Cara Pacitti

@carapacitti.bsky.social

Senior economist at Resolution Foundation, mainly working on housing and public finances. All views my own.

The cash measure of the government’s balance sheet (the central government net cash requirement) is now sitting £10.9bn above forecast, showing a similar gap from the OBR’s estimates as central government net borrowing (the accrued measure).

February 21, 2025 at 8:46 AM

The cash measure of the government’s balance sheet (the central government net cash requirement) is now sitting £10.9bn above forecast, showing a similar gap from the OBR’s estimates as central government net borrowing (the accrued measure).

On the spending side, central government spending was £1.9bn higher than OBR forecasts for this month (and now £0.3bn higher than expected for the fiscal year so far – so broadly in line with forecast, see below).

February 21, 2025 at 8:46 AM

On the spending side, central government spending was £1.9bn higher than OBR forecasts for this month (and now £0.3bn higher than expected for the fiscal year so far – so broadly in line with forecast, see below).

The main driver is tax receipts, which were £4.6bn weaker than the OBR expected this month, pushing up borrowing relative to the OBR’s forecast, and are now £7.7bn lower than the OBR forecast for the year to date.

February 21, 2025 at 8:46 AM

The main driver is tax receipts, which were £4.6bn weaker than the OBR expected this month, pushing up borrowing relative to the OBR’s forecast, and are now £7.7bn lower than the OBR forecast for the year to date.

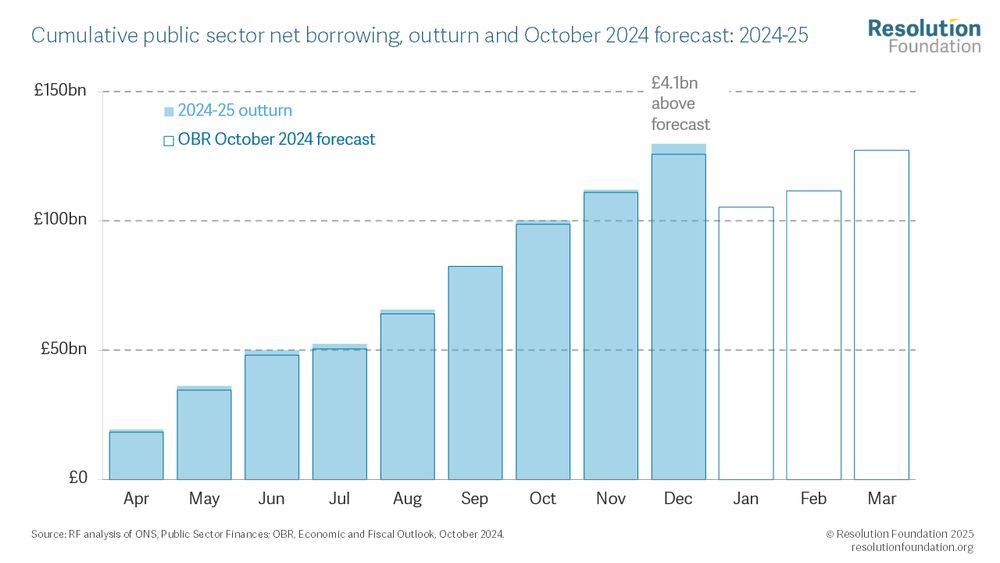

This leaves borrowing now running a huge £12.8bn higher than the OBR forecast over the first ten months of the fiscal year (Apr-Jan) – which is a significant gap given they only delivered their most recent forecasts four months ago!

February 21, 2025 at 8:46 AM

This leaves borrowing now running a huge £12.8bn higher than the OBR forecast over the first ten months of the fiscal year (Apr-Jan) – which is a significant gap given they only delivered their most recent forecasts four months ago!

The public sector was in surplus by £15.4bn in December – this is the highest monthly surplus since such records began in 1993 (in nominal terms). Bringing in more in receipts than we spent in January might sound like good news for the Chancellor – but there’s a (seriously big) catch!

February 21, 2025 at 8:46 AM

The public sector was in surplus by £15.4bn in December – this is the highest monthly surplus since such records began in 1993 (in nominal terms). Bringing in more in receipts than we spent in January might sound like good news for the Chancellor – but there’s a (seriously big) catch!

The cash measure of the government’s balance sheet (the central government net cash requirement) now sitting £0.8bn below forecast, showing a much smaller gap from the OBR’s estimates than central government borrowing (the accrued measure).

January 22, 2025 at 8:26 AM

The cash measure of the government’s balance sheet (the central government net cash requirement) now sitting £0.8bn below forecast, showing a much smaller gap from the OBR’s estimates than central government borrowing (the accrued measure).

Meanwhile, tax receipts are largely in line with what the OBR expected so far this month, and are £1.8bn lower than the OBR forecast for the year to date.

January 22, 2025 at 8:26 AM

Meanwhile, tax receipts are largely in line with what the OBR expected so far this month, and are £1.8bn lower than the OBR forecast for the year to date.

This is primarily driven by central government spending which was £2.7bn higher than OBR forecasts for this month (although still sits £4.2bn lower than expected for the first three quarters of the fiscal year – see below).

January 22, 2025 at 8:25 AM

This is primarily driven by central government spending which was £2.7bn higher than OBR forecasts for this month (although still sits £4.2bn lower than expected for the first three quarters of the fiscal year – see below).

And more importantly, if we compare borrowing for this month against the OBR’s most recent forecast, it’s £3.2bn higher – with borrowing now running £4.1bn higher than the OBR forecast over the first three quarters of the fiscal year (Apr-Dec).

January 22, 2025 at 8:25 AM

And more importantly, if we compare borrowing for this month against the OBR’s most recent forecast, it’s £3.2bn higher – with borrowing now running £4.1bn higher than the OBR forecast over the first three quarters of the fiscal year (Apr-Dec).

But back to today’s data… Public sector borrowing was £17.8bn in December – over £10bn higher than this time last year, and the highest December borrowing in four years (in nominal terms) - and the third highest on record after the depths of the financial crisis in 2009 and the pandemic in 2020.

January 22, 2025 at 8:25 AM

But back to today’s data… Public sector borrowing was £17.8bn in December – over £10bn higher than this time last year, and the highest December borrowing in four years (in nominal terms) - and the third highest on record after the depths of the financial crisis in 2009 and the pandemic in 2020.

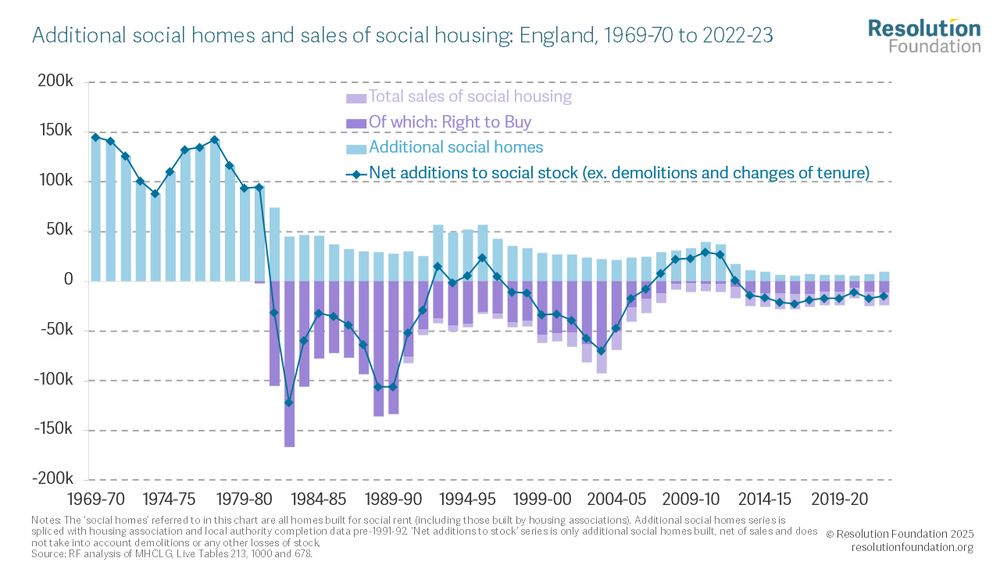

If, however, the Government wanted to return the UK’s affordable housing stock back to the level when it was last in power, 400,000 new social homes would be needed – at a cost of £50 billion.

