Fade Dance

@fadedance.bsky.social

Consilience, Frameworks, Inflection Points.

Exploring ideas and expanding horizons.

Exploring ideas and expanding horizons.

What part of the most legendary slide in an investor slide deck of all time isn't clear?

December 16, 2024 at 6:24 PM

What part of the most legendary slide in an investor slide deck of all time isn't clear?

"So there isn’t a need for them to de-risk per se. However, it looks like crowding performance could be peaking again, which doesn’t bode well for crowded longs going forward" (JPM pos intelligence team)

December 14, 2024 at 6:07 PM

"So there isn’t a need for them to de-risk per se. However, it looks like crowding performance could be peaking again, which doesn’t bode well for crowded longs going forward" (JPM pos intelligence team)

frothy market, of course, but there's a strong narrative here. Quantum computing exponentially scales and it's starting to break out of the lab environment into the real world. That's the backdrop. Then there is a catalyst which directly ties into what you screenshotted.

December 11, 2024 at 7:50 PM

frothy market, of course, but there's a strong narrative here. Quantum computing exponentially scales and it's starting to break out of the lab environment into the real world. That's the backdrop. Then there is a catalyst which directly ties into what you screenshotted.

Don't have the up-to-date data for the S&P on hand, but here is Gold. That's a typical example of a maxed out CTA exposure, Where down markets cause them to puke and even up markets generate very little further buying since their exposure is at the top of the band. S&P Future exposure included too.

December 11, 2024 at 12:05 AM

Don't have the up-to-date data for the S&P on hand, but here is Gold. That's a typical example of a maxed out CTA exposure, Where down markets cause them to puke and even up markets generate very little further buying since their exposure is at the top of the band. S&P Future exposure included too.

Essential (company) had this prototyped before they closed their doors.

December 10, 2024 at 11:07 PM

Essential (company) had this prototyped before they closed their doors.

Falling/cheaper skew helps with the collar proposition when it comes to looking at hedges and or limiting downside.

December 6, 2024 at 9:03 PM

Falling/cheaper skew helps with the collar proposition when it comes to looking at hedges and or limiting downside.

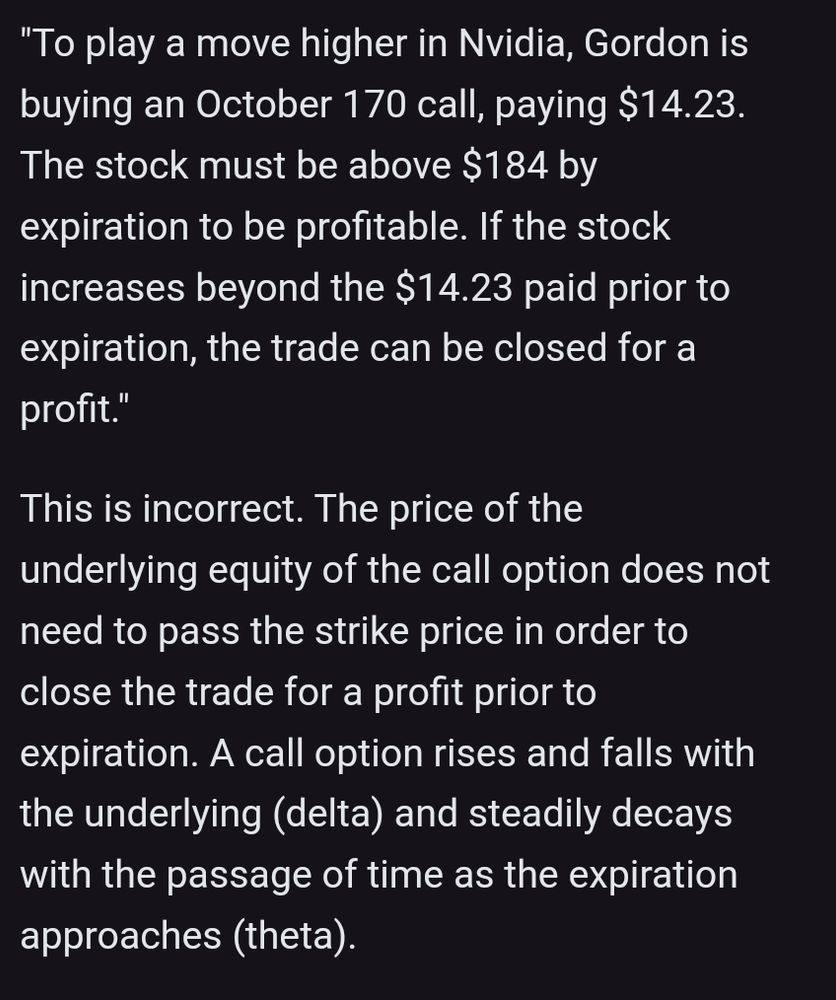

I had to send a correction to their "option team" because they didn't understand call spreads, while recommending that readers put on a call spread...

Chat GPT would be better at generating trade ideas.

To be fair, they did respond. Maybe they have moved up to freshman college level.

Chat GPT would be better at generating trade ideas.

To be fair, they did respond. Maybe they have moved up to freshman college level.

December 6, 2024 at 8:45 PM

I had to send a correction to their "option team" because they didn't understand call spreads, while recommending that readers put on a call spread...

Chat GPT would be better at generating trade ideas.

To be fair, they did respond. Maybe they have moved up to freshman college level.

Chat GPT would be better at generating trade ideas.

