@jadhazell.bsky.social

London School of Economics, macro professor

But consistent with our framework, the solvency of the pension fund sector improved during the liquidity crisis.

Here’s a link to the paper. Comments welcome!

jadhazell.github.io/website/LASH...

(11/11)

Here’s a link to the paper. Comments welcome!

jadhazell.github.io/website/LASH...

(11/11)

jadhazell.github.io

December 16, 2024 at 12:02 PM

But consistent with our framework, the solvency of the pension fund sector improved during the liquidity crisis.

Here’s a link to the paper. Comments welcome!

jadhazell.github.io/website/LASH...

(11/11)

Here’s a link to the paper. Comments welcome!

jadhazell.github.io/website/LASH...

(11/11)

We show that institutions with ex- ante larger LASH risk sold substantially more bonds during the crisis. Bond sales exacerbated the crisis further by contributing to interest rates. (10/11)

December 16, 2024 at 12:02 PM

We show that institutions with ex- ante larger LASH risk sold substantially more bonds during the crisis. Bond sales exacerbated the crisis further by contributing to interest rates. (10/11)

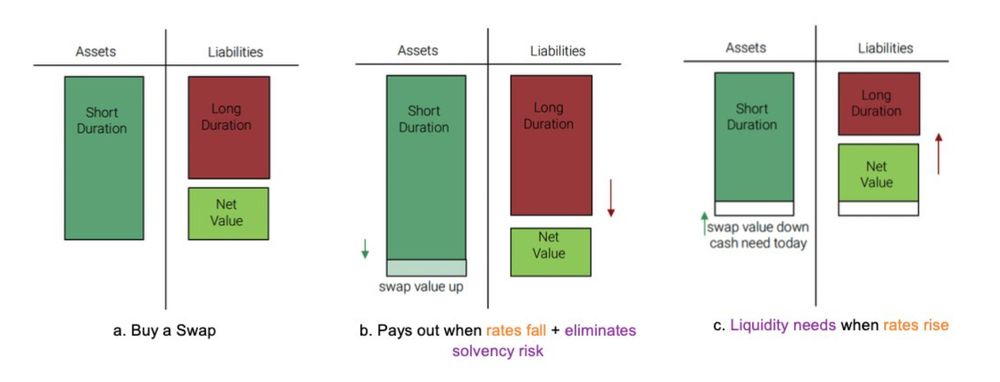

3) When rates rise sharply, LASH risk leads to liquidity crises—i.e. the UK bond market crisis of September and October 2022. The crisis involved rising interest rates, margin calls, and bond sales by pension funds. (9/11)

December 16, 2024 at 12:02 PM

3) When rates rise sharply, LASH risk leads to liquidity crises—i.e. the UK bond market crisis of September and October 2022. The crisis involved rising interest rates, margin calls, and bond sales by pension funds. (9/11)

2) Low interest rates cause LASH risk. In the time series, low interest rates associate with high LASH risk. In the cross section, institutions that are more exposed to falling rates take on more LASH risk. (8/11)

December 16, 2024 at 12:02 PM

2) Low interest rates cause LASH risk. In the time series, low interest rates associate with high LASH risk. In the cross section, institutions that are more exposed to falling rates take on more LASH risk. (8/11)

LASH risk is big: at the peak, a 100bps rise in interest rates would have generated liquidity needs close to the liquid asset holdings of the entire UK pension fund and insurance sector. (7/11)

December 16, 2024 at 11:57 AM

LASH risk is big: at the peak, a 100bps rise in interest rates would have generated liquidity needs close to the liquid asset holdings of the entire UK pension fund and insurance sector. (7/11)

We make three main contributions.

1) We show that non-banks take on LASH risk to hedge solvency risk. We measure LASH risk for pound sterling interest rate contracts held by UK non-banks, using amazing supervisory data. (6/11)

1) We show that non-banks take on LASH risk to hedge solvency risk. We measure LASH risk for pound sterling interest rate contracts held by UK non-banks, using amazing supervisory data. (6/11)

December 16, 2024 at 11:57 AM

We make three main contributions.

1) We show that non-banks take on LASH risk to hedge solvency risk. We measure LASH risk for pound sterling interest rate contracts held by UK non-banks, using amazing supervisory data. (6/11)

1) We show that non-banks take on LASH risk to hedge solvency risk. We measure LASH risk for pound sterling interest rate contracts held by UK non-banks, using amazing supervisory data. (6/11)

But when rates rise, the value of the swap falls, and the fund must pay liquid assets (“margin”) to their counterparty. The margin requirement is LASH risk, which materializes even as the solvency of the fund improves with rising rates. (5/11)

December 16, 2024 at 11:57 AM

But when rates rise, the value of the swap falls, and the fund must pay liquid assets (“margin”) to their counterparty. The margin requirement is LASH risk, which materializes even as the solvency of the fund improves with rising rates. (5/11)

Imagine a pension fund with long-duration liabilities and shorter duration assets. Falling rates lowers solvency since liabilities rise more than assets. The fund can hedge this solvency risk using an interest rate swap, whose value rises when rates fall. (4/11)

December 16, 2024 at 11:56 AM

Imagine a pension fund with long-duration liabilities and shorter duration assets. Falling rates lowers solvency since liabilities rise more than assets. The fund can hedge this solvency risk using an interest rate swap, whose value rises when rates fall. (4/11)

Institutions take LASH risk when they hedge against losses, using strategies that require liquidity as solvency improves. LASH is different from most other forms of liquidity risk, which materialize when solvency gets worse. (3/11)

December 16, 2024 at 11:56 AM

Institutions take LASH risk when they hedge against losses, using strategies that require liquidity as solvency improves. LASH is different from most other forms of liquidity risk, which materialize when solvency gets worse. (3/11)

We’re motivated by recent liquidity crises, such as the pandemic crisis of Spring 2020 or the 2022 UK bond market crisis. We link these crises to Liquidity After Solvency Hedging or “LASH” risk. (2/11)

December 16, 2024 at 11:56 AM

We’re motivated by recent liquidity crises, such as the pandemic crisis of Spring 2020 or the 2022 UK bond market crisis. We link these crises to Liquidity After Solvency Hedging or “LASH” risk. (2/11)