January 15, 2025 at 12:03 PM

If, however, the Government wanted to return the UK’s affordable housing stock back to the level when it was last in power, 400,000 new social homes would be needed – at a cost of £50 billion.

Changes include tweaking the discount formula, and increasing the numbers of years tenants must have lived in their home to qualify from three up to ten years. As a result of this eligibility change, around 500,000 fewer tenants would be currently eligible to buy their own council homes.

January 15, 2025 at 12:03 PM

Changes include tweaking the discount formula, and increasing the numbers of years tenants must have lived in their home to qualify from three up to ten years. As a result of this eligibility change, around 500,000 fewer tenants would be currently eligible to buy their own council homes.

Stepping back - Right to Buy has enabled over 2mn people to buy their homes from local councils since its introduction in 1980, but the failure to replace these homes has resulted in a catastrophic decline in the social housing stock.

January 15, 2025 at 12:03 PM

Stepping back - Right to Buy has enabled over 2mn people to buy their homes from local councils since its introduction in 1980, but the failure to replace these homes has resulted in a catastrophic decline in the social housing stock.

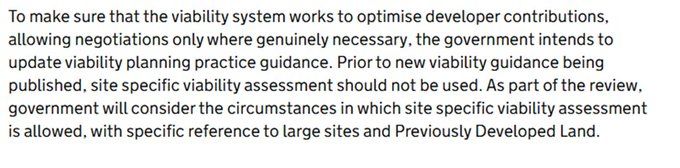

Promised updates to guidance on viability negotiations are welcome though if they give local authorities more strength to push back on developers trying to negotiate down their affordable housing contributions.

December 12, 2024 at 2:31 PM

Promised updates to guidance on viability negotiations are welcome though if they give local authorities more strength to push back on developers trying to negotiate down their affordable housing contributions.

A shift towards building in unaffordable areas in the South, such as London and Cambridge, means Midlands and Northern cities lose out from these changes to the Standard Method - and cities like Birmingham and Manchester remain key to any plausible strategy to stronger UK growth.

December 12, 2024 at 2:31 PM

A shift towards building in unaffordable areas in the South, such as London and Cambridge, means Midlands and Northern cities lose out from these changes to the Standard Method - and cities like Birmingham and Manchester remain key to any plausible strategy to stronger UK growth.

2. And a shift away from relatively affordable areas (primarily in the North) means targets are higher in areas that are more productive (relative to the government's pre-consultation targets in the summer).

December 12, 2024 at 2:31 PM

2. And a shift away from relatively affordable areas (primarily in the North) means targets are higher in areas that are more productive (relative to the government's pre-consultation targets in the summer).

1. This change means the targets perform better in terms of targeting homes in areas of low affordability (see blue bars below).

December 12, 2024 at 2:31 PM

1. This change means the targets perform better in terms of targeting homes in areas of low affordability (see blue bars below).

This was previously set to be calculated as below, with an affordability 'adjustment factor' boosting targets in areas where house prices were more than four times incomes.

December 12, 2024 at 2:31 PM

This was previously set to be calculated as below, with an affordability 'adjustment factor' boosting targets in areas where house prices were more than four times incomes.

Courtesy of the English Private Landlord Survey out this morning - annual reminder that although there are landlords with Buy to Let mortgages that will be facing higher costs due to interest rate rises, over 40% of landlords have no borrowing of any kind on any of their properties.

December 5, 2024 at 9:54 AM

Courtesy of the English Private Landlord Survey out this morning - annual reminder that although there are landlords with Buy to Let mortgages that will be facing higher costs due to interest rate rises, over 40% of landlords have no borrowing of any kind on any of their properties.

But it's worth noting that while we've seen a significant loosening this budget, fiscal policy ends up relatively tight by the end of the forecast - broadly appropriate in the context of an economy operating close to full capacity and with ample room for interest rates cuts.

October 31, 2024 at 2:30 PM

But it's worth noting that while we've seen a significant loosening this budget, fiscal policy ends up relatively tight by the end of the forecast - broadly appropriate in the context of an economy operating close to full capacity and with ample room for interest rates cuts.