To be fair, they did respond. Maybe they have moved up to freshman college level.

The Great Depression was caused by a Great Swan.

December 6, 2024 at 1:21 AM

The Great Depression was caused by a Great Swan.

Now there was a legendarily stable government system with checks and balances. Obviously of its time, but I'd take that DOGE over this one.

December 3, 2024 at 11:49 PM

Now there was a legendarily stable government system with checks and balances. Obviously of its time, but I'd take that DOGE over this one.

My favorite visualization of this is fairly simple:

December 1, 2024 at 3:20 AM

My favorite visualization of this is fairly simple:

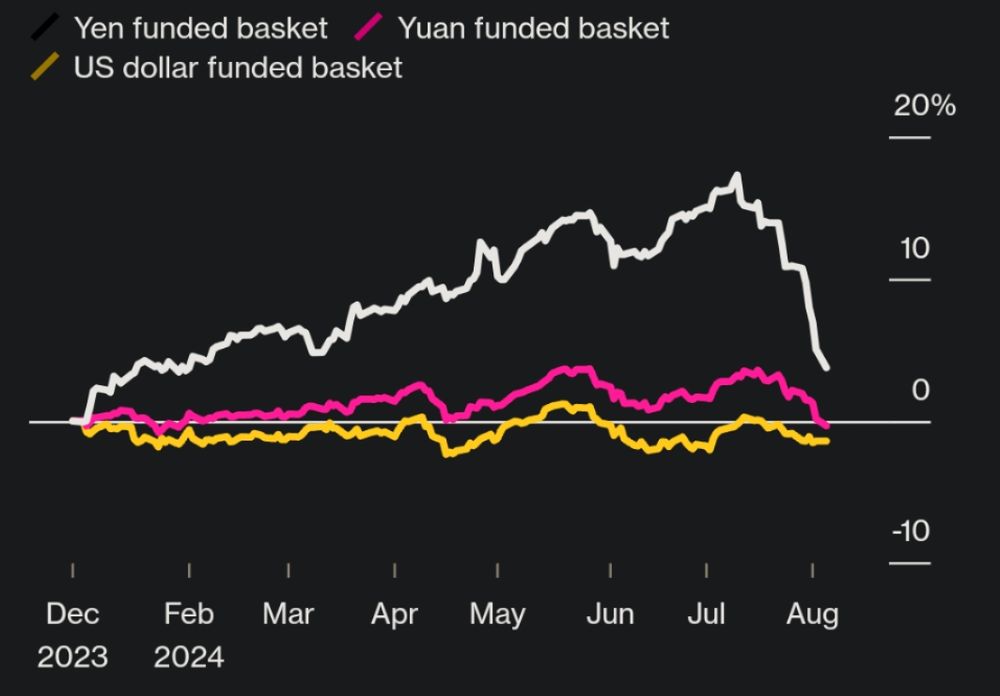

Hard not to be zoomed in to BoJ, since it's such a dominant part of the narrative. Geopol can hit that area through second order effects. Part of Napier's book has Japan and China tangled up because of implied lines in the sand when it comes to exporter positioning.

November 29, 2024 at 10:25 PM

Hard not to be zoomed in to BoJ, since it's such a dominant part of the narrative. Geopol can hit that area through second order effects. Part of Napier's book has Japan and China tangled up because of implied lines in the sand when it comes to exporter positioning.

Totem Macro has a good angle on this thesis and the liquidity aspect. Fed is focused on minimum healthy level for reserves. Stress is coming from liquidity due to bank balance sheet capacity which may be an underpriced risk. Carry trades are intrinsically tied to balance sheet capacity as well.

November 29, 2024 at 9:41 PM

Totem Macro has a good angle on this thesis and the liquidity aspect. Fed is focused on minimum healthy level for reserves. Stress is coming from liquidity due to bank balance sheet capacity which may be an underpriced risk. Carry trades are intrinsically tied to balance sheet capacity as well.

...another good one that your recommendation reminds me of. More focused on the "unwind" part. but with Napoleonic Mercantilism coming back into vogue, It may be prudent to prepare for rogue waves with cross-border capital flows. Russell Napier has a great voice too. Would recommend the audio.

November 29, 2024 at 9:32 PM

...another good one that your recommendation reminds me of. More focused on the "unwind" part. but with Napoleonic Mercantilism coming back into vogue, It may be prudent to prepare for rogue waves with cross-border capital flows. Russell Napier has a great voice too. Would recommend the audio.

More angles on the historical action from 16. GS:

November 27, 2024 at 5:57 PM

More angles on the historical action from 16. GS:

Another angle to consider when it comes to flow effects and equities is dealer gamma exposure on both single stock and index levels. If you break out the analysis into long gamma and short gamma regimes, it's apparent that the periods where realized vol is amplified vs suppressed matters quite a bit

November 27, 2024 at 12:08 AM

Another angle to consider when it comes to flow effects and equities is dealer gamma exposure on both single stock and index levels. If you break out the analysis into long gamma and short gamma regimes, it's apparent that the periods where realized vol is amplified vs suppressed matters quite a bit

There is some seasonality that shows in the data, although on second glance pre-election years are stronger than I had mentally filed:

November 26, 2024 at 10:11 PM

There is some seasonality that shows in the data, although on second glance pre-election years are stronger than I had mentally filed:

Just buy quality factor, like COST:

November 26, 2024 at 9:16 PM

Just buy quality factor, like COST: