Parker Ross

@econparker.bsky.social

Global Chief Economist @ Arch Capital Group | ex JPM AIG HUD | Husband to Jamie; Dad to Landon, Greyson & Logan | No investment advice & views are my own 🦬🇺🇸🇮🇱

https://www.linkedin.com/in/econ-parker/

https://www.linkedin.com/in/econ-parker/

🙏

They really are!

They really are!

November 11, 2025 at 6:55 PM

🙏

They really are!

They really are!

🙏

Congrats to you too!

Congrats to you too!

November 11, 2025 at 6:55 PM

🙏

Congrats to you too!

Congrats to you too!

🙏

Already a nightly routine! 😂

Already a nightly routine! 😂

November 10, 2025 at 8:30 PM

🙏

Already a nightly routine! 😂

Already a nightly routine! 😂

Bottom line:

▶️GDP data capture the domestic surge in tech/software capex

▶️But nearly half of AI hardware is imported and netted out in net exports

The U.S. is investing in Tech at record pace, but global supply chains are doing half the heavy lifting.

▶️GDP data capture the domestic surge in tech/software capex

▶️But nearly half of AI hardware is imported and netted out in net exports

The U.S. is investing in Tech at record pace, but global supply chains are doing half the heavy lifting.

September 26, 2025 at 2:39 PM

Bottom line:

▶️GDP data capture the domestic surge in tech/software capex

▶️But nearly half of AI hardware is imported and netted out in net exports

The U.S. is investing in Tech at record pace, but global supply chains are doing half the heavy lifting.

▶️GDP data capture the domestic surge in tech/software capex

▶️But nearly half of AI hardware is imported and netted out in net exports

The U.S. is investing in Tech at record pace, but global supply chains are doing half the heavy lifting.

Here’s the kicker: the imported share of tech capex has jumped to nearly 50% - the highest on record.

So even my earlier GDP contribution charts understate the true size of the AI investment boom.

So even my earlier GDP contribution charts understate the true size of the AI investment boom.

September 26, 2025 at 2:39 PM

Here’s the kicker: the imported share of tech capex has jumped to nearly 50% - the highest on record.

So even my earlier GDP contribution charts understate the true size of the AI investment boom.

So even my earlier GDP contribution charts understate the true size of the AI investment boom.

Together, they show the full scale of the AI (and other tech-related) build-out.

September 26, 2025 at 2:39 PM

Together, they show the full scale of the AI (and other tech-related) build-out.

Now compare imports with BEA’s domestic investment data.

Both domestic and imported tech capex have surged in tandem.

Both domestic and imported tech capex have surged in tandem.

September 26, 2025 at 2:39 PM

Now compare imports with BEA’s domestic investment data.

Both domestic and imported tech capex have surged in tandem.

Both domestic and imported tech capex have surged in tandem.

Look under the hood:

Computer & networking gear imports are surging,

While semiconductor imports have actually slumped.

That’s because high-end AI GPUs often get classified under “computers,” not chips...

So the AI boom can show up more prominently in segments outside of semiconductors.

Computer & networking gear imports are surging,

While semiconductor imports have actually slumped.

That’s because high-end AI GPUs often get classified under “computers,” not chips...

So the AI boom can show up more prominently in segments outside of semiconductors.

September 26, 2025 at 2:39 PM

Look under the hood:

Computer & networking gear imports are surging,

While semiconductor imports have actually slumped.

That’s because high-end AI GPUs often get classified under “computers,” not chips...

So the AI boom can show up more prominently in segments outside of semiconductors.

Computer & networking gear imports are surging,

While semiconductor imports have actually slumped.

That’s because high-end AI GPUs often get classified under “computers,” not chips...

So the AI boom can show up more prominently in segments outside of semiconductors.

Combining the two, it's clear the economy's recent resilience is coming from the recent ramp-up in business investment in software and technology, which contributed an average of more than 1%-pt to real GDP growth in Q1 and Q2.

September 25, 2025 at 2:39 PM

Combining the two, it's clear the economy's recent resilience is coming from the recent ramp-up in business investment in software and technology, which contributed an average of more than 1%-pt to real GDP growth in Q1 and Q2.

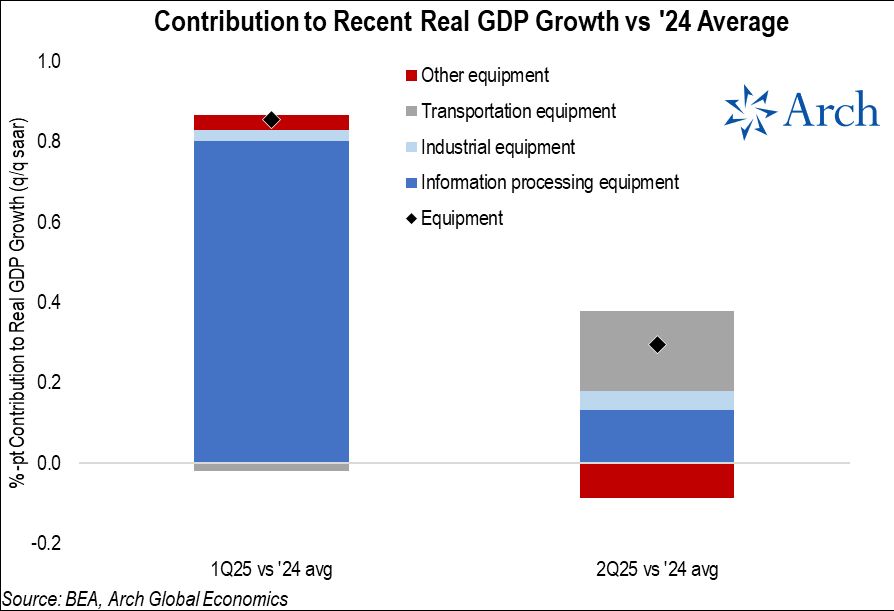

Similar story on the equipment side.

It hasn't been a massive surge in bulldozers and industrial equipment, but rather information processing equipment (again hello AI).

It hasn't been a massive surge in bulldozers and industrial equipment, but rather information processing equipment (again hello AI).

September 25, 2025 at 2:39 PM

Similar story on the equipment side.

It hasn't been a massive surge in bulldozers and industrial equipment, but rather information processing equipment (again hello AI).

It hasn't been a massive surge in bulldozers and industrial equipment, but rather information processing equipment (again hello AI).

Within Intellectual Property Products, it's again unsurprisingly mostly been about software investment (hello AI).

September 25, 2025 at 2:39 PM

Within Intellectual Property Products, it's again unsurprisingly mostly been about software investment (hello AI).

What is driving business investment in recent quarters?

Mostly Intellectual Property Products and Equipment.

Structures have unsurprisingly been a drag (similar to residential investment).

Mostly Intellectual Property Products and Equipment.

Structures have unsurprisingly been a drag (similar to residential investment).

September 25, 2025 at 2:39 PM

What is driving business investment in recent quarters?

Mostly Intellectual Property Products and Equipment.

Structures have unsurprisingly been a drag (similar to residential investment).

Mostly Intellectual Property Products and Equipment.

Structures have unsurprisingly been a drag (similar to residential investment).

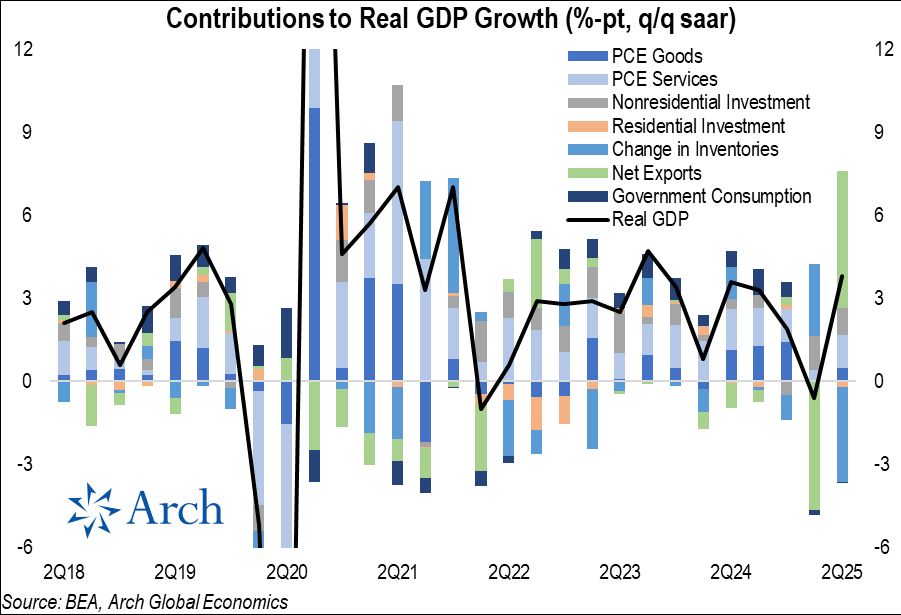

Personal consumption was a drag, along with residential investment, but business fixed investment offset most of that weakness in Q2.

September 25, 2025 at 2:39 PM

Personal consumption was a drag, along with residential investment, but business fixed investment offset most of that weakness in Q2.

Again, breaking it down vs the '24 average and stripping out the volatile components (net exports, inventories) and government, we see real final sales to domestic purchasers was roughly in-line with the 2024.

September 25, 2025 at 2:39 PM

Again, breaking it down vs the '24 average and stripping out the volatile components (net exports, inventories) and government, we see real final sales to domestic purchasers was roughly in-line with the 2024.

Zooming in on the first half, here's how much each category deviated from the '24 average...

Again, we see the big swing in inventories and net exports.

Again, we see the big swing in inventories and net exports.

September 25, 2025 at 2:39 PM

Zooming in on the first half, here's how much each category deviated from the '24 average...

Again, we see the big swing in inventories and net exports.

Again, we see the big swing in inventories and net exports.

Stripping out those two volatile categories (i.e. inventories & net exports) gives you a good view on the core underlying drivers of the economy: Final Sales to Private Domestic Purchasers.

Again, now we see there was a modest dip in Q1, with Q2 back to the prior trend pace.

Again, now we see there was a modest dip in Q1, with Q2 back to the prior trend pace.

September 25, 2025 at 2:39 PM

Stripping out those two volatile categories (i.e. inventories & net exports) gives you a good view on the core underlying drivers of the economy: Final Sales to Private Domestic Purchasers.

Again, now we see there was a modest dip in Q1, with Q2 back to the prior trend pace.

Again, now we see there was a modest dip in Q1, with Q2 back to the prior trend pace.

Looking at the revised series, here's contributions to real GDP growth over time, showing all of the slowdown occurred in Q1, with exports and inventories driving most of the swing.

September 25, 2025 at 2:39 PM

Looking at the revised series, here's contributions to real GDP growth over time, showing all of the slowdown occurred in Q1, with exports and inventories driving most of the swing.

Looking at the breadth and severity of increases in insured unemployment across states, two-thirds are up y/y, but only 23% are up more than 10bps.

So, there's widespread softening, but it's not very rapid.

So, there's widespread softening, but it's not very rapid.

September 25, 2025 at 2:37 PM

Looking at the breadth and severity of increases in insured unemployment across states, two-thirds are up y/y, but only 23% are up more than 10bps.

So, there's widespread softening, but it's not very rapid.

So, there's widespread softening, but it's not very rapid.