This amounts to the biggest fiscal loosening on record since 2010 (excluding interventions made at the height of the pandemic) - so it's unsurprising we've seen gilt rates rise as it's likely the Bank will slow the pace of rate cuts in response.

October 31, 2024 at 2:30 PM

This amounts to the biggest fiscal loosening on record since 2010 (excluding interventions made at the height of the pandemic) - so it's unsurprising we've seen gilt rates rise as it's likely the Bank will slow the pace of rate cuts in response.

Taking this all together - we've seen nearly £145bn of additional borrowing across the forecast - £240bn of current spending increases and £97bn of capital spending, offset by £140bn of tax rises and £50bn of economic effects of policy.

October 31, 2024 at 2:29 PM

Taking this all together - we've seen nearly £145bn of additional borrowing across the forecast - £240bn of current spending increases and £97bn of capital spending, offset by £140bn of tax rises and £50bn of economic effects of policy.

Should we worry about high interest costs? A step back - many of the tough decisions being made by the Chancellor are the result of public finances that have become much more tricky to balance given high debt interest costs (and a less healthy population).

October 31, 2024 at 2:29 PM

Should we worry about high interest costs? A step back - many of the tough decisions being made by the Chancellor are the result of public finances that have become much more tricky to balance given high debt interest costs (and a less healthy population).

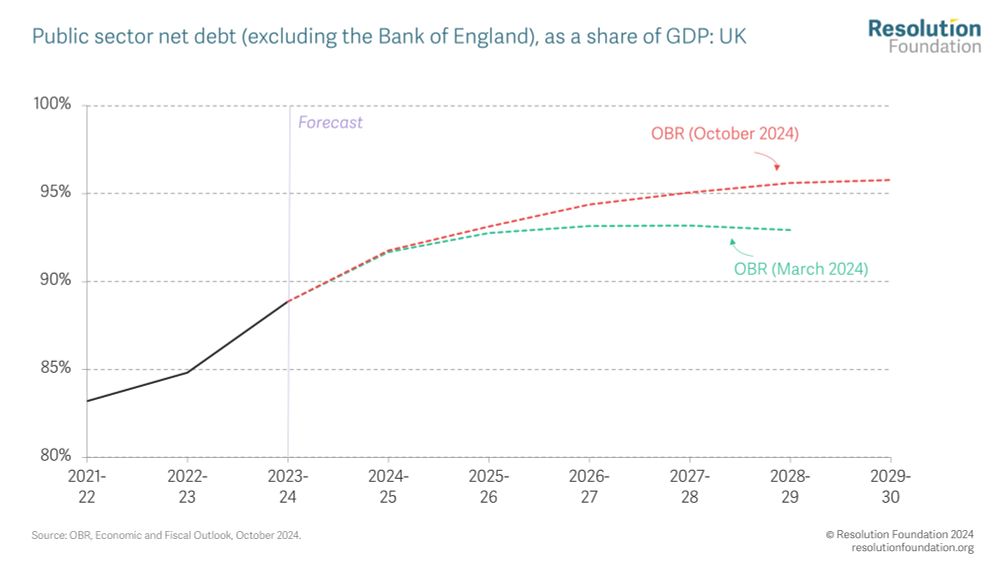

Moving to a PSNFL rule allows the Chancellor to borrow much more to increase investment, with headroom expanding by £21bn relative to the previous target, as the treatment of QE and student loan flows means PSNFL is falling faster than PSND (ex. BofE) across the forecast.

October 31, 2024 at 2:28 PM

Moving to a PSNFL rule allows the Chancellor to borrow much more to increase investment, with headroom expanding by £21bn relative to the previous target, as the treatment of QE and student loan flows means PSNFL is falling faster than PSND (ex. BofE) across the forecast.

The previous Government's fiscal rules wouldn't have had room to implement this - Jeremy Hunt's fiscal rule to have debt ex. Bank of England falling in 2029-30 would be broken by £6bn in the current forecasts.

October 31, 2024 at 2:27 PM

The previous Government's fiscal rules wouldn't have had room to implement this - Jeremy Hunt's fiscal rule to have debt ex. Bank of England falling in 2029-30 would be broken by £6bn in the current forecasts.