Jonathan Heathcote

@heathcote.bsky.social

Economist. Macro, inequality, public finance, international finance, asset pricing, labor.

https://www.jonathanheathcote.com

https://www.jonathanheathcote.com

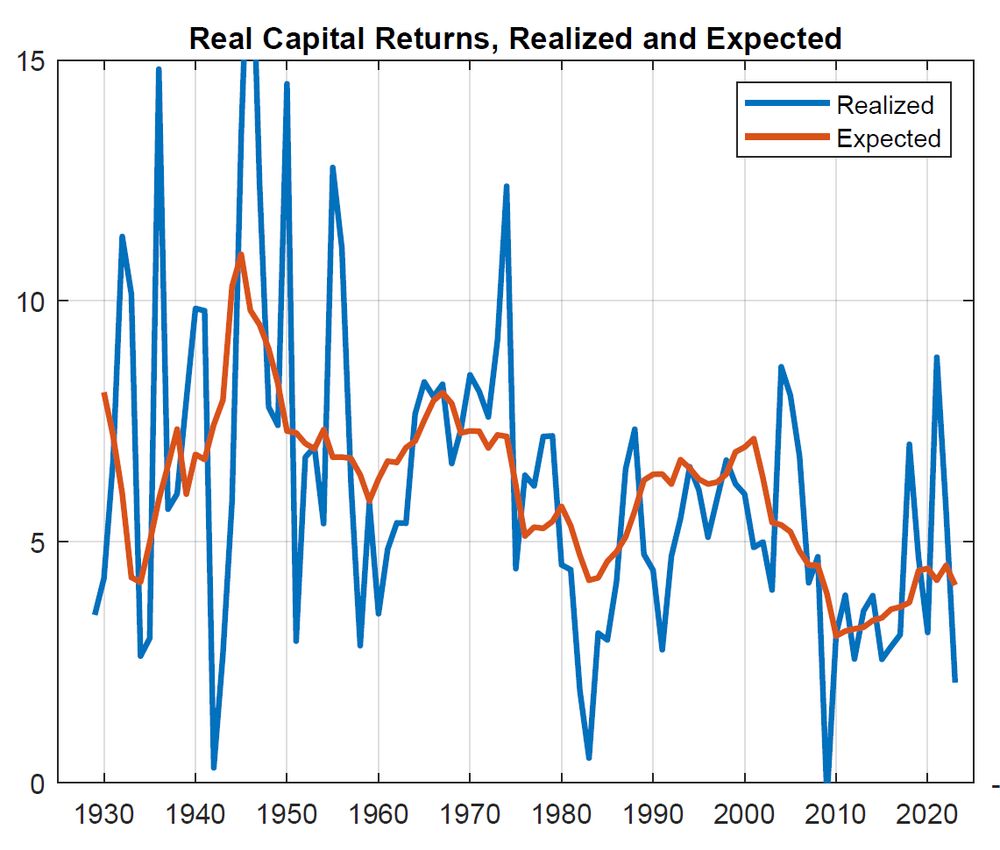

Longer time series for perspective.

April 6, 2025 at 7:51 PM

Longer time series for perspective.

Then we ask whether the observed path for investment is consistent with the required return to capital investment being equal, date by date, to the expected return estimated from the finance model. We find that it is, given a plausible path for expected productivity growth. 8/

February 11, 2025 at 1:45 AM

Then we ask whether the observed path for investment is consistent with the required return to capital investment being equal, date by date, to the expected return estimated from the finance model. We find that it is, given a plausible path for expected productivity growth. 8/

We compare the time series for expected returns from our finance model with a series for realized returns to capital estimated from our macro model (given time series for taxes, depreciation, labor’s share of value-added etc). The two track closely. 7/

February 11, 2025 at 1:45 AM

We compare the time series for expected returns from our finance model with a series for realized returns to capital estimated from our macro model (given time series for taxes, depreciation, labor’s share of value-added etc). The two track closely. 7/

Why do we find this? Part of the explanation is that our macro-model consistent firm income measure — free cash flow — looks quite different to dividends paid. At low frequency, valuations and free cash flow clearly co-move, pointing to a link between the two.6/

