?

July 3, 2025 at 6:01 AM

#3 In other words, many green firms and projects are considered as ‘non-bankable’. Based on our analysis, we propose a classification that considers two criteria: 1) Is the investment green or does it generate high GHG emissions? 2) Is it bankable, not yet bankable, or never bankable?

#2 We show that the problem is not the lack of capital, but the lack of bankable green projects. Increases in green lending and investments by banks and other financial institutions remain negligible because green investments fail to meet the desired risk-return profiles of investors.

July 3, 2025 at 6:01 AM

#2 We show that the problem is not the lack of capital, but the lack of bankable green projects. Increases in green lending and investments by banks and other financial institutions remain negligible because green investments fail to meet the desired risk-return profiles of investors.

Reposted by Joscha Wullweber

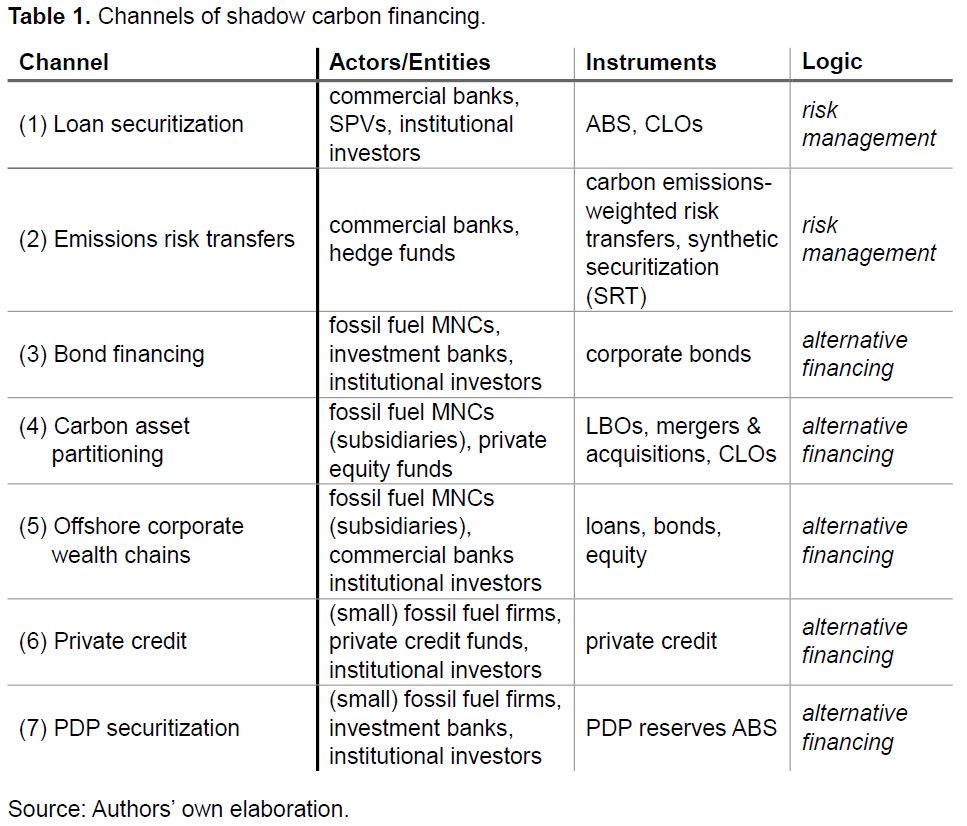

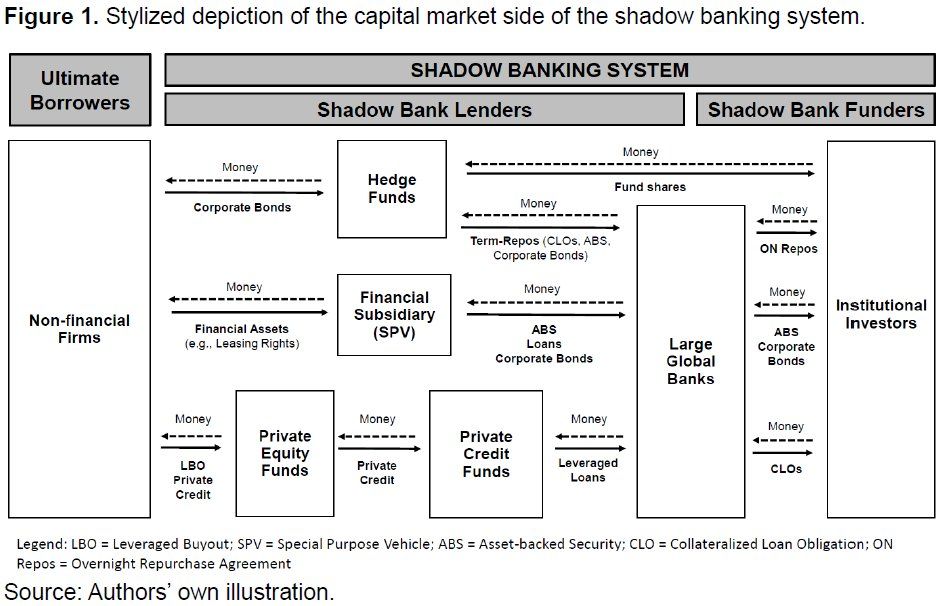

(1) loan securitization, (2) emissions risk transfers, (3) bond financing, (4) carbon asset partitioning, (5) offshore corporate wealth chains, (6) private credit, and (7) proved developed producing reserves securitization.

April 1, 2025 at 10:34 AM

(1) loan securitization, (2) emissions risk transfers, (3) bond financing, (4) carbon asset partitioning, (5) offshore corporate wealth chains, (6) private credit, and (7) proved developed producing reserves securitization.

Reposted by Joscha Wullweber

Drawing on qualitative expert interviews and financial market data, the paper explains how the offshore-shadow-banking nexus hampers the green transition by introducing the concept of ‘shadow carbon financing’, which can operate through the following seven channels:

April 1, 2025 at 10:34 AM

Drawing on qualitative expert interviews and financial market data, the paper explains how the offshore-shadow-banking nexus hampers the green transition by introducing the concept of ‘shadow carbon financing’, which can operate through the following seven channels:

Reposted by Joscha Wullweber

These blind spots seriously undermine regulatory efficacy because offshore finance enables the obfuscation of financial flows, while shadow banking facilitates alternative financing to high carbon-emitting firms.

April 1, 2025 at 10:34 AM

These blind spots seriously undermine regulatory efficacy because offshore finance enables the obfuscation of financial flows, while shadow banking facilitates alternative financing to high carbon-emitting firms.

Reposted by Joscha Wullweber

Recent years saw regulatory efforts to steer the financial system towards financing the transition to a net-zero economy and phase out carbon financing. However, EU regulation has left the nexus of offshore finance and the shadow banking system untouched.

April 1, 2025 at 10:34 AM

Recent years saw regulatory efforts to steer the financial system towards financing the transition to a net-zero economy and phase out carbon financing. However, EU regulation has left the nexus of offshore finance and the shadow banking system untouched.