February 11, 2025 at 1:45 AM

Why do we find this? Part of the explanation is that our macro-model consistent firm income measure — free cash flow — looks quite different to dividends paid. At low frequency, valuations and free cash flow clearly co-move, pointing to a link between the two.6/

The paper’s first result is that our estimated asset pricing model interprets fluctuations in valuations quite differently. We find that fluctuations over the past 100 years mostly reflect fluctuations in long run expected free cash flow! (x in the plot below) 5/

February 11, 2025 at 1:45 AM

The paper’s first result is that our estimated asset pricing model interprets fluctuations in valuations quite differently. We find that fluctuations over the past 100 years mostly reflect fluctuations in long run expected free cash flow! (x in the plot below) 5/

On top of that, conventional wisdom in finance is that volatility in valuations mostly reflects fluctuations in the expected return that firm owners require (rather than time variation in expected cash flow). If firm owners’ required returns are volatile, why is their capital invested so smooth? 4/

February 11, 2025 at 1:45 AM

On top of that, conventional wisdom in finance is that volatility in valuations mostly reflects fluctuations in the expected return that firm owners require (rather than time variation in expected cash flow). If firm owners’ required returns are volatile, why is their capital invested so smooth? 4/

Valuations are volatile, while the aggregate capital stock is smooth. That poses a challenge to reconciling macro and finance. 3/

February 11, 2025 at 1:45 AM

Valuations are volatile, while the aggregate capital stock is smooth. That poses a challenge to reconciling macro and finance. 3/

We study valuations of US corporations from 1929 onward using 2 models: an asset pricing model, and a stochastic growth model that incorporates factorless income. We fit these models to data from the Integrated Macroeconomic Accounts, focusing on free cash flow as a measure of income. 2/

February 11, 2025 at 1:45 AM

We study valuations of US corporations from 1929 onward using 2 models: an asset pricing model, and a stochastic growth model that incorporates factorless income. We fit these models to data from the Integrated Macroeconomic Accounts, focusing on free cash flow as a measure of income. 2/

The housing supply is not fixed in the short run. There are lots of people who could rent out second homes, ADUs, or put property on AirBnb, if they felt it would be worthwhile financially.

January 14, 2025 at 4:17 PM

The housing supply is not fixed in the short run. There are lots of people who could rent out second homes, ADUs, or put property on AirBnb, if they felt it would be worthwhile financially.

I suspect low US taxes and agglomeration effects are big drivers of US dynamism. With respect specifically to Finland, Nokia screwed up.

January 12, 2025 at 7:06 PM

I suspect low US taxes and agglomeration effects are big drivers of US dynamism. With respect specifically to Finland, Nokia screwed up.

They did have access to venture capital — ie some other rich people. But that seems to also exist to some extent in Scandinavia (I watched The Playlist!)

January 12, 2025 at 7:05 PM

They did have access to venture capital — ie some other rich people. But that seems to also exist to some extent in Scandinavia (I watched The Playlist!)

@fatihguvenen.bsky.social is arguing that entrepreneurs need to have skin in the game (i.e they need wealth so they can have an equity stake). That makes sense But many of the richest Americans are self-made — they built big businesses without much initial wealth.

January 12, 2025 at 7:02 PM

@fatihguvenen.bsky.social is arguing that entrepreneurs need to have skin in the game (i.e they need wealth so they can have an equity stake). That makes sense But many of the richest Americans are self-made — they built big businesses without much initial wealth.

And what is the answer?

December 14, 2024 at 8:27 PM

And what is the answer?

Macro without macro.

December 10, 2024 at 12:37 AM

Macro without macro.

I don’t quite understand the table. If I look at highly selective colleges, enrollment for every sub-group declined by more than enrollment for all. Perhaps there is a ‘did not declare race’ group, whose enrollment rose.

December 3, 2024 at 2:02 PM

I don’t quite understand the table. If I look at highly selective colleges, enrollment for every sub-group declined by more than enrollment for all. Perhaps there is a ‘did not declare race’ group, whose enrollment